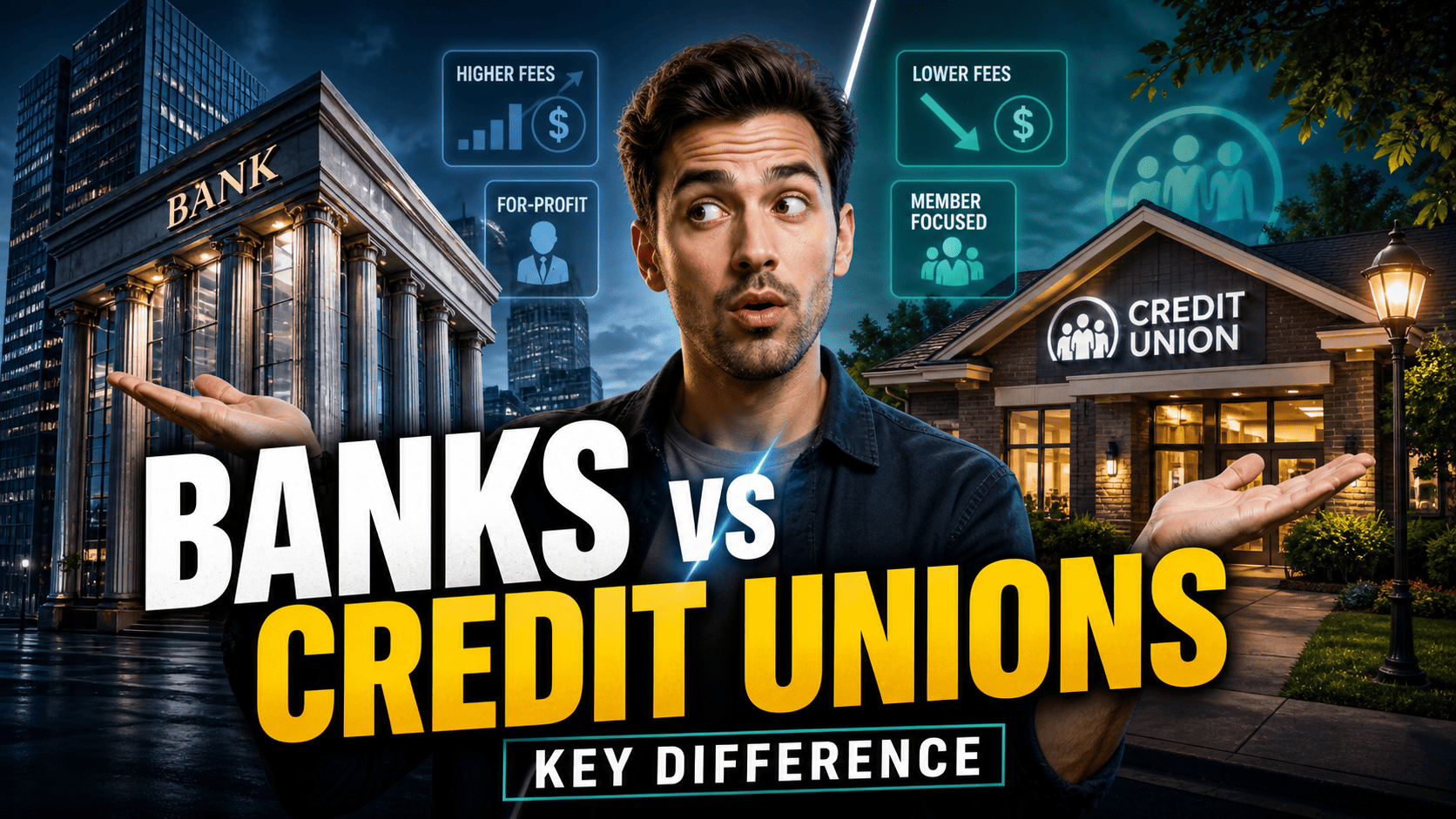

Quick Answer: The major difference between retail banks and credit unions comes down to who owns them and where the money goes. Retail banks are for-profit businesses owned by shareholders, while credit unions are not-for-profit institutions owned by you — the member. That one difference shapes everything from the fees you pay to the interest rates you get and how you're treated when you walk through the door.

