Ever been turned down for a loan, a job, or even an apartment? That formal notice you receive explaining why isn't just a standard rejection letter. It's called an adverse action letter, and it's a crucial document required by law.

Think of it less as a rejection slip and more as a roadmap. This letter must outline the specific reasons for the denial, giving you the information you need to understand the decision.

What Is An Adverse Action Letter And Why Does It Matter?

At its core, an adverse action letter is a transparency tool mandated by federal law. The main goal is to protect consumers by making sure they know exactly why a negative decision was made about them. This knowledge is power—it allows you to spot and fix errors on your credit report or work on the financial issues that led to the denial in the first place.

For funding companies, this letter is much more than a box to check off a compliance list. Yes, staying on the right side of laws like the Fair Credit Reporting Act (FCRA) is non-negotiable. But savvy companies see the strategic potential. A well-written, helpful notice can turn a negative experience into a positive touchpoint, building trust and keeping the door open for future business.

From Legal Hurdle to Growth Strategy

Getting the adverse action process right can actually help a funding company grow its business. It’s a bit counterintuitive, but it works. When a denial comes with a vague, unhelpful notice, the applicant just feels frustrated and will likely never come back. That's a lost opportunity.

Now, imagine a different approach. Using a system like Score Machine to generate clear, data-driven adverse action letters completely changes the conversation. Instead of a flat "no," the applicant gets a detailed explanation of why they were denied and—here's the key part—the exact steps they can take to qualify in the future. This directly contributes to increasing a funding company's total funding volume by converting previously denied applicants into future approvals.

This transforms the entire interaction, building a pipeline of future clients.

A denial becomes a "not yet." By providing actionable guidance, funding companies can keep applicants engaged, creating a pool of informed, motivated people who will return as soon as they meet the criteria.

This strategy turns a regulatory requirement into a powerful engine for growth. It allows companies to increase their total funding volume over time by helping previously denied applicants get back on track and eventually get approved.

The benefits are clear:

- Builds a Future Pipeline: You keep potential clients in your orbit by giving them a clear path to approval, making it likely they'll come back to you when they're ready.

- Strengthens Brand Trust: A transparent and helpful process shows you’re a partner in their financial journey, not just a gatekeeper.

- Increases Funding Volume: Instead of losing applicants to competitors, you give them the tools to succeed, securing their business down the road and boosting your overall funding numbers.

