Ever been stopped dead in your tracks by a low credit score when applying for a loan? It's a frustrating roadblock, and building credit the old-fashioned way can feel like watching paint dry. For many, it takes years of perfect financial discipline.

But what if you could add years of positive credit history to your report, almost overnight?

This is exactly where tradelines come in. Think of your credit report as your financial resume. If it's a little thin or has a few smudges, getting the best "jobs"—in this case, loans with great rates—is tough. A tradeline is like adding a seasoned professional’s stellar work history to your own resume. Suddenly, you look a lot more experienced and reliable to lenders.

How Tradelines Give Your Credit Score an Instant Lift

The core strategy involves becoming an authorized user on someone else's well-managed credit card. You pay a fee, and their positive payment history and high credit limit get added to your credit report. This can give your score a serious jumpstart by beefing up key factors like your payment history and credit utilization ratio.

The Core Concept of Credit "Piggybacking"

At its heart, using an authorized user (AU) tradeline is a form of credit "piggybacking." You're essentially borrowing the good reputation of an established credit account. Once you're added, the entire history of that account—its age, credit limit, and perfect payment record—often gets reported to the credit bureaus as if it were your own.

This one simple move can have a massive and immediate impact on the two most important factors in your FICO score.

Payment history alone accounts for a whopping 35% of your FICO score, so adding an account with years of on-time payments is a game-changer, especially for someone with a thin file. On top of that, adding a high-limit card with a low balance can drastically lower your overall credit utilization, which makes up another 30% of your score. Getting that utilization number below the magic 30% threshold can often produce a score boost of 20 to 100 points in just 30-60 days.

You can get a deeper look into how this strategy plays out at Priority Tradelines.

A Quick Comparison of Tradeline Types

While authorized user tradelines are the most popular way to get a quick credit boost, it’s good to know what else is out there. To help you see the bigger picture, here’s a quick breakdown of the different types of tradelines and how they work.

Tradeline Types and Their Potential Impact

| Tradeline Type | How It Works | Best For | Potential Score Boost |

|---|---|---|---|

| Authorized User (AU) | You pay to be added to a seasoned credit card with perfect history. | Individuals with thin credit files or low scores needing a rapid boost. | High |

| Primary Tradeline | An account (loan, credit card) opened in your own name. | Anyone looking to build a long-term, sustainable credit history. | Gradual |

| Seasoned Tradeline | A term often used for an older AU tradeline with a long history. | Maximizing the "age of credit history" factor in your score. | Very High |

This table gives you a bird's-eye view, but understanding these distinctions is key. Each type serves a different purpose, and knowing which one fits your situation is the first step toward making a smart decision. Now, let’s dig a little deeper into the mechanics of how this all works.

How Tradelines Actually Boost Your Credit Score

Think of your credit report as a resume for lenders. If it's thin or has a few blemishes, you'll have a tough time getting approved for anything significant. Adding a well-chosen tradeline is like getting a glowing, ten-year work history from a Fortune 500 executive added to your own resume. Suddenly, you look far more established, reliable, and trustworthy in the eyes of a lender.

This isn't just smoke and mirrors. A high-quality authorized user (AU) tradeline injects positive data directly into the most heavily weighted parts of your credit score. It's a strategic move designed to create an immediate, positive impact where it counts the most.

