Your Score Dropped and You Don't Know Why. Let's Fix That.

You check your credit score and it's down 40 points. You didn't miss a payment. You didn't open new accounts. Nothing changed — except the number.

Sound familiar? You're not alone. Most people have no idea how their credit score actually works, and that blind spot costs real money — higher interest rates, denied applications, missed opportunities that add up over a lifetime.

Here's the truth: your credit score isn't random. It follows specific rules. Once you understand them, you take back control. That's what this article is for — the actual mechanics lenders look at, not the recycled "pay your bills on time" advice you've heard a thousand times.

Your Score Isn't a Grade. It's a Risk Prediction.

Your credit score doesn't measure how responsible you are. It predicts how likely you are to fall 90+ days behind on a payment in the next two years. That's it. Higher score = lower risk = better terms.

FICO powers roughly 90% of U.S. lending decisions. VantageScore is the other major model. Both use a 300–850 scale.

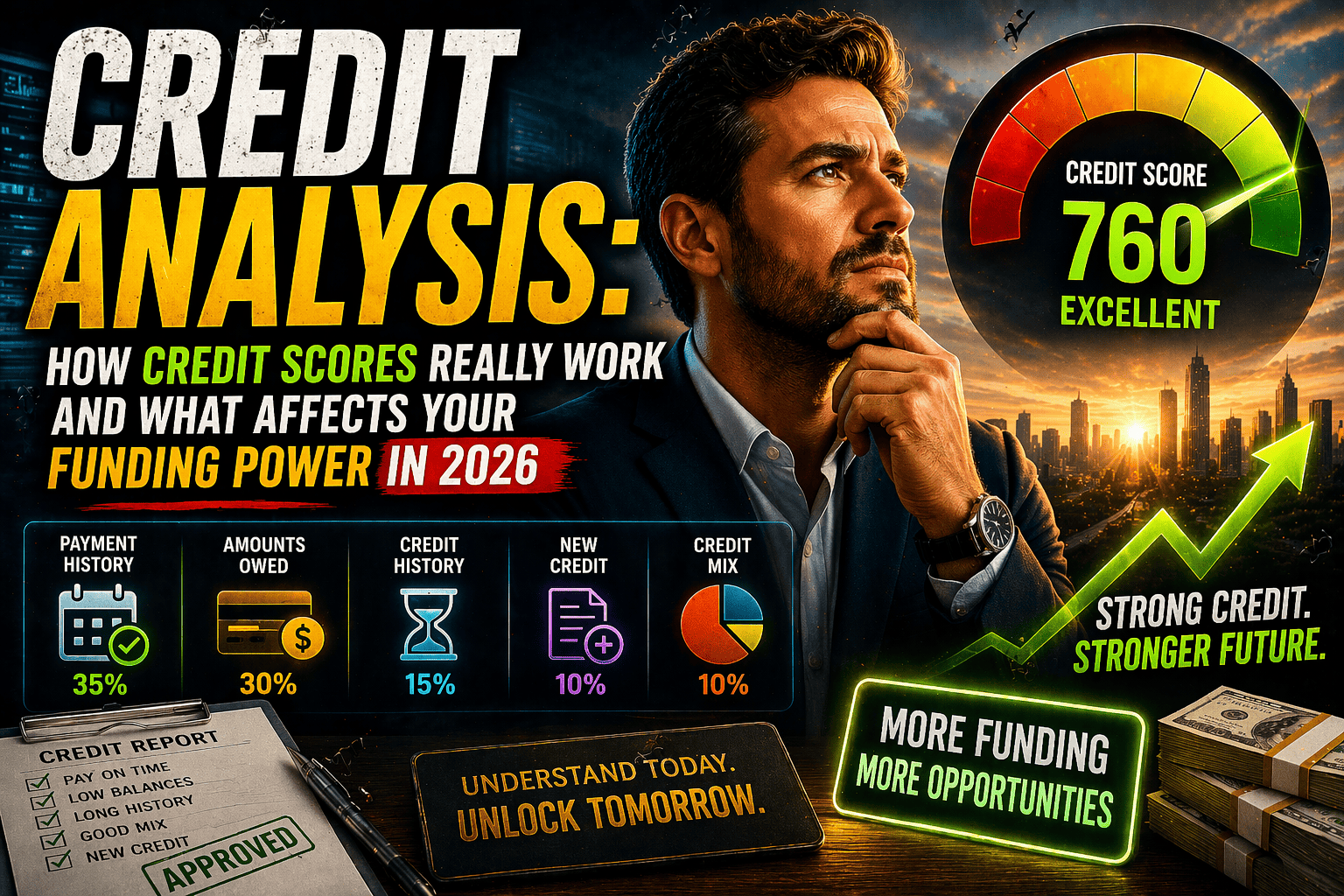

Equifax breaks down the five ingredients FICO uses:

Payment History (35%) — The biggest factor. Have you paid people back? A single 30-day late payment can drop a high score by 50–100 points. Bankruptcies and collections sit on your report for 7–10 years under the FCRA. The kicker? The higher your score was, the harder a late payment hits — because the deviation from your pattern is a louder alarm.

Credit Utilization (30%) — What percentage of your available credit are you using? You've heard "keep it under 30%." That's not a target — it's a ceiling before things get ugly. FICO's data shows top scorers keep utilization under 6%. The FICO Credit Insights report found average utilization climbed to 35.5% in 2025, with Federal Reserve data showing average card debt at $6,360 per person. And utilization is measured per-card and overall — maxing out one card still triggers a risk signal.

Length of Credit History (15%) — How old are your accounts? Longer history = more data = more confidence in the prediction. FICO says top scorers opened their first account ~25 years ago. That college credit card you never use? It's quietly helping. Don't close it.