So you're trying to figure out what is a major difference between retail banks and credit unions — and honestly, it's a question more people should be asking. Whether you're opening your first checking account, shopping for a better loan rate, or just tired of paying too many fees, understanding this difference can save you real money.

Here's the thing. Banks and credit unions look alike on the surface. They both hold your money, offer loans, and give you a debit card. But underneath, they run on completely different engines. And once you see that, choosing between them gets a whole lot easier.

Quick Comparison: Retail Banks vs Credit Unions

Before we get into the details, here's a simple side-by-side look at how these two stack up.

| Feature | Retail Bank | Credit Union |

|---|---|---|

| Ownership | Shareholders / investors | You — the members |

| Profit Model | For-profit | Not-for-profit |

| Main Goal | Generate profit for shareholders | Serve members and return value |

| Fees | Often higher monthly and service fees | Typically lower or no monthly fees |

| Loan Rates | Usually higher interest rates on loans | Often lower interest rates on loans |

| Savings Rates | Typically lower APY on savings | Often higher APY on savings |

| Access | Large branch and ATM networks nationwide | Smaller networks; shared ATM programs |

| Eligibility | Open to the general public | May require membership eligibility |

| Insurance | FDIC-insured (up to $250,000) | NCUA-insured (up to $250,000) |

| Customer Focus | Transaction-oriented, technology-driven | Relationship-oriented, community-focused |

Now let's break all of this down so it actually makes sense.

What Is a Retail Bank?

You've probably been inside a retail bank hundreds of times without even thinking about what makes it a "retail" bank. Simply put, it's a bank that serves regular people like you and me — not giant corporations or Wall Street investors.

Retail Bank Meaning

A retail bank is any bank that focuses on everyday consumers and small businesses. It's where you go to open a checking account, deposit your paycheck, get a car loan, or apply for a mortgage. You might also hear them called consumer banks or personal banks. Same thing, different name.

Common Retail Bank Services

Retail banks offer pretty much everything you'd expect — checking and savings accounts, certificates of deposit, debit and credit cards, personal loans, auto loans, mortgages, home equity loans, online and mobile banking, wire transfers, and safe deposit boxes. The bigger ones also offer investment services, insurance, and wealth management if you need that kind of thing.

Examples of Retail Banks

You know the names. Bank of America, JPMorgan Chase, Wells Fargo, Citibank, U.S. Bank — these are the heavy hitters. They serve millions of customers and have thousands of branches and ATMs spread across the country. If you've ever driven past a bank on a street corner, chances are it was one of these.

What Is a Credit Union?

Now here's where things get interesting. A credit union looks a lot like a bank from the outside, but it works very differently on the inside. A credit union is different from a bank mainly because it's built to serve you, not to make money for someone else.

Credit Union Meaning

A credit union is a financial cooperative that's owned and run by the people who use it. That means if you have an account there, you're not just a customer — you're literally one of the owners. Every member gets an equal vote in how things are run, no matter how much money is in their account. Pretty different from a bank, right?

Who Owns Credit Unions?

You do. Well, the members do. When you open an account at a credit union, you become a part-owner. Members elect a volunteer board of directors who make the big decisions. There are no outside shareholders pocketing profits from your fees or your loan interest. The money stays in the family, so to speak.

What Do Credit Unions Offer?

Pretty much everything a bank offers. You'll find checking accounts (they sometimes call them share draft accounts), savings accounts (share accounts), money market accounts, CDs (share certificates), credit cards, auto loans, personal loans, mortgages, business accounts, and online and mobile banking. The product lineup is more similar than most people realize.

Credit Union Examples

Credit unions come in all shapes and sizes. Some are built around a specific employer, like a big tech company or government agency. Others serve a certain community, geographic region, military branch, or school district. You've probably heard of some of the bigger ones — Navy Federal Credit Union, Pentagon Federal Credit Union, and State Employees' Credit Union. But there are also thousands of smaller, local credit unions that fly under the radar and do great work.

The Major Difference Between Retail Banks and Credit Unions

Alright, let's get to the heart of it. The major difference between banks and credit unions is that banks are for-profit companies owned by shareholders, and credit unions are not-for-profit cooperatives owned by their members. That's the big one. And it changes everything.