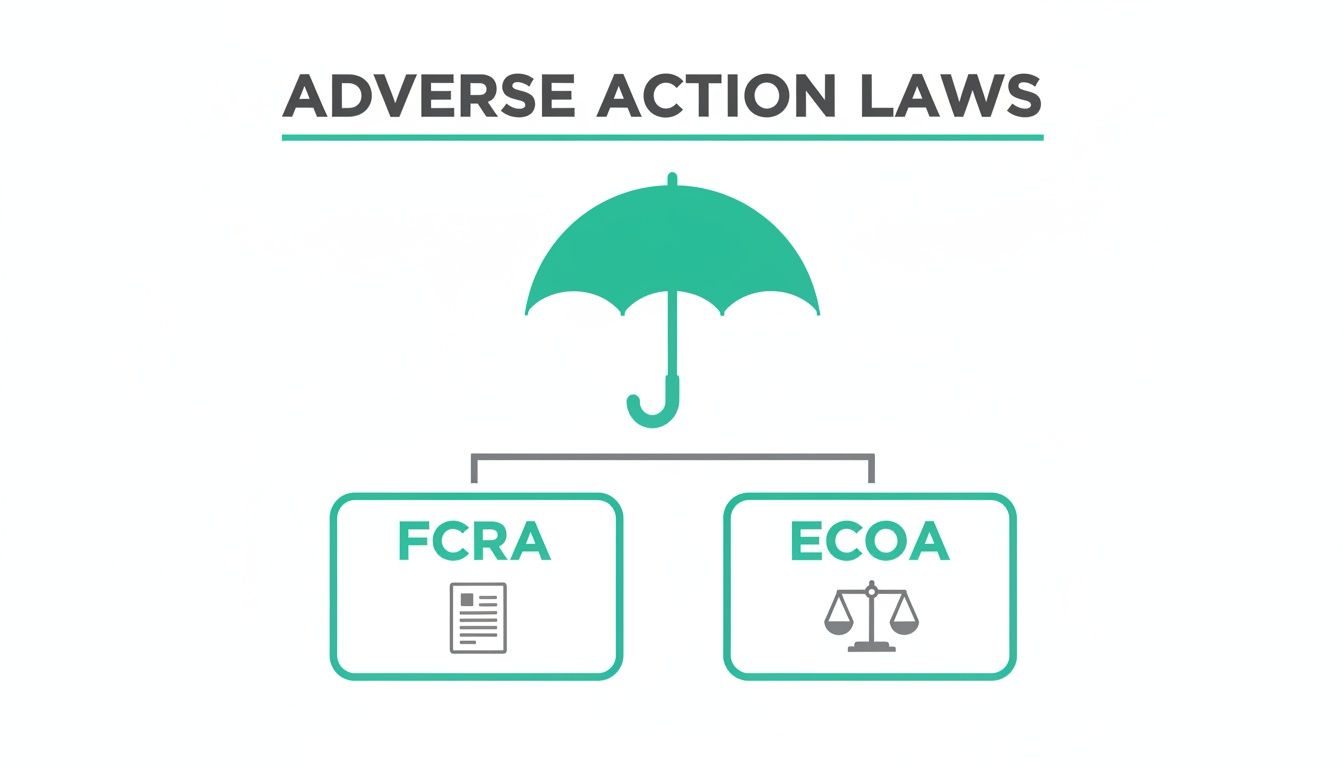

Navigating The Legal Maze of FCRA and ECOA Compliance

Any time a funding company uses a credit report to make a decision, it steps into a regulatory world shaped by two critical federal laws: the Fair Credit Reporting Act (FCRA) and the Equal Credit Opportunity Act (ECOA). They might seem similar, but they have very different jobs.

Think of it this way: FCRA is the "what and why" law, focusing on the data in the credit report. ECOA is the "who and how" law, ensuring the decision-making process is fair and non-discriminatory for everyone.

FCRA’s main goal is to make sure the information pulled from credit bureaus is accurate and used fairly. If you turn down an application—even partially—because of something in a credit report, FCRA is the reason you have to send an adverse action letter. It’s all about transparency.

ECOA, on the other hand, is designed to stop lending discrimination dead in its tracks. It makes it illegal to deny credit based on race, religion, national origin, sex, marital status, age, or because someone receives public assistance. ECOA is why you have to let applicants know your decision, whether it's a yes or a no, within 30 days.

Core Requirements of The FCRA

When a credit report is part of your decision, the FCRA gets very specific about what your adverse action notice needs to say. Missing any of these details can land you in serious hot water. The law isn't just about sending a rejection letter; it’s about giving the applicant the power to understand and fix potential errors.

Your notice absolutely must include:

- A clear statement that your decision was based on information from a credit reporting agency.

- The name, address, and phone number of the specific credit reporting agency that provided the report.

- A disclaimer stating that the credit reporting agency did not make the decision and can't explain why you did.

- A notice that the applicant has the right to get a free copy of their credit report from that agency within 60 days.

- A statement explaining their right to dispute any inaccurate or incomplete information with the credit agency.

These aren't just suggestions. They're required because they give the applicant a direct path to see the. same information you saw and correct any mistakes that might have cost them the approval. To dig deeper into these rules, you can find detailed compliance guides in our documentation at https://thescoremachine.com/docs.

Understanding ECOA And Its Broad Reach

While FCRA is triggered specifically by the use of credit reports, ECOA’s rules apply to all credit applications, no matter what information you used. If you deny someone credit, ECOA requires you to send a notification, reinforcing the law's anti-discrimination mission with clear, consistent communication.

An ECOA notice has to either give the specific reasons for the denial or tell the applicant they have a right to request those reasons within 60 days. This forces creditors to have a legitimate, non-discriminatory basis for their decisions.

The term "adverse action" is also wider than you might think. Under the FCRA in the US, it isn't just a flat-out denial. It also includes offering someone less favorable terms than they applied for or even downgrading an existing account. For example, if an applicant doesn't qualify for your best rates and you offer them a higher-interest product instead, they're still entitled to a notice.

This principle of transparency isn't unique to the US. In Europe, GDPR has similar consumer protections, and sending a vague notice can lead to massive fines. Understanding both FCRA and ECOA is the foundation for building a compliant, transparent, and trustworthy funding business.

Anatomy Of A Compliant Adverse Action Letter

So, we've covered the legal theory. Now let's get practical. What does a compliant adverse action letter actually look like? Think of it less like a single document and more like a carefully constructed information packet. Every single piece is there for a reason—to protect both your business and the applicant you've just turned down.

Simply sending a letter that says "Application Denied" is a fast track to a compliance nightmare. Today's regulations, particularly the FCRA and ECOA, demand total transparency. The real goal is to give the consumer a clear road map, showing them exactly what information was used and how they can verify it for themselves.

This is where two major federal laws come into play, forming the legal framework for every notice you send.

As you can see, both the Fair Credit Reporting Act (FCRA) and the Equal Credit Opportunity Act (ECOA) govern the process. They work together, creating a dual layer of rules you absolutely have to follow.

The Non-Negotiable Core Components

When your decision is based on information from a consumer report, every adverse action letter you send must include a few key things. These aren't just suggestions; they are strict legal requirements. Getting even one wrong can lead to some pretty hefty fines.

Here’s a breakdown of what you must include:

- Specific Reasons for the Decision: This is the heart of the letter. You have to state the main reason or reasons for the denial, and you have to be specific. Vague phrases like "poor credit history" won't cut it anymore. Instead, you need to point to the real factors, like “high utilization of existing credit” or “delinquent past or present credit obligations with others.”

- Credit Reporting Agency Information: You have to name the credit bureau that provided the report. That means including the full name, address, and phone number of the agency, whether it’s Equifax, Experian, TransUnion, or another provider.

- A Statement on the Agency's Role: The letter needs a clear disclaimer stating that the credit bureau did not make the decision and can't explain why it was made. This points the applicant back to the right party—you.

These three elements are the foundation of a compliant notice. They make sure the applicant knows who to call and why you made the decision you did.

Informing Applicants of Their Rights

Beyond just the "what" and "why," your letter also has to educate the applicant on their rights under the law. This commitment to transparency is a cornerstone of the FCRA.

An adverse action letter must act as a clear guide, informing the consumer of their power to investigate and dispute the data that led to the denial. It shifts the focus from a simple rejection to an opportunity for correction and financial education.

Your notice is legally required to tell the applicant two very important things:

- Their right to a free credit report: You must inform them that they can get a free copy of their consumer report from the agency you named, as long as they request it within 60 days.

- Their right to dispute inaccuracies: The letter has to explain that they can dispute any information they believe is inaccurate or incomplete directly with that credit reporting agency.

This is where the process actually empowers the consumer. It gives them a direct path to find and fix errors—like mixed-up files or old, outdated information—that could be torpedoing their financial life.

Putting all these pieces together correctly is non-negotiable. Modern systems can automate this, ensuring every disclosure is included correctly, every single time. If you want to see how this can be built into an efficient workflow, you can learn more about the features that enable automated compliance.

Adverse Action Letter Compliance Checklist

To make sure nothing slips through the cracks, it’s helpful to use a checklist. This table breaks down the essential components required by both the FCRA and ECOA in every adverse action notice.

| Component | Description | Required By |

|---|---|---|

| Action Taken | A clear statement of the specific adverse action taken (e.g., credit denied, account terminated). | ECOA |

| Creditor Information | The name and address of the creditor or business making the adverse decision. | ECOA |

| Specific Reasons | The principal and specific reason(s) for the denial, not vague or generic codes. | FCRA & ECOA |

| CRA Information | The name, address, and toll-free telephone number of the consumer reporting agency (CRA) used. | FCRA |

| CRA Disclaimer | A statement that the CRA did not make the decision and cannot provide the reasons. | FCRA |

| Right to Free Report | A notice of the consumer's right to obtain a free copy of their report from the CRA within 60 days. | FCRA |

| Right to Dispute | A notice of the consumer's right to dispute inaccurate or incomplete information with the CRA. | FCRA |

| Credit Score Details | If a credit score was used, you must disclose the score, the range of possible scores, key factors that adversely affected it, and the date it was created. | FCRA (FACTA) |

| ECOA Notice | The required ECOA notice that prohibits discrimination against credit applicants. | ECOA |

Following this checklist ensures you’re not just sending a letter, but a compliant, transparent, and fair communication that meets all federal standards. By assembling these components correctly, you create an adverse action letter that upholds consumer rights and shields your business from unnecessary legal risk.

Common Compliance Mistakes and How to Avoid Them

Navigating the rules for an adverse action letter can feel like walking a tightrope. Even with the best of intentions, it’s surprisingly easy to stumble into common compliance traps that lead to hefty fines and a tarnished reputation. These mistakes often seem small, but to regulators, they signal a failure to protect a consumer's rights.

One of the most frequent fumbles is sending a notice with vague, cookie-cutter reasons for denial. Simply checking a box next to "poor credit history" or "credit score too low" just doesn't cut it anymore. That kind of generic feedback leaves the applicant completely in the dark and goes against the very spirit—and letter—of the law, which demands real transparency.

Timing is another place where businesses often slip up. The Equal Credit Opportunity Act (ECOA) is crystal clear: you generally have 30 days from receiving a completed application to notify the applicant of your decision. Missing that deadline is a straightforward violation and an easy thing for regulators to catch.

Vague Reasons and Incomplete Information

Put yourself in the shoes of a small business owner who applied for a loan to expand their shop. They get a denial letter that just says "unfavorable credit report." What does that even mean? Was it a late payment from two years ago? High credit card balances? Maybe there’s a flat-out error on their report? Without any specific details, they have no idea what to do next.

This is exactly the kind of situation regulators are cracking down on. The game really changed when the Consumer Financial Protection Bureau (CFPB) issued Circular 2023-03, which completely upended the old requirements. For years, creditors got by using pre-printed forms with broad categories, but the new guidance demands highly specific, individualized reasons tied directly to the applicant's financial picture. That could mean pointing to exact late payments or a high debt-to-income ratio, not just a low score. You can read more about these enforcement trends and see how fines are shaping compliance standards.

Beyond vague reasons, other common missteps include:

- Forgetting the Credit Bureau Details: You absolutely have to include the full name, address, and phone number of the credit reporting agency you used.

- Omitting Required Disclosures: Leaving out the legally required statements about the applicant's right to a free credit report and their right to dispute inaccuracies is a major no-no.

- Providing Incorrect Information: Listing the wrong credit bureau or an old phone number is just as bad as leaving it out, since it makes it impossible for the applicant to follow up.

Shifting From Compliance Risk to Funding Opportunity

Getting this right isn't just about dodging fines; it’s about building a smarter business process that can actually help you fund more deals down the road. When you handle a denial poorly, that applicant is gone for good. But when you generate a compliant, detailed adverse action letter, it becomes a roadmap for them.

This is where a system like Score Machine can be a game-changer. By automating how these letters are created, you get rid of the human error that creeps in with manual processes. The platform makes sure every required disclosure is in place and that the reasons for denial are specific and backed by data pulled straight from the applicant's file.

Instead of a compliance task that slows you down, the adverse action process becomes a tool for nurturing future clients. By providing a clear, actionable blueprint for what needs to be fixed, you empower applicants to improve their creditworthiness and ultimately increase your funding volume.

This simple shift in perspective turns a hard "no" into a "not yet." The applicant you turned down now understands exactly what they need to