New Credit Inquiries (10%) — Hard inquiries from applications can ding your score if they pile up. Good news: rate-shopping for the same loan type within 14–45 days counts as one inquiry. Soft inquiries (checking your own score, pre-approvals) don't affect anything.

Credit Mix (10%) — Lenders like seeing you handle both revolving credit (cards) and installment loans (mortgage, auto). But at 10%, don't open accounts just to diversify — the inquiry and lower account age usually cost more than the mix boost adds.

What Lenders Are Actually Doing in 2026

The landscape has shifted. Here's what matters right now:

Average FICO is 715 — down two points from 2024, largely from student loan delinquencies hitting reports again after years of pandemic-era pauses (FICO data).

90+ day delinquencies jumped from 7.4% to 8.3% in early 2025 — first time surpassing pre-pandemic levels. CFPB data suggests this keeps climbing through 2026.

The credit middle class is shrinking. The 600–749 score range dropped from 38.1% of the population in 2021 to 33.8% by 2025. People are migrating toward the extremes.

| Risk Tier | Score Range | Credit Card APR | What It Means |

|---|---|---|---|

| Super-Prime | 740+ | 17–21% | Best rates, easiest approvals |

| Prime | 680–739 | 21–24% | Solid access, competitive terms |

| Near-Prime | 620–679 | 24–27% | Higher costs, conditional approvals |

| Subprime | 580–619 | 27–30%+ | Limited to secured/specialty products |

| Deep Subprime | Below 580 | 30%+ or declined | Rebuilding territory |

Average credit card APR sits around 22.30% for accounts carrying balances (Federal Reserve). New offers average 23.77% (LendingTree). The Fed's 2025 rate cuts helped slightly, but issuers have been slow to pass savings along.

On DTI: lenders want you under 36%. With U.S. card debt at $1.28 trillion and student loans back, managing DTI is critical.

New Scoring Models Worth Knowing

FICO 10T is gaining traction with lenders. It uses trended data — looking at how your balances moved over 24 months, not just today's snapshot. Paying things down steadily? You get rewarded. Balances creeping up? Steeper penalty than older models.