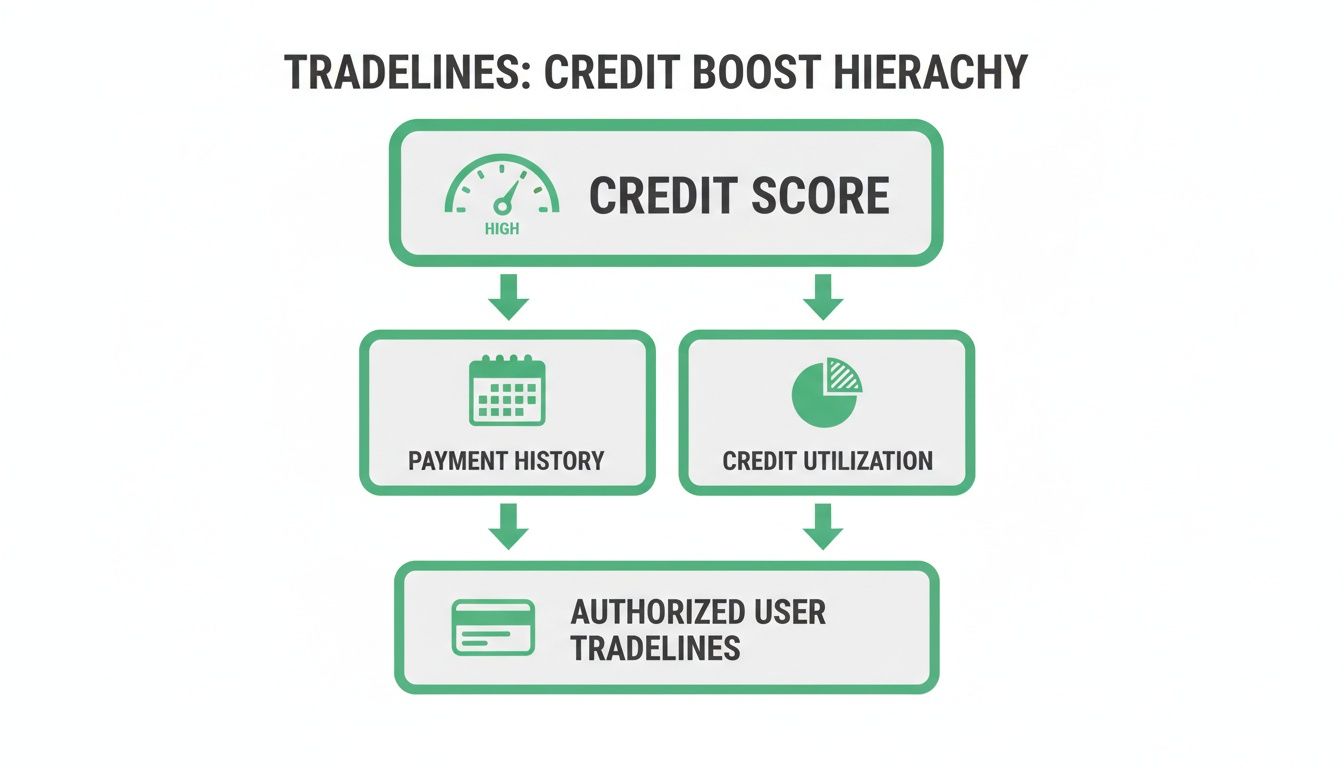

This flowchart shows exactly how a tradeline targets the most influential parts of your credit score.

As you can see, the whole point is to beef up your payment history and slash your credit utilization—the two biggest pieces of the credit score pie.

The Heavy Hitters: Payment History and Credit Utilization

When it comes to your credit score, two factors tower above the rest: your payment history (35%) and your credit utilization (30%). Combined, they account for a whopping 65% of your FICO score, and this is precisely where tradelines do their best work.

When you become an authorized user, the entire history of that account gets copied onto your credit report.

Imagine a credit card that has been open for 10 years with a perfect record of on-time payments. That entire decade of positive history is instantly grafted onto your file, which can have a massive impact on the most important scoring factor.

At the same time, the tradeline adds its credit limit to your total available credit, but ideally with a very low balance. For instance, getting added to a card with a $20,000 limit that only has a $500 balance immediately drops your overall credit utilization ratio. This one move can take you from a high-risk zone (say, over 50% utilization) down to a much healthier level (under 10%), showing lenders you’re not financially overextended.