Retail Banks Are For-Profit

When a retail bank makes money — through loan interest, account fees, service charges, you name it — that profit goes to shareholders. The bank's first priority is making those investors happy. You're important as a customer, sure, but the shareholders are the ones the bank ultimately answers to.

Credit Unions Are Not-for-Profit

A credit union doesn't have shareholders to please. So when it earns more than it spends, that extra money goes right back to you in the form of better savings rates, lower loan rates, fewer fees, and improved services. "Not-for-profit" doesn't mean they can't make money. It just means the money works for you instead of for Wall Street.

Why Ownership Changes Everything

Think about it this way. If a bank needs to boost profits for its investors, it might raise your fees or keep your savings rate low. A credit union doesn't have that pressure. It can afford to charge you less, pay you more on your savings, and treat you like a person instead of a transaction number. That ownership difference is the root of almost every other difference you'll notice between these two.

How Are Credit Unions Different From Banks?

Let's zoom in on the specific ways credit unions differ from retail banks — the stuff that actually affects your wallet and your experience.

1. Ownership Structure

With a bank, you're a customer. The bank is owned by private shareholders or public investors. With a credit union, you're a member-owner. You get voting rights and a real say in how the place is run. It's a completely different relationship.

2. Profit Purpose

Banks exist to make money for their owners. Credit unions exist to serve their members. Both need to stay financially healthy, but their reasons for existing are fundamentally different. A bank sends profits to shareholders. A credit union reinvests them into better services for you.

3. Fees

This is where you'll really feel the difference in your pocket. Credit unions tend to charge significantly lower fees — monthly maintenance fees, overdraft fees, ATM fees, loan origination fees, you name it. Some credit unions offer completely free checking with no minimum balance. The National Credit Union Administration (NCUA) data consistently shows that credit union fee structures run lower across the board.

4. Interest Rates

Here's another big one. Credit unions frequently offer higher APY on your savings and lower interest rates on loans and credit cards. If you're trying to grow your savings or borrow money without getting crushed by interest, a credit union can make a real difference over time.

5. Membership Requirements

Banks are open to pretty much everyone. Walk in, show your ID, and you're in. Credit unions are a little different — they usually require you to meet some kind of eligibility criteria. Maybe you work for a certain employer, live in a specific area, served in the military, or belong to a qualifying organization. The good news? A lot of credit unions have loosened their requirements in recent years, so it's easier to join than you might think.

6. Branch and ATM Access

Big banks win on sheer size. If you travel a lot or move around, having Chase or Bank of America branches everywhere is genuinely convenient. Credit unions are usually smaller, but here's the workaround — many of them participate in shared branching networks like CO-OP Shared Branch, which gives you access to thousands of locations and ATMs across the country. It's not quite the same as having a mega-bank on every corner, but it's closer than most people expect.

7. Customer Service

This is where credit unions really shine. Because they're member-owned and community-driven, they tend to treat you like a neighbor, not a number. You're more likely to talk to someone who knows your name and actually cares about your situation. Banks, on the other hand, might offer fancier apps and faster tech — but the service can feel a bit cold and transactional. For what it's worth, the Consumer Financial Protection Bureau (CFPB) has noted that credit unions consistently receive fewer consumer complaints relative to their size than large banks.

Similarities Between Banks and Credit Unions

Okay, so they're different — but they're also more alike than you might think. Let's talk about the similarities between banks and credit unions so you get the full picture.

Both Offer Deposit Accounts

Whether you walk into a bank or a credit union, you'll find checking accounts, savings accounts, CDs, and money market accounts. The products work basically the same way. Credit unions just use slightly different names sometimes.

Both Offer Loans

Need an auto loan, personal loan, mortgage, home equity line, or credit card? Both banks and credit unions have you covered. The application process and product structures are very similar at both.

Both Offer Digital Banking

Gone are the days when credit unions were stuck in the past with their technology. Most modern credit unions now offer solid mobile apps, online banking, bill pay, electronic transfers, and mobile check deposit. The big banks still have an edge in some areas, but the gap has gotten much smaller.