VantageScore 4.0 factors in rent, utilities, and telecom payments — huge for anyone with a thin credit file. Fannie Mae and Freddie Mac now accept both models for mortgage underwriting, opening doors that were previously locked.

How Age Changes the Game

The FICO Credit Insights report and Experian show the Silent Generation averages ~760 while Gen Z sits at ~681 with the biggest year-over-year drop of any age group. About 34% of consumers under 30 carry student loans (vs. 17% overall), and nearly half of Gen Z who faced income loss last year turned to credit cards or Buy Now, Pay Later to get by. If you're young, the priority is simple: build the payment habit now. History length comes with time — but bad habits compound fast.

How Reporting Actually Works

Your creditors send data to Equifax, Experian, and TransUnion about once a month using the Metro 2 format. Not all creditors report to all three bureaus, which is why your scores can differ. Your utilization snapshot happens at the time of reporting — usually your statement closing date. Pay down your balance before the statement closes, and the bureau sees a lower number. I've seen people gain 20–30 points from this timing trick alone. Pull your free reports yearly at AnnualCreditReport.com and check for errors — they're more common than you'd think.

The Real Dollar Cost

Take a $300,000 mortgage over 30 years. A borrower at 740 might get 6.5% — roughly $382K in total interest. Someone at 580 might see 8%+ — pushing interest past $492K. That's $110,000 more for the same house. That's what credit health actually costs.

Five Myths Quietly Wrecking Your Credit

"Checking my score hurts it." Nope. Soft inquiry. Zero impact. A FICO survey found 45% check monthly. The other 55% should start.

"Carrying a balance builds credit." It just costs you interest. Pay in full every month.

"Close cards you don't use." Don't. You lose available credit (higher utilization) and eventually lose account history. Leave them open.

"All debt is the same." Revolving debt (cards) is viewed as riskier than installment loans (mortgage, auto). FICO's research shows people now prioritize car payments over mortgages and student loans.

"I have one credit score." You might have 30+. FICO makes different versions for different industries. Each bureau holds slightly different data. The CFPB confirms — there's no single "true" score.

Seven Moves You Can Make Today

- Pull your reports at AnnualCreditReport.com. Dispute errors — bureaus must investigate within 30 days.

- Pay before your statement date (not the due date) to report a lower utilization.

- Auto-pay minimums on everything. One forgotten payment does more damage than months of good behavior.

- Get added as an authorized user on a family member's old, clean account.

- Use pre-qualification tools (soft pulls) before formally applying for credit.

- Keep old accounts open — the age and available credit both help your score.

- Diversify your credit mix gradually — only when it makes financial sense.

FAQ

Good score in 2026? 670+ is "good," but you want 680+ for prime products and 740+ for best rates. Average is 715 (FICO).

How often does it change? Recalculated every time it's pulled. Underlying data updates monthly.

Does income affect my score? No — but lenders look at it separately for DTI calculations.

How long do negatives last? Seven years for most items. Bankruptcies: 7–10 years. Inquiries: 2 years (affect score for ~12 months). FCRA rules.

How do I fix errors? Dispute with Equifax, Experian, or TransUnion directly. Escalate to the CFPB if unresolved.

Further Reading: Credit Analysis: How Credit Scores, Debt & Financial Behavior Impact Your Funding Power

About the Author

Ali Badi — CTO, Credit Risk Strategist & Funding Analyst

Ali has spent years in the weeds of credit risk and fintech. Every article at The Score Machine has one goal: translate the stuff lenders deal with behind closed doors into language that helps real people make better decisions. The Score Machine is an AI-powered credit analysis and funding readiness platform — built to help you understand what lenders are really looking at.

Disclaimer: This article is for educational purposes only — not financial, legal, or lending advice. Based on publicly available data as of early 2026. Consult a qualified professional before making credit or lending decisions. The Score Machine is not a lender, broker, or credit repair company.