A tradeline essentially helps overwrite a weak history with a strong one. It also dilutes high balances with a large new credit limit, giving you an immediate and powerful lift in the two most significant scoring categories.

Strengthening Your Credit Age, Mix, and New Inquiries

Beyond the big two, tradelines also give the other components of your FICO score a nice bump.

The length of your credit history (15%) gets a serious upgrade. If your oldest account is only two years old, adding a 15-year-old tradeline can dramatically increase the average age of your accounts overnight. This makes your credit profile look much more mature and stable.

This is especially powerful for anyone building credit from the ground up. And while credit mix (10%) is about having different types of accounts (like credit cards and installment loans), adding a strong revolving tradeline can provide a solid foundation. An old account with a perfect payment record can remain on your report for up to 10 years even after being closed, which provides a long-lasting benefit for people rebuilding after bankruptcy or new immigrants establishing their financial footing. You can explore more about these long-term benefits and how they apply in different situations.

Finally, there’s new credit (10%). Adding a tradeline is a savvy way to strengthen your credit file without the "hard inquiry" that comes from applying for new credit yourself. This allows you to build a stronger profile first, which greatly improves your odds of getting approved when you do decide to apply for your own primary accounts. It’s a calculated first step toward long-term financial success.

How to Choose a Reputable Tradeline Company

So, you understand what tradelines are and how they can work. That’s the easy part. Now comes the real challenge: finding a company you can actually trust.

The tradeline world is a bit like the Wild West—it's largely unregulated. That means for every seasoned expert, there's a shady operator just waiting to take your money. Choosing wrong won't just leave you with an empty wallet; it could seriously damage your credit and put your personal information at risk.

This is where you need to be sharp. Picking a provider for your tradelines for credit boost isn't like choosing a new pair of shoes. The stakes are much, much higher.

Imagine shelling out hundreds, or even thousands, for a top-tier tradeline, only to watch your credit report and see... nothing. Or worse, what if that "company" you handed your Social Security number to was just a front for identity thieves? These aren't just hypotheticals; they are very real risks.

The Risks of Working With the Wrong Provider

The promise of a quick credit fix can make it easy to overlook the red flags. Before you jump in, you absolutely need to understand what can go wrong.

Here are the most common nightmares you want to avoid:

- Ghost Tradelines: You pay the fee, but the tradeline never actually posts to your credit file. The company gives you the runaround with excuses until they eventually just disappear, leaving you with nothing to show for your investment.

- Identity Theft: Some outfits are just scams designed to harvest your sensitive data. They have no intention of ever providing a tradeline; they just want your information to exploit later.

- Toxic Tradelines: A truly dishonest provider might stick you on a tradeline with a history of late payments or a maxed-out balance. This is the opposite of a boost—it's a direct hit to your credit score.

- Getting Flagged by Lenders: Banks and lenders are getting smarter about spotting credit manipulation. If you work with a sketchy company, your file could get flagged, making it even harder to get approved for loans down the road.

While adding an authorized user is perfectly legal, the business of buying and selling that access lives in a gray area. This is why doing your homework isn't just a good idea—it's your best defense. A legitimate company will be upfront and offer solid guarantees.

Your Vetting Checklist for Tradeline Companies

To navigate this landscape safely, you need a clear, methodical way to check out any company you're considering. Think of it as a pre-flight inspection before you trust them with your financial future. A solid, trustworthy company should pass this checklist with flying colors.

The table below is your guide. Use it to compare potential providers side-by-side. If a company raises more than one of these red flags, it's probably best to walk away.

