Getting pre-approved for a home loan might appear daunting because it requires a thorough examination of your financial situation. During this process, the lender assesses your credit report, verifies your income through detailed documentation, and checks your debt-to-income ratio to confirm your financial stability. A good credit score plays a key role in how to get pre-approved for a home loan.

What Does It Mean to Get Pre-Approved for a Home Loan?

Think of pre-approval as a lender giving you a conditional green light. It’s their commitment—based on a thorough review—to lend you a specific sum for a home. This isn't a back-of-the-napkin estimate; it's a formal step that shows sellers you're a serious buyer who can actually get the financing. The result is a pre-approval letter that strengthens your position.

The lender isn't just taking your word for it. They're going to verify every financial detail you provide, from your employment history to your down payment amount, moving past the self-reported numbers to get the real story. This comprehensive credit report review is the very heart of the mortgage pre-approval process.

The Core Components of Pre-Approval

When a lender decides if you're a good candidate for a mortgage, they're really looking at a few key pieces of your financial puzzle. Each one helps them see if you can handle the responsibility of a home loan and meets their lender requirements.

Here’s what they're zeroing in on:

Credit Score and History: The first thing they'll do is a hard credit inquiry. They're looking for a strong payment history and a solid credit score that shows you're a reliable borrower.

Income Verification: You’ll need to prove what you earn. This means handing over loan application documentation like W-2s, tax returns, and your most recent pay stubs to confirm your monthly income assessment is accurate and, just as importantly, stable.

Debt-to-Income (DTI) Ratio: This is a big one. They'll add up all your monthly debt payments and compare that total to your gross monthly income. Your debt-to-income ratio gives them a clear picture of how much of your money is already spoken for.

Assets and Down Payment: Lenders need to see that you have the cash on hand for the down payment amount and closing costs. Bank statements and investment account information will be required.

Why This Detailed Review Matters

This whole process is about proving your financial stability and defining your true borrowing power. By putting your credit history and income under a microscope, the lender gets the confidence they need to approve your loan. Knowing these lender requirements ahead of time is absolutely crucial, and it helps determine your interest rate estimate and available loan program options. A successful property appraisal will be the final step.

For funding companies, using a credit intelligence tool like Score Machine can significantly increase funding volume. By pre-vetting applicants, the platform identifies fundable clients faster, reduces the time spent on unqualified leads, and provides a clear roadmap for borderline cases to become approval-ready. This efficiency directly translates to more closed loans and improved portfolio performance.

Once you’ve gone through the mortgage pre-approval process, you walk away with a firm budget and a powerful pre-approval letter. This document makes you a much more attractive buyer, signaling to sellers that you're a low-risk, prepared candidate ready to make a competitive offer. It truly sets the stage for a much smoother path to owning a home.

Why Is Home Loan Pre-Approval Important Before You Start House Hunting?

Think of a pre-approval letter as your golden ticket in the home-buying game. It’s the ultimate power move, instantly signaling to sellers and their agents that you’re not just browsing—you're a serious, qualified buyer ready to make a move. This isn't just a casual estimate; it's a document showing a lender has already dug into your finances and has agreed, in principle, to lend you a specific amount of money. The mortgage pre-approval process gives you credibility.

In a hot market, having a pre-approval is basically table stakes. Picture this: a seller gets two nearly identical offers. One comes from a buyer with a solid pre-approval letter in hand, and the other doesn't. Who do you think they'll choose? The pre-approved buyer, every single time. It dramatically lowers the seller's risk of a deal collapsing at the last minute over financing issues related to income verification or credit score.

But this letter isn't just for sellers. It’s for you. The mortgage pre-approval process forces you to get real about your budget from day one. You'll know exactly how much house you can afford based on your monthly income assessment and debt-to-income ratio, saving you the heartache of falling for a home that's just out of reach.

Set Your Budget and Gain Confidence

One of the biggest wins from getting pre-approved early is the sheer clarity it brings. The lender gives you a solid interest rate estimate, which lets you calculate your potential monthly mortgage payment with surprising accuracy. This is a cornerstone of your future financial stability.

This upfront homework means you can walk into open houses with confidence. You know your price ceiling, so you can make quick, decisive offers without panicking about the numbers. Getting a handle on lender requirements and knowing your down payment amount from the get-go puts you way ahead of the competition.

A pre-approval letter tells everyone—sellers, agents, and even you—that you've done the financial legwork. It’s real proof that you have the borrowing power to make your homeownership dream happen.

It's also worth noting how the market is changing. First-time homebuyers now make up a record share of all home loans, and younger buyers (35 and under) are driving more than half of all financed purchases. This means lenders are scrutinizing things like credit score, income verification, and debt-to-income ratio more closely than ever, especially for buyers with a shorter financial track record. This is exactly why a thorough credit report review before you even talk to a lender is so critical. You can discover more insights about this shift in the mortgage market and how it might affect you.

Win Bidding Wars and Close Faster

When you find yourself in a multiple-offer situation, that pre-approval letter is what sets you apart. Sellers are always looking for the surest bet—the offer most likely to close without a hitch. Your letter proves you've already cleared major financial hurdles like verifying your employment history and passing a monthly income assessment.

Plus, getting your financial ducks in a row early can actually speed up the closing process. A huge chunk of the paperwork, from your loan application documentation to income verification, is already complete. This makes the final underwriting and property appraisal stages run much more smoothly. The bottom line? You get the keys to your new home faster, all because you took the time to get pre-approved before you started your search.

How Is Pre-Approval Different From Pre-Qualification?

In the world of home loans, you’ll hear "pre-qualification" and "pre-approval" thrown around a lot, often as if they mean the same thing. They absolutely do not. Getting them mixed up is a common misstep that can cause major headaches when you’re trying to buy a home.

Think of a pre-qualification as a casual chat. It’s a quick, back-of-the-napkin calculation based entirely on numbers you give the lender—your estimated income, your debts, what you think your credit score is. There's no deep dive, no hard credit report review, and no one is asking for your loan application documentation just yet. It’s a rough estimate, a starting point to see what you might be able to borrow.

The mortgage pre-approval process, however, is the real deal. This is the formal interview. A lender will pull your credit, scrutinize your financial documents, and complete a full income verification. They want to see your employment history and confirm your income down to the dollar. It’s a much more involved process that demonstrates your financial stability, but it gives you a concrete answer on your actual borrowing power and a valid pre-approval letter.

Pre-Qualification vs Pre-Approval At a Glance

It's easy to see why people get these two mixed up, but their impact on your home search is worlds apart. One gives you a loose idea, while the other gives you real leverage. This table breaks down the core differences so you can see exactly what each step entails in meeting lender requirements.

| Feature | Pre-Qualification | Pre-Approval |

|---|---|---|

| Verification Level | Based on self-reported financial info | Requires verified loan application documentation (W-2s, pay stubs, bank statements) |

| Credit Check | Typically a "soft" credit pull or none at all | Requires a "hard" credit inquiry, which can affect your credit score |

| Lender Commitment | Informal estimate, not a commitment to lend | A conditional commitment to lend a specific amount via a pre-approval letter |

| Impact on Offers | Minimal; shows you've started the process | Significant; makes your offer much stronger to sellers |

| Time to Complete | Can often be done in minutes online or over the phone | Can take several days to a week, depending on your lender |

Understanding this table is key. A pre-qualification is for your own planning, but a pre-approval is for making serious moves in the market.

Why the Difference Is a Game-Changer

Sellers and their agents know this distinction inside and out. A pre-qualification is a nice first step, but it doesn't hold much water because nothing has been proven.

A pre-approval letter, on the other hand, is like cash in hand. It’s tangible proof that a lender has already vetted you and is serious about funding your loan. It signals to everyone that you are a qualified, low-risk buyer who can close the deal, pending a successful property appraisal.

A pre-qualification gives you a ballpark figure. A pre-approval gives you negotiating power. In a competitive market, a strong pre-approval letter can be the single thing that makes a seller choose your offer over someone else's.

This formal vetting process is precisely why pre-approval is so valuable. Lenders dig into every corner of your financial life to make sure you can handle the loan. You can learn more about building the financial stability they're looking for by understanding what it means to be credit ready.

A Closer Look at the Verification Process

So, what does that "deeper look" really involve? Lenders don't just ask about your debt-to-income ratio; they calculate it precisely using verified documents, leaving no room for error.

Here’s a quick rundown of what makes the mortgage pre-approval process so much more thorough:

Hard Credit Inquiry: A pre-approval requires a "hard pull" on your credit, which can cause a small, temporary dip in your credit score. This gives the lender a complete, official look at your entire credit history.

Document Verification: You’ll need to provide substantial loan application documentation. Get ready to gather a couple of years of tax returns, recent W-2s, and several months of bank statements for a full monthly income assessment.

Asset Confirmation: They will also need to see that you have the cash on hand for the down payment amount and closing costs. They want to see the money in your account.

In the end, while a pre-qualification is a fine place to start, it’s the pre-approval that truly sets you up for success. It gives you a reliable budget to shop with, makes your offers competitive, and provides the confidence you need to move forward as a serious homebuyer.

When Is the Best Time to Get Pre-Approved for a Home Loan?

Timing your mortgage pre-approval is a bit of an art. Jump the gun, and your pre-approval letter could expire before you even find a house you love. Wait too long, and you'll be in a mad dash, potentially losing out on your dream home because you can't make a serious offer. The mortgage pre-approval process has a distinct timeline.

So, what's the sweet spot? For most people, it's a good idea to start getting your ducks in a row about three to six months before you plan to seriously hit the pavement. This isn't just a random number; it’s a strategic buffer. It gives you the breathing room to do a deep dive with a credit report review and fix any little surprises that might be dragging down your credit score.

This head start also means you can gather all the necessary loan application documentation—pay stubs, tax returns, bank statements—without the last-minute panic. If you have a more complicated financial picture, like being self-employed or knowing you need to work on your credit to prove your financial stability, starting even earlier, say six to twelve months out, is an even smarter move.

Syncing Up Your Pre-Approval and Your House Hunt

Here’s a critical piece of the puzzle: a pre-approval letter isn't good forever. Most of them expire after 60 to 90 days. Lenders do this because your financial situation can change—your income, your debt, your employment history. The goal is to have that powerful letter in your hand, fresh and valid, the moment you’re ready to write an offer.

This is precisely why that three-to-six-month runway is so valuable. It gives you time to:

Beef up your savings for that all-important down payment amount.

Strategically pay down credit cards or loans to improve your debt-to-income ratio.

Shop around with different lenders to compare rates and loan program options.

By planning ahead, you’re not just getting a piece of paper. You're building the strongest possible financial profile to impress lenders when it's go-time. A good monthly income assessment will help you prepare.

How the Market Shapes Your Timeline

In today’s market, a well-timed pre-approval isn't just a good idea—it's essential. The mortgage pre-approval market is growing at a staggering pace, projected to expand by 18.10% each year between 2025 and 2033. This isn’t just a statistic; it shows a fundamental shift in how people buy homes. Lenders are digging deeper than ever into your credit score, income verification, and debt-to-income ratio. Fulfilling lender requirements is key.

Knowing this, you can see why getting a clear picture of your credit before you even talk to a loan officer has become a huge advantage for smart buyers. You can read the full research on mortgage pre-approval market growth to get a better sense of where things are headed.

For lenders, this is where a tool like Score Machine can be a game-changer. It helps quickly pinpoint who is ready for a loan right now and who needs a little work, providing a clear blueprint to get them there. This turns more inquiries into closed deals.

How Do You Get Pre-Approved for a Home Loan Step by Step?

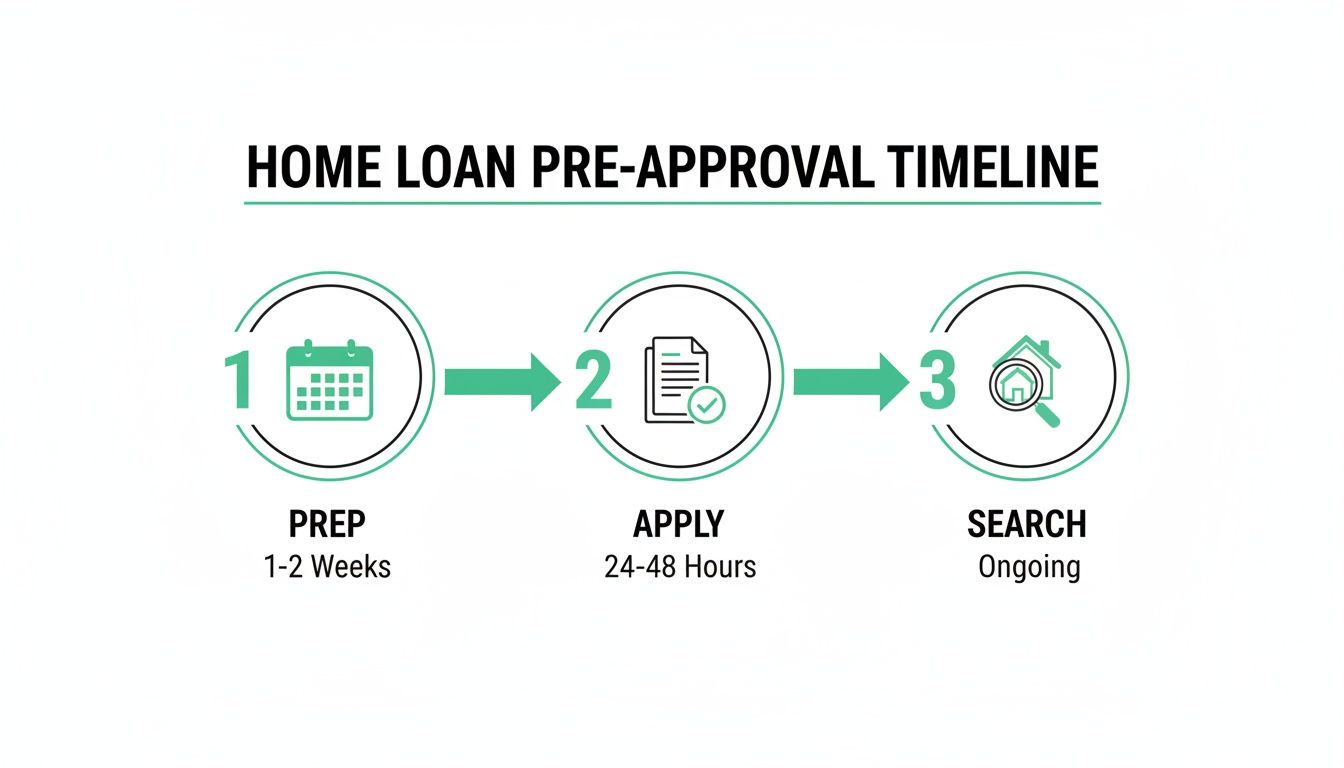

Getting pre-approved for a home loan isn't a single action—it's a journey. Think of it as building a case to prove your financial stability to a lender. The good news is that you're in the driver's seat for most of it. This roadmap will walk you through the practical, manageable steps of the mortgage pre-approval process that take you from just thinking about a new home to holding a powerful pre-approval letter.

Start With a Financial Self-Audit

Your first move, long before you ever talk to a loan officer, should be a deep dive into your own credit report for a personal credit report review. Why? Because the lender is about to do the same thing with a hard inquiry, and you don't want any surprises.

Pulling your own credit report (which is a soft pull and won't affect your score) is like proofreading your financial resume before the big interview. It gives you a chance to spot and dispute errors, identify any old accounts you forgot about, and see the exact credit score the lender will see.

This whole process can feel overwhelming, but it generally follows a clear path from prep work to actively shopping for a house.

As you can see, the time you spend getting your ducks in a row upfront directly impacts how smoothly the application and your eventual home search will go.

Get Your Paperwork in Order

Once you've reviewed your credit, it’s time to gather your loan application documentation. This is where you paint the full picture of your financial health for the lender. Being meticulously organized here can shave days, or even weeks, off your mortgage pre-approval process.

Start a folder and begin collecting these key documents:

Proof of Income: Your W-2s from the last two years and your most recent pay stubs covering a full 30-day period. This is ground zero for the lender's monthly income assessment and income verification.

Tax Returns: Have your complete federal tax returns from the past two years ready, especially if you're self-employed or your income fluctuates.

Bank and Asset Statements: Print out the last two or three months of statements for all your accounts—checking, savings, 401(k)s, brokerage accounts. This proves you have the funds for the down payment amount.

Employment Verification: The lender will call your employer to confirm your job and salary as part of your employment history review, so have your HR department’s contact info handy to avoid delays.

For mortgage companies, this document-chasing phase is often where things grind to a halt. A credit intelligence tool like Score Machine can be a game-changer here. By pre-qualifying applicants first, it ensures that only the most viable candidates—those with a high likelihood of approval—move on to the intensive documentation stage. This focuses resources where they count and can significantly boost the number of funded loans.

Run the Numbers a Lender Cares About

With your documents ready, the focus shifts to the math. The most important calculation is your debt-to-income ratio (DTI). It's simple: a lender adds up all your monthly debt payments (car, student loans, credit card minimums) and divides it by your gross monthly income.

Most lenders want to see a DTI of 43% or lower. Of course, some loan program options have more flexible lender requirements, but that's a solid benchmark to aim for. You will also get an interest rate estimate.

Next, do your own honest monthly income assessment. Don't just look at your gross pay. Figure out what you can genuinely afford for a monthly housing payment after accounting for taxes, insurance, and the inevitable costs of home maintenance. This step helps you zero in on a loan amount that truly fits your life and ensures your long-term financial stability. If you want to go deeper, there are plenty of great loan preparation strategies you can use to get your finances in fighting shape.

Choose a Lender and Make Your Move

Finally, it’s time to find a lending partner. Don't just walk into the nearest bank. Compare interest rates, closing costs, and the types of loan program options available from different sources like local banks, national credit unions, and independent mortgage brokers. Each has its own strengths and lender requirements.

Once you've picked one, you'll fill out their official application. But because you’ve done all the heavy lifting—from the credit report review to organizing every last piece of loan application documentation—this part should be a breeze. You'll submit your file, give them the green light for the hard credit pull, and wait for their decision.

A 'yes' gets you the coveted pre-approval letter. This is your golden ticket to start making serious offers on homes, with the understanding that the final loan is still contingent on a successful property appraisal.

What Does a Home Loan Pre-Approval Letter Include?

So you’ve made it through the lender’s gauntlet and have a pre-approval letter in hand. Congratulations! This document is your golden ticket in the homebuying world, instantly elevating you to a serious, competitive buyer.

Think of it this way: a pre-approval isn't just a casual thumbs-up. It’s a formal statement from a lender declaring that they’ve already dug into your finances and are, in principle, willing to lend you a specific chunk of cash. When you show this to a seller, you're not just making an offer; you're proving you have the financial stability to see it through.

Sellers love pre-approved buyers because it takes a massive amount of guesswork out of the equation. It tells them a financial institution has already completed a credit report review, verified your income verification documents, and calculated your debt-to-income ratio. That upfront work gives them confidence that the deal won't collapse at the last minute, making your offer far more attractive than one from someone who hasn't done their homework.

What’s Inside the Letter

Your pre-approval letter isn't just a single number; it contains a few key details that will guide your entire home search. Getting familiar with these components is essential for making smart moves when you start touring homes.

Here’s a quick rundown of what to look for:

Maximum Loan Amount: This is the big one—the absolute ceiling on what the lender is willing to give you. It’s your official budget.

Loan Program Options: It will name the specific loan you qualify for, whether it's a Conventional, FHA, or VA loan. These loan program options come with different lender requirements, which can influence the types of properties you can buy.

Interest Rate Estimate: The letter will include an estimated interest rate based on your credit score and financial picture at that moment. Keep in mind this rate isn't locked; it can (and often does) move with the market.

Down Payment Amount: It often mentions the down payment amount you discussed, which shows the lender has confirmed you have the necessary cash on hand.

Expiration Date: Pre-approvals have a shelf life. Look for an expiration date, which is typically 60 to 90 days out. After that, you’ll need to get your financials re-checked as part of the mortgage pre-approval process.

Reading Between the Lines

A pre-approval letter is a huge confidence booster, but it's crucial to know what it isn't: a final, done-deal guarantee. It’s a conditional approval, and a few major hurdles still stand between you and the closing table.

The biggest “if” is the property appraisal. The home you make an offer on must appraise for at least the sale price. If the appraisal comes in low, the lender won’t cover the difference, forcing you to either renegotiate with the seller or find the extra cash yourself.

Your final loan approval also depends on your financial life staying exactly the same. Any big changes—a new car loan, a job switch, or even a dip in your credit score—could derail the entire process. The best advice? Put your financial life on ice until the keys are in your hand.

Treat your pre-approval as the official start of your serious house hunt, not the end of your financing journey. It's the tool that lets you shop with real authority, backed by a lender who has already vetted your loan application documentation and employment history.

What Should You Do After You’re Pre-Approved?

Getting that pre-approval letter is a huge moment—definitely a reason to celebrate. But think of it as the official start of the race, not the finish line. Your most important job now is to protect the very financial stability that got you pre-approved in the first place.

Why? Because any big financial moves from this point forward can put your final loan approval at risk. The mortgage pre-approval process isn't over yet.

Hold Your Financial Horses

This is the part where you basically hit the pause button on your financial life. Lenders are going to pull your credit and review your file again right before you close. A last-minute drop in your credit score or a sudden spike in your debt-to-income ratio is the kind of surprise that can kill a deal.

So, put a freeze on things like opening new credit cards, financing a car (or even new furniture), or moving large, undocumented sums of cash into your bank account.

Keep Everything Exactly the Same

Lenders fell in love with the financial snapshot you gave them. Don't give them a reason to second-guess that decision. They want to see the exact same borrower at the closing table that they pre-approved weeks ago.

Even a seemingly positive change, like switching jobs for a pay raise, can create underwriting headaches and delay your closing. Consistency is your best friend right now.

Here’s a simple "don't" list to live by until you have the keys in your hand:

Don't apply for any new credit. No store cards, no auto loans, nothing.

Don't change your job. Your employment history needs to be stable.

Don't make large cash deposits. Lenders have to source every dollar, and un-sourced cash is a major red flag for income verification.

Don't co-sign a loan for anyone. From the lender's perspective, their new debt is now your new debt.

Team Up with an Agent and Start Looking

With that pre-approval letter in your hand, you're officially a serious buyer. It's the perfect time to find a great real estate agent. Your pre-approval shows them you’re ready to go and, just as importantly, it defines your budget. No more wasting time looking at homes you can't realistically afford based on your monthly income assessment.

Your pre-approval also gives your offer some serious muscle. When a seller sees you've already been vetted by a lender, they have more confidence that your financing won't collapse. In a hot market, that can easily be the edge you need. Just keep in mind that the loan is still dependent on a successful property appraisal.

As you start house hunting, it's smart to get a really granular view of your budget. Our free mortgage calculator can help you nail down what your monthly payments will look like.

The global mortgage market is projected to hit an incredible $18.2 trillion by 2032, which means lender requirements are only getting tighter. In this landscape, having a deep understanding of your own credit profile is more important than ever. It's what helps you strengthen your loan application documentation and lock in the best possible terms. You can discover more insights about the mortgage market and see where things are headed.

FAQ Question

- What is pre-approval for a home loan?

- A lender agrees to lend you a specific amount after evaluating your financial situation, providing a verified price range and a conditional commitment, subject to appraisal and final underwriting.

- How is pre-approval different from pre-qualification?

- Pre-qualification is a preliminary estimate based on self-reported information, while pre-approval involves providing documents and a credit check to confirm you are qualified for a specific amount.

- What documents will I need for pre-approval?

- Typically required are government IDs, proof of income (such as pay stubs, W-2s, or tax returns if self-employed), two years of tax returns, bank statements, asset documentation, and consent for a credit check.

- Does a higher credit score help my pre-approval?

- Yes, a higher score can improve eligibility, interest rate, and loan options. Lenders also consider debt-to-income ratio, employment history, and assets.

- How long does the pre-approval process take?

- Most lenders provide a decision within 24–72 hours after documents are submitted, though some may take longer.

- What is debt-to-income (DTI) and why does it matter?

- DTI compares monthly debt payments to gross monthly income. Lower DTIs are preferable as high DTIs can limit loan options or approval.

- Can I get pre-approved if I’m self-employed?

- Yes, but more documentation is usually required, such as tax returns for over two years, year-to-date profit-and-loss statements, and additional income verification.

- How long is a pre-approval letter valid?

- Validity varies by lender, often 60–90 days, sometimes up to 120 days. You might need to refresh it if your home search takes longer.

- Do I need a specific price range in mind to get pre-approved?

- Not necessarily, but having a target range helps the lender provide a realistic pre-approval and aids in confident shopping.

- Will pre-approval hurt my credit score?

- Yes, a hard credit inquiry will cause a temporary score dip. However, multiple inquiries for the same type of loan within 14–45 days are often treated as one inquiry by many lenders.

- Can I still shop around after getting pre-approved?

- Yes, you can compare rates from multiple lenders, but avoid opening new credit lines to protect your score.

- What factors can cause my pre-approval to be denied later?

- Changes in income, job status, new large debts, a credit score drop, or misreporting information can affect the final underwriting.

- Do I need to make a large down payment to get pre-approved?

- No, but larger down payments can improve approval odds and loan terms. Some loans require as little as 3–5% down, depending on the program and credit.

- What is the difference between pre-approval and a mortgage rate lock?

- Pre-approval is a lender’s conditional commitment, while a rate lock is an agreement to maintain the quoted interest rate for a set period, often linked to closing timelines after finding a home.

- What should I do after getting pre-approved?

- Begin house hunting within your approved range, maintain steady credit behavior, avoid new large debts, and once you find a home, work with your lender for final approval and closing.

Ready to make that pre-approval a reality? Score Machine gives you the AI-powered credit intelligence to see your financial profile the way lenders do. Get a clear, actionable plan to move forward with confidence and secure the best loan terms available. Analyze your credit report in seconds. Start your free analysis at https://thescoremachine.com.