Both Can Be Federally Insured

This one matters a lot. Banks are typically insured by the Federal Deposit Insurance Corporation (FDIC), and federally insured credit unions are covered by the National Credit Union Administration (NCUA). Both protect your deposits up to $250,000 per depositor, per institution. So your money is just as safe at a credit union as it is at a bank — as long as the institution is federally insured.

Bank vs Credit Union: Which Is Better?

Honestly? There's no one-size-fits-all answer. It really depends on what matters most to you. Here's a quick way to think about it.

Choose a Retail Bank If You Want

Go with a bank if you need a massive branch and ATM network wherever you travel, want the latest and greatest mobile banking technology, need a huge selection of financial products and premium rewards credit cards, rely on business banking or commercial services, need international wire transfers and global access, or prefer seamless integration with popular financial apps.

Choose a Credit Union If You Want

Go with a credit union if you're looking for lower monthly fees and fewer surprise charges, better interest rates on both your savings and your loans, a more personal, community-oriented banking experience, a financial institution that genuinely puts your interests first, or access to financial education and member-only perks.

Best Option for Savings Account

If growing your savings is your top priority, credit unions often come out ahead. Many offer higher APY on savings accounts and share certificates compared to retail banks. Over months and years, that higher yield adds up to real money in your pocket.

Best Option for Loans

Planning to borrow? Check with a credit union first. They frequently offer lower rates on auto loans, personal loans, and credit cards. Comparing rates before you commit could save you hundreds — or even thousands — over the life of your loan. It's one of those small steps that makes a big difference.

Best Option for Convenience

If you need branches and ATMs in every city you visit, and you want the absolute best digital experience, a large retail bank is probably your best bet. Just know that the extra convenience often comes with higher fees and lower rates. It's a trade-off worth thinking about.

Are Credit Unions Safer Than Banks?

This is one of the most common questions people ask, and the answer is reassuring. Both banks and credit unions are safe places for your money — as long as they're federally insured.

FDIC Insurance for Banks

The Federal Deposit Insurance Corporation (FDIC) has been protecting bank depositors since 1933. If your FDIC-insured bank ever fails, your deposits are covered up to $250,000 per depositor, per insured bank, for each account ownership category. In all that time, no depositor has ever lost a single penny of insured funds. That's a pretty solid track record.

NCUA Insurance for Credit Unions

The National Credit Union Administration (NCUA) offers the same level of protection for federally insured credit unions through the National Credit Union Share Insurance Fund (NCUSIF). Your deposits are covered up to $250,000, and this insurance carries the full faith and backing of the United States government — same as the FDIC.

What This Means for You

Bottom line? Your money is protected either way, as long as you're banking with a federally insured institution. Before you open any account, it's a smart move to double-check. You can verify a bank's status with the FDIC's BankFind tool, or look up a credit union on the NCUA's Credit Union Locator. Takes about 30 seconds, and it's worth the peace of mind.

Is a Credit Union a Bank?

Short answer — no, not technically. A credit union isn't a bank. But it does a lot of the same things a bank does. You can open checking and savings accounts, get loans, use credit cards, and do all your banking online, just like you would at a traditional bank.

The real difference? A bank is usually a for-profit company owned by shareholders. A credit union is a not-for-profit cooperative owned by its members — by you. For your day-to-day banking, the experience will feel pretty similar. But behind the scenes, the motivations driving each institution are very different.

Credit Unions Differ From Retail Banks Because They Are Member-Owned

This is worth saying one more time, because it really is the whole ballgame. Credit unions differ from retail banks because they are member-owned cooperatives. When you join one, you're not just opening an account — you're becoming a part-owner of the institution.

That means you get to vote on the board of directors. You get a seat at the table during annual meetings. And you directly benefit from the credit union's success through better rates, lower fees, and improved services. Everything flows from this one idea: the credit union exists to serve you, not to make someone else rich.

Pros and Cons of Retail Banks

Pros of Retail Banks

Let's give banks their credit (no pun intended). They offer some genuine advantages — huge branch and ATM networks you can rely on anywhere, cutting-edge mobile and online banking, a massive selection of financial products, strong business banking and commercial lending, international capabilities, and top-tier rewards credit cards. If you need scale and technology, banks deliver.