Tradeline Provider Vetting Checklist

Before you sign any contracts or send any money, run the company through this checklist. A reputable provider will have no problem meeting these standards.

| Evaluation Criteria | What to Look For | Red Flags to Avoid |

|---|---|---|

| Business History & Reputation | An established business with a physical address, a professional website, and real, verifiable customer reviews. | A brand-new company with no history, a PO box for an address, or testimonials that sound fake and generic. |

| Transparency and Pricing | Clear, upfront pricing with zero hidden fees. Everything should be laid out in a written agreement before you pay. | Vague price lists, high-pressure sales calls pushing you to "act now," or a refusal to provide a detailed contract. |

| Customer Service and Support | Real people you can talk to on the phone or via email who know what they're talking about and answer questions directly. | Unresponsive support, evasive answers, or companies that will only communicate through a website chat box. |

| Posting Guarantee | A crystal-clear, written guarantee that the tradeline will post to at least two of the three major credit bureaus. | No guarantee is offered, or the "guarantee" is full of loopholes and conditions that make it practically useless. |

| Contract and Agreement | A formal, legally sound contract that spells out the exact service, the specific tradeline, the total cost, and the guarantee terms. | No contract at all, or just a simple invoice that lacks any real terms and conditions to protect you. |

By putting every potential company through this level of scrutiny, you dramatically lower your risk. A legitimate business will be proud to show you its track record and will be completely transparent about its process and pricing.

Don't ever be afraid to ask tough questions—your financial health is on the line. A quality provider will see your diligence not as a hassle, but as the mark of a serious and responsible client.

How Funding Companies Use Score Machine to Increase Approvals

For any funding company, broker, or loan officer, a denied application is a lost opportunity. Each "no" represents lost revenue and a client you couldn't serve. But many of these declined applicants aren't dead ends; they're "near-misses"—clients who are just a few strategic steps away from qualifying. This is where a tool like Score Machine can fundamentally change a funding business, turning denials into a pipeline of future approvals.

Instead of simply delivering bad news, funding professionals can become strategic partners. By analyzing a client's credit file with Score Machine's AI, they can pinpoint the exact weaknesses that led to the denial—problems that a targeted tradeline for credit boost is perfectly designed to fix. This transforms the business model from a simple gatekeeper to a problem-solver, unlocking a significant new stream of revenue from previously unqualified leads.

From Automatic Denials to Actionable Funding Plans

The traditional funding process is binary: approved or denied. Score Machine introduces a profitable third option: "Not yet, but here’s how." The platform's AI simulates a lender's underwriting perspective, identifying the specific reasons for a denial. It doesn't just say the score is too low; it reveals why—high credit utilization, a thin file, or insufficient credit history.

Once these issues are diagnosed, the funding company can provide the client with a clear, step-by-step plan for approval. This might involve recommending a specific seasoned tradeline to increase the age of their credit history or a high-limit tradeline to lower their utilization ratio. This consultative approach not only salvages a potential deal but also builds immense client trust and loyalty.

Score Machine provides a visual dashboard of the credit file, making complex data easy to understand.

This snapshot allows a funding professional to instantly see what an underwriter sees, highlighting the exact obstacles holding an applicant back. With this data, they can confidently recommend the right tradeline to solve the specific problem, increasing the client's chances of getting funded.

Creating New Revenue and Boosting Closing Rates

Integrating Score Machine into the workflow is a direct path to business growth. By guiding "near-miss" clients through a credit improvement plan, a funding company can achieve several key objectives. First, it significantly expands the pool of fundable applicants by converting a large portion of previously denied leads.

Second, it creates a new revenue stream. Offering in-depth credit analysis and strategic planning as a value-added service positions the company as a full-service consultancy, not just a transaction-based business.

By turning a denial into a concrete action plan, you prevent that lead from going to a competitor. You keep the client within your ecosystem, guide their credit improvement, and ensure that when they are ready for funding, they return to you.

This strategy leads directly to higher closing rates. When a client comes back with a stronger credit profile built on the company's expert guidance, their likelihood of approval skyrockets. This improves key performance metrics, strengthens relationships with lenders, and builds a reputation as a firm that gets deals done. It’s a powerful cycle that transforms lost opportunities into predictable revenue.

Using Score Machine to Plan Your Credit Boost

Adding a tradeline to your credit report without a clear strategy is like taking a road trip without a map. Sure, you'll end up somewhere, but it's probably not where you wanted to go. This is exactly where guesswork gets people into trouble and where data-driven planning completely changes the game. Using a tool like Score Machine turns a risky gamble into a calculated move designed to hit a specific funding goal.

Instead of crossing your fingers and hoping for the best, you can build a precise playbook for your credit journey. It’s all about making sure every dollar you invest in a tradelines for credit boost strategy goes directly toward fixing the problems holding you back. It's about working smarter to get the results you need.

Step 1: Analyze Your Full Credit Report

First things first: you need a crystal-clear picture of where you stand right now. Inside the Score Machine platform, you’ll start by pulling your full, tri-bureau credit report. This isn't just a simple score summary—it's the raw data, the same information lenders see when they make their decisions.

This step is non-negotiable. You can't fix a problem you don't fully understand. Pulling the report directly within the platform gives the AI the raw material it needs to find actionable insights, not just spit out generic advice.

Step 2: Diagnose the Weaknesses with AI

With your report loaded, Score Machine's AI gets to work. Think of it as a financial detective, combing through your file to find the exact factors dragging down your score. It won't just tell you that you have "high utilization"; it will pinpoint the specific accounts that are causing the most damage.

Is your credit history too short? Do you have too few account types? The AI analysis flags these weaknesses and shows you how much they're hurting your score, giving you a clear priority list. This is what separates a targeted, effective strategy from just taking a shot in the dark.

This screenshot shows how Score Machine translates your complex credit file into something you can actually understand and act on.

The visual breakdown immediately points out the problem areas, making it obvious what needs your attention first.

Step 3: See Your File Through a Lender's Eyes

Here's where things get really interesting. One of the most powerful features is the underwriting blueprint. This tool simulates how a lender’s automated system actually views your file, turning all that complicated credit data into a straightforward fundability report. It shows you the strengths, the weaknesses, and the red flags an underwriter would spot in a heartbeat.

This perspective is invaluable. It helps you understand not just your score, but your overall risk profile. Seeing your file from a lender's point of view is the key to making strategic decisions that directly improve your chances of approval.

Step 4: Select the Perfect Tradeline

Now that you have this deep analysis, you can choose a tradeline with surgical precision. The platform's insights guide you straight to the type of account that will fix your specific issues.

- High Utilization? The system will show you why you need a tradeline with a high credit limit—think $25,000+—to drastically bring down your overall debt-to-credit ratio.

- Short Credit History? Your analysis will point toward a seasoned tradeline, one with a history of 10+ years, to give the average age of your accounts a serious boost.

- Thin File? The blueprint might suggest adding a strong revolving account to build a more robust and trustworthy credit profile that lenders want to see.

This data-driven approach takes all the guesswork out of the equation. You’re no longer just buying a tradeline; you’re investing in a specific solution perfectly matched to your credit report's needs, ensuring you get the biggest possible impact for your money.

Building Long-Term Credit Health Beyond Tradelines

Getting a powerful tradeline can feel like you’ve crossed the finish line, but it’s really just the start of a much bigger race. While a strategic tradeline for credit boost can unlock funding opportunities that were previously out of reach, it's not a set-it-and-forget-it solution.

Think of it as a launchpad. It provides the initial thrust, but you're the one who has to pilot the rocket. True, lasting financial strength comes from what you do after you get that initial boost.

The tradeline gets you in the door; good financial habits are what let you stay there. Your new, higher score is an incredible asset, but it’s one you need to protect and grow. Without a solid game plan, you risk sliding right back to where you started. This is where you pivot from a short-term tactic to a long-term credit-building strategy.

From Boost to Sustainable Growth

Once your score jumps, your number one priority should be establishing your own primary tradelines. That higher score makes you a far more appealing candidate in the eyes of lenders, so now is the perfect time to apply for the credit products that will become the bedrock of your financial future.

Here’s a roadmap for what to do next:

- Open a Secured Credit Card: This is often the best first move. You put down a small cash deposit that acts as your credit limit, which makes getting approved much easier. Use it for a few small, regular purchases and—this is key—pay the balance in full every single month to build a perfect payment history under your own name.

- Get a Credit-Builder Loan: These are clever tools that essentially work in reverse. You make small monthly payments that go into a locked savings account. Once you've paid off the "loan," the money is yours. Every payment you make gets reported to the credit bureaus, adding a positive installment loan history to your file.

- Report Your Rent and Utilities: You're already paying these bills, so why not get credit for them? Several services can now report your on-time rent and utility payments to the credit bureaus, adding more positive accounts to your report without taking on new debt.

The Cornerstone of Lasting Credit Health

In the end, every single credit-building strategy comes back to one fundamental principle: perfect, on-time payments. This isn’t just important; it's the single most heavily weighted factor in your credit score, making up a massive 35% of the FICO model.

A tradeline gives you a fantastic head start, but it's the consistent, flawless payment record on your own accounts that will keep your score high for good.

The real goal isn't just a higher number; it's fundability. A tradeline gives you a temporary boost, but building your own strong credit history with responsible habits is what creates a permanently resilient financial future.

Use the window of opportunity a tradeline opens to get these foundational accounts in place. When you pair that immediate lift with these sustainable, long-term habits, you successfully transition from borrowing someone else's credit history to building your own.

Tradeline FAQs: Your Questions Answered

Diving into the world of tradelines can feel like navigating a maze. You've probably got a lot of questions, and getting straight answers is the only way to feel confident before you put your money on the line.

Let's cut through the noise and tackle the most common questions people have about using tradelines for a credit boost.

Are Tradelines Legal? And Are They Safe?

Let’s get the big one out of the way first. Yes, the practice of adding an authorized user to a credit card is 100% legal. It’s protected under the Equal Credit Opportunity Act.

But legality and safety are two different things. Your safety hinges entirely on the company you work with. A reputable provider will give you a rock-solid contract, be completely transparent about their process, and guarantee the accounts are spotless. The real danger isn't the method itself; it's falling for a shady operator. That's why you can't afford to skip the vetting process.

How Fast Will My Credit Score Go Up?

Generally, you should see an impact on your credit score within 30 to 60 days. The timeline starts when the credit card's monthly statement closes, which is when the new authorized user account gets reported to the credit bureaus.

The exact timing can vary a bit based on each creditor's reporting schedule. This is why it’s a good idea to keep an eye on your score in the months following the purchase. You'll be able to confirm the tradeline has posted and see its effect with your own eyes.

Is There Any Way a Tradeline Could Hurt My Score?

Absolutely, and this is the single biggest risk. If the primary cardholder misses a payment or maxes out the card, that negative activity can spill over onto your credit report and drag your score down.

This is where a legitimate tradeline company earns its keep. They completely remove this risk by guaranteeing their accounts will always have a low balance and a perfect payment history. They monitor these accounts like a hawk to make sure nothing negative ever gets reported, protecting both your investment and your credit.

How Long Does a Tradeline Stick Around on My Report?

An authorized user tradeline stays on your credit report for as long as you're listed as an authorized user. Most tradelines you buy will last for two to four billing cycles, giving you a specific window to make your move.

The real goal here isn't just a temporary bump. You need to use that score boost to secure your own primary lines of credit. Getting approved for your own credit cards and loans—and managing them well—is how you build a strong, sustainable credit history that keeps your score high long after the tradeline is gone.

Ready to stop guessing and start building a powerful credit profile? Score Machine uses AI-driven analysis to give you a clear, actionable plan. See your credit file through a lender's eyes and identify the exact steps you need to take to unlock better funding opportunities. Create your free account and get your personalized underwriting blueprint today.