Elevate Your Home Buying with a home loan consultant

Think of a home loan consultant as your personal guide through the often-confusing maze of mortgages. They're a strategic partner who works directly for you, not for a specific bank. Their job is to dive deep into your financial situation, then shop around with dozens of different lenders to find the loan that actually fits your life—saving you a ton of time and stress along the way.

What Is a Home Loan Consultant

Trying to secure a mortgage on your own can feel like navigating a thick forest without a map. You're surrounded by different lenders, loan types, interest rates, and fee structures, and it's easy to get lost. A home loan consultant is the seasoned guide who knows the terrain inside and out. They chart the best path to get you to your destination: homeownership.

It helps to think of them as a personal shopper for your finances. Instead of you spending countless hours researching banks and filling out application after application, they do all the heavy lifting. The process starts with them getting to know your unique financial picture, your long-term goals, and any potential hurdles.

Your Advocate in the Loan Process

Here’s the most important difference: a loan officer at a bank can only offer you their employer's products. A home loan consultant, on the other hand, has access to a huge network of lenders. This is a game-changer. A bank officer works for the bank; a consultant works for you. Their loyalty is to your best interest, not a corporate sales quota.

To give you a clearer picture, let's break down the key differences between going with an independent consultant versus a bank's in-house loan officer.

Home Loan Consultant vs Bank Loan Officer at a Glance

| Feature | Home Loan Consultant (Broker) | Bank Loan Officer |

|---|---|---|

| Loyalty | Works for you, the borrower. | Works for the bank/lender. |

| Product Access | Access to a wide network of lenders and diverse loan products. | Limited to the products offered by their specific institution. |

| Flexibility | Can find niche lenders for complex situations (e.g., self-employed). | Must adhere to the bank's strict lending guidelines. |

| Negotiation | Negotiates rates and terms on your behalf across multiple lenders. | Offers the bank's established rates and terms. |

| Compensation | Typically paid a commission by the lender upon closing (or a flat fee). | Salaried employee, often with a bonus structure based on loan volume. |

As the table shows, the independent model offers a completely different level of service and choice, which can make a massive difference in the loan you ultimately get.

This personalized approach comes with some major advantages:

- Wider Access to Loans: They can connect you with wholesale lenders, credit unions, and banks you’d probably never find on your own.

- Expert Negotiation: They know the market and can negotiate rates and terms on your behalf, potentially saving you thousands over the life of your loan.

- Creative Problem-Solving: If you have a tricky financial situation, like being self-employed or having a less-than-perfect credit score, they know which lenders are more willing to work with you.

A home loan consultant acts as a buffer between you and the lender. They translate the complex jargon, handle the mountain of paperwork, and make sure the entire process flows smoothly from the first application to the final closing. They are your dedicated expert in a very high-stakes transaction.

The mortgage industry is always in flux. The number of active loan officers recently hit 221,161, and the broker segment saw a significant 12.5% increase. This trend suggests that more and more borrowers are seeing the value in the independent consultant model, especially in a market with unpredictable interest rates. You can learn more by digging into the latest mortgage market trends.

By partnering with a home loan consultant, you’re not just getting a loan—you’re gaining an ally who is committed to your financial well-being. They provide the clarity and confidence you need to make one of the biggest financial decisions of your life, helping you sidestep common mistakes and secure a loan that truly works for you.

What a Home Loan Consultant Does for You

Think of a good home loan consultant as your personal financial quarterback for the home-buying game. They're not just pushing paperwork; they’re your strategic partner, guiding you through the entire mortgage maze from start to finish. Their job is a mix of deep financial analysis, insider market knowledge, and sharp negotiation.

It all starts with a financial deep-dive. Your consultant will comb through your income, assets, debts, and credit history to get a real, unvarnished look at your borrowing power. This isn't just about plugging numbers into a calculator; it's about understanding the story your finances tell a lender.

From Analysis to Application

Once they have a crystal-clear picture of your financial health, the real matchmaking begins. Consultants have access to a huge network of lenders—from the big national banks to smaller, specialized credit unions. They sift through countless mortgage products to find the one that truly fits your life, whether that’s a conventional 30-year fixed, an FHA loan, or something more unique for a one-of-a-kind property.

This is where you really see their value. They meticulously prepare your loan application, making sure it’s packaged in a way that underwriters will love. This proactive approach sidesteps those frustrating delays and endless requests for "just one more document." Every 'i' is dotted, and every 't' is crossed long before your file lands on a lender’s desk.

A consultant's real job is to make you look like the strongest, most reliable borrower possible. They become your advocate, translating your financial life into a compelling story that gives an underwriter the confidence to say "approved." That advocacy can be the difference between a smooth closing and a soul-crushing rejection.

Negotiation and Closing Your Loan

After your application is in, your consultant shifts gears and becomes your negotiator. They go to bat for you, working with the lender to lock in the best possible rates and terms. Often, they can find savings or perks you'd never get access to on your own. This is especially true when the market is moving quickly.

They're navigating a complex financial world. For instance, agency mortgage securitizations recently jumped 10.6% year-over-year to $301 billion, a move almost entirely fueled by a massive 63% spike in refinances. A sharp consultant understands what these mortgage and housing trends mean and can use that knowledge to your advantage.

Ultimately, a great home loan consultant turns what can be an intimidating, confusing process into a clear, manageable journey. From that first financial review to the moment you get the keys, they provide the expert guidance that makes the path to homeownership that much smoother. It all starts with being prepared, which is why knowing your own credit readiness is such a powerful first step.

Improving Your Chances of Loan Approval

A great home loan consultant does more than just find you a loan; they work with you to become the kind of applicant lenders are excited to approve. Think of them as your personal financial strategist. They meticulously review your entire profile to make sure it’s presented in the strongest possible light, turning you into a truly 'fundable' candidate.

This whole process usually kicks off with a deep dive into your credit report. They’re on the hunt for common errors, figuring out the best ways to reduce debt to positively impact your score, and spotting any quick wins that could give you an immediate boost. It’s all about being proactive and clearing away potential red flags before a lender’s underwriter ever lays eyes on your file.

Gaining an Underwriter's Perspective

To really get an edge, the best consultants are now using sophisticated tools that give them a peek behind the curtain. They use platforms that show them your financial profile from an underwriter's point of view, going way beyond a simple credit score to see what a lender really cares about. This allows them to zero in on specific risks and strengths with laser-like accuracy.

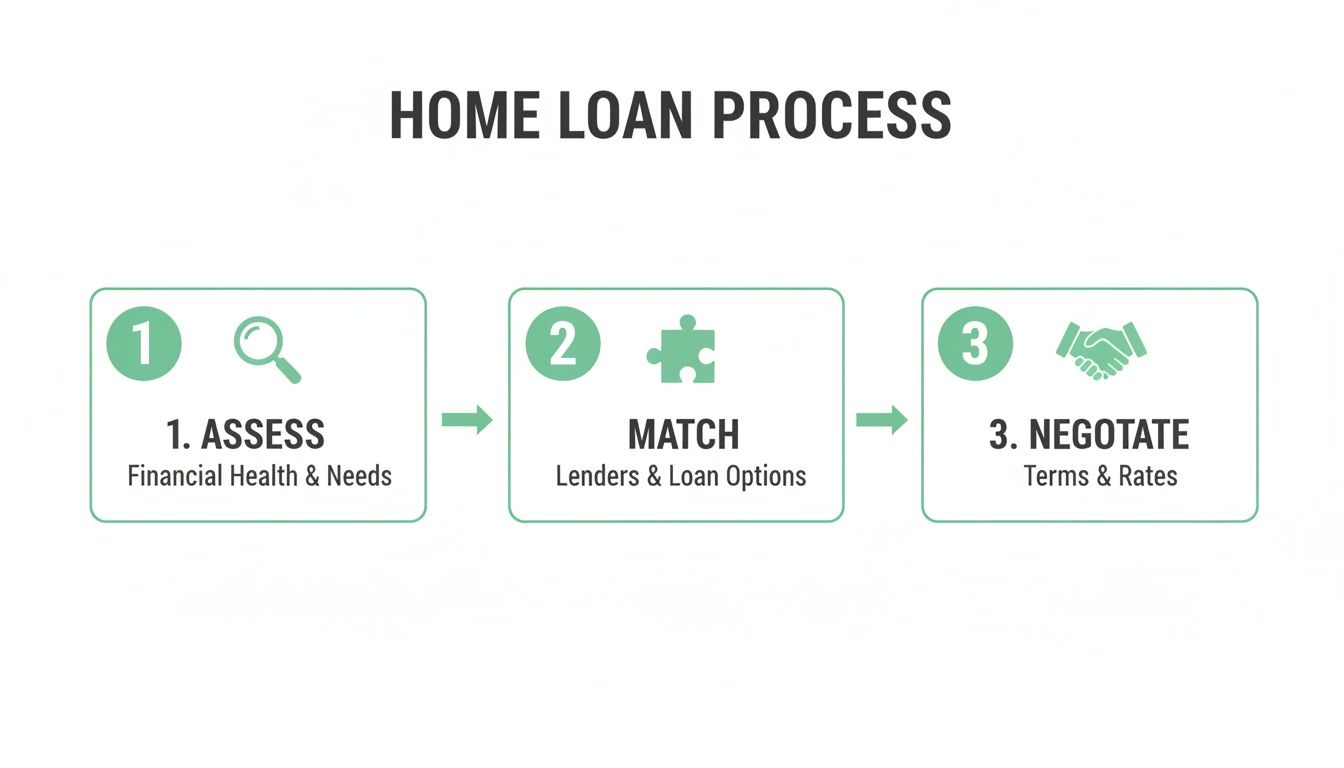

This infographic breaks down the fundamental three-step process a consultant uses to get you from start to finish.

As you can see, a solid application always starts with a thorough assessment, followed by smart matching and, finally, skilled negotiation.

One of the standout tools in this arena is Score Machine. Its AI-driven analysis provides your consultant with an instant, data-backed roadmap of your fundability. It doesn't just spit out a number; it tells the story behind it, highlighting the exact details that might make an underwriter pause.

By simulating the underwriting process before you ever submit an application, a home loan consultant can tackle potential problems head-on. You walk into the lender's office with a profile that’s already been polished for approval, which massively cuts down the risk of getting denied.

This level of detailed summary helps a consultant give you precise, step-by-step guidance to make your application as strong as it can possibly be.

From Advice to Action

Armed with these deep insights, your consultant can give you incredibly specific advice. Instead of just saying, "you should pay down your debt," they can show you exactly which credit card to pay off and by how much to get the biggest bang for your buck on your credit score. This targeted strategy saves you time and money by focusing your efforts where they'll have the most impact. You can learn more about how this works by checking out these expert tips on strategic loan preparation.

Ultimately, this modern approach to loan readiness makes the whole process smoother and more successful for everyone. For a mortgage brokerage, having consultants who can pre-vet clients this effectively is a huge advantage. It means they’re submitting cleaner, stronger loan packages that are far more likely to sail right through underwriting. This slashes rejection rates, saves a ton of time on back-and-forth communication, and builds a rock-solid reputation. By turning guesswork into a science, a skilled home loan consultant makes getting a mortgage more efficient and predictable.

How the Pros Stack the Deck for Loan Approval

At the end of the day, a funding company or mortgage brokerage lives and dies by one thing: closed loans. In a market this crowded, you can't just be good; you have to be ruthlessly efficient and surgically precise. This is where the real advantage comes from—ditching the old-school manual slog for a smarter, data-driven approach to credit analysis.

When a home loan consultant has a serious tool like Score Machine in their corner, their entire process changes. They're no longer just glancing at a credit score and making an educated guess. Instead, they get an immediate, deep-dive analysis of a client's real-world fundability. This completely flips the script on how loan applications are built and submitted.

From "Submit and Pray" to Data-Backed Confidence

The old method for preparing a loan application was basically a game of chance. You'd package it up, send it off, and then just wait for the underwriter's list of problems to roll in. Modern platforms, however, let a consultant get ahead of the game. They essentially run a full underwriting simulation before the file ever lands on a lender's desk.

Score Machine's analysis is designed to spot the exact same red flags that would make a human underwriter hesitate. It can pinpoint hidden risks buried in a credit profile, double-check data for inconsistencies, and even find overlooked strengths you can build the application around. Think of it as getting the underwriter's notes in advance.

For any funding operation, this is huge. It means your consultants can craft a targeted, step-by-step game plan for every single client before submission. This pre-flight check all but eliminates the easily avoidable rejections, which saves an incredible amount of time, money, and headaches for everyone.

By cleaning up these potential issues on the front end, consultants can send lenders a file that’s not just complete, but optimized for a fast "yes." This is how you systematically increase your closing ratio.

Working Smarter, Not Harder, for Better Margins

When your team can instantly and accurately gauge a client's real shot at funding, the whole operation just runs smoother. They waste less time on files that are dead on arrival or chasing down endless paperwork for a difficult approval. Instead, they can focus their energy on clients who are genuinely ready to go.

This efficiency boost pays off in a few critical ways:

- Increased Funding Volume: By accurately pre-qualifying more applicants and submitting stronger files, funding companies directly increase their loan approval rates. More approved loans mean more closed deals and a direct increase in revenue.

- Lower Operating Costs: Fewer rejections mean fewer wasted hours and less administrative drag. The business runs leaner and more profitably.

- Happier Clients, More Referrals: Nothing builds trust like getting results. When clients see a clear plan that actually leads to an approval, they become your best source of new business.

A home loan consultant who uses this kind of technology is simply a bigger asset to the company. They close more loans, which makes clients happy and drives revenue directly to the bottom line. This isn't just about tweaking one loan application; it's about building a more predictable and profitable business model. By turning messy credit data into a clear roadmap for approval, you gain a massive competitive edge that grows your revenue and cements your reputation as the team that gets it done.

How to Choose the Right Home Loan Consultant

Picking the right home loan consultant is a make-or-break decision on the road to buying a home. Think of this person as more than just a paper-pusher; they're a crucial part of your team, a strategic partner who should be in your corner from day one. To hire with confidence, you need to ask the right questions upfront and make sure you’re bringing on a real pro who’s invested in your success.

That first conversation is your interview—and you’re the one in charge. You’re trying to get a feel for their experience, how they communicate, and most importantly, what their game plan is for making your loan application bulletproof. A great consultant is transparent, knows their stuff, and can lay out a clear strategy for getting you the keys to your new home.

Key Questions to Ask a Potential Consultant

Don't just show up and hope for the best. Go into that first meeting with a list of questions. Their answers will tell you everything you need to know about their skills and whether they're the right person for your unique situation. You can start with the basics, but don't hesitate to press them on their specific methods and the technology they use to give their clients an advantage.

Here are a few essential questions to get the ball rolling:

- Experience with Your Situation: Ask, "How many clients have you helped with a financial profile like mine?" This is critical if you're self-employed, have complex income streams, or are still building your credit. You don't want to be their guinea pig.

- Lender Network: Find out what kind of lenders they work with. A consultant with a broad network of lending partners can shop around for the best fit, not just push the one or two products they know best. More options are always better for you.

- Communication Style: This one’s simple but so important: "How do you keep your clients in the loop?" You need someone who is proactive and clear. The last thing you want is to be left in the dark, wondering where your application stands.

Inquiring About Fees and Technology

There should be zero mystery about what this is going to cost you. Ask for a crystal-clear breakdown of their fee structure so you don't get hit with unexpected charges down the line. A consultant who is on the level will have no problem explaining exactly how they get paid and what you can expect to pay.

This is also a great time to dig into their process for getting you "mortgage ready."

A truly modern consultant does more than just pull your credit score and hope for the best. Ask them, "What tools do you use to analyze my credit and prepare my file for underwriting?" This question is what separates the old-school players from the pros.

Experts who use sophisticated analysis platforms can see your application through an underwriter's eyes. They can spot the exact red flags that might cause trouble and give you a concrete action plan to fix them before you apply. This data-first approach seriously boosts your approval odds.

While you're getting a handle on the numbers, it's also a good idea to play with a free online mortgage calculator to get a ballpark idea of your payments. Ultimately, finding a consultant who pairs years of hands-on experience with powerful modern tools is your ticket to a much smoother and more successful home-buying journey.

Common Questions About Home Loan Consultants

Deciding to work with a home loan consultant is a big move, so it's only natural to have a few questions before diving in. You need to understand how they work, what they can realistically do for you, and the best time to bring them into your corner. Let's break down the most common questions we hear from homebuyers.

The first thing on most people's minds? Money. There's a common myth that you'll have to write a big check directly out of your own pocket, but that's rarely how it works.

How Do Home Loan Consultants Get Paid?

Typically, a home loan consultant is paid a commission by the lender, but only after your loan successfully closes. This is called lender-paid compensation, and it's usually a small percentage of the total loan amount. In less common situations, a borrower might pay the consultant directly.

Any good consultant will be crystal clear about their fees from the very beginning. They’ll walk you through a Loan Estimate document that itemizes every single cost, so there are no surprises. This structure means their success is directly tied to yours—if you don't get the loan, they don't get paid.

Can a Home Loan Consultant Guarantee I’ll Be Approved?

No one can ever guarantee a loan approval. The final say always rests with the lender's underwriter. However, a consultant's entire job is to stack the deck in your favor and give you the absolute best shot at getting that "yes."

They do this by meticulously preparing your application, finding the right lender for your specific profile, and positioning you as a rock-solid borrower. They take a process that can feel like a gamble and turn it into a calculated strategy.

Think of it this way: an expert consultant doesn't just submit your application; they essentially pre-underwrite it. They hunt down and resolve potential red flags long before the lender's team ever lays eyes on your file. This proactive work is what dramatically boosts your odds of a fast, smooth approval.

This is where their real value lies. They know exactly what lenders are looking for and how to navigate their unique requirements.

Should I Just Go Directly to My Bank Instead?

You can certainly go to your bank, but remember, they can only offer you their products. That’s a pretty limited menu. A home loan consultant, on the other hand, has relationships with dozens of different lenders, giving them access to a huge marketplace of loan options.

This allows them to shop around on your behalf to find not just a better rate, but a loan program that genuinely fits your life and financial goals. They work for you, not one specific bank, which means their advice is focused entirely on what's best for you.

When Is the Right Time to Contact a Home Loan Consultant?

The sooner, the better. Ideally, you should reach out months before you even start seriously browsing home listings. This gives you and your consultant plenty of runway to get your financial ducks in a row.

Getting started early allows them to review your finances, get you pre-approved, and spot any credit issues that need attention. This prep time is your secret weapon, turning a stressful, reactive process into a calm, strategic one. You'll be a much stronger, more confident buyer when you're finally ready to make an offer.

Ready to see how your credit profile looks through an underwriter's eyes? Score Machine delivers the deep analysis and clear, actionable steps you need to build a stronger application. Our platform gives you the insight to boost your fundability and approach lenders with total confidence. Get your instant credit analysis today at thescoremachine.com.