Cons of Retail Banks

On the flip side, you'll often deal with higher monthly fees and service charges, lower interest rates on your savings, customer service that can feel impersonal and rushed, policies designed to maximize profit rather than help you, and sometimes tougher requirements to get approved for loans. The convenience comes at a cost.

Pros and Cons of Credit Unions

Pros of Credit Unions

Credit unions bring a lot to the table — lower fees across the board, higher APY on your savings and CDs, lower rates on loans and credit cards, friendly and personalized service, a democratic structure where your voice actually counts, and financial education programs designed to help you get ahead. If you want your financial institution to feel like it's on your team, credit unions deliver that.

Cons of Credit Unions

Fair warning, though — credit unions aren't perfect for everyone. You might run into membership eligibility requirements that limit your options, fewer physical branches (especially if you travel a lot), a smaller selection of specialized products, mobile apps and tech that can lag behind the biggest banks, and limited international banking services. These are real trade-offs worth considering.

Simple Example: Bank vs Credit Union

Let's make this really concrete. Say you and your neighbor both need a $25,000 auto loan. You apply at a big retail bank and get offered 6.5 percent for 60 months. Your neighbor walks into the local credit union and gets 5.0 percent for the same term.

Over the life of that loan, your neighbor pays roughly $1,000 less in total interest. Why? Because the credit union isn't trying to squeeze maximum profit out of every loan — it's trying to give its members the best deal possible.

Now, you might get a slicker online application and more branches to visit if you ever need help. Your neighbor might have to drive a bit further for in-person support. Both experiences have value. The question is which one matters more to you.

Final Answer: What Is the Major Difference?

Let's bring it all home. The major difference between retail banks and credit unions is that retail banks are for-profit institutions owned by shareholders, while credit unions are not-for-profit institutions owned by their members.

That one difference — ownership — is the reason credit unions tend to charge lower fees, offer better rates, and provide more personalized service. And it's the reason retail banks tend to offer bigger networks, more products, and more advanced technology.

Neither one is objectively "better." They're built for different priorities. Now that you understand what sets them apart, you're in a much stronger position to pick the one that actually works for your life, your goals, and your wallet.

Frequently Asked Questions

What is a major difference between retail banks and credit unions? It all comes down to ownership and profit. Retail banks are for-profit businesses owned by shareholders. Credit unions are not-for-profit cooperatives owned by you — the members. That difference shapes everything from your fees to your interest rates to how you're treated.

What is the difference between a bank and a credit union? A bank is typically owned by investors or shareholders and run for profit. A credit union is owned by its members and run to serve them. Both offer similar products, but their goals and cost structures are very different.

Are credit unions better than banks? It depends on what you need. Credit unions usually have lower fees and better rates. Banks usually offer bigger networks and better tech. There's no universal winner — just the one that fits your priorities best.

Is a credit union a bank? Not technically. But for your everyday banking needs — checking, savings, loans, credit cards, online banking — a credit union does pretty much everything a bank does. The key difference is who owns it and where the profits go.

Who owns credit unions? The members do. When you open an account at a credit union, you become a part-owner with equal voting rights. Members elect a volunteer board of directors to steer the ship. There are no outside shareholders taking profits.

What do banks and credit unions have in common? More than you'd think. Both offer deposit accounts, loans, credit cards, and digital banking. Both can be federally insured — banks by the FDIC and credit unions by the NCUA — with deposits protected up to $250,000.

What services do credit unions provide? Just about everything you'd find at a bank — checking and savings accounts, CDs, auto loans, personal loans, mortgages, credit cards, online banking, mobile banking, and often financial education programs too.

Are banks and credit unions insured? Yes, as long as they're federally insured. Banks are covered by the FDIC and credit unions by the NCUA. Both programs protect your deposits up to $250,000 per depositor, per institution, for each account ownership category.

Why do credit unions often have lower fees? Because they're not-for-profit and member-owned, credit unions don't need to generate returns for outside shareholders. That means they can pass the savings along to you through lower fees, better rates, and reduced charges.

Should I choose a bank or a credit union? If you want nationwide access, top-tier tech, and a wide product range — go with a bank. If you want lower fees, better rates, and a more personal experience — go with a credit union. And honestly, a lot of people use both to get the best of both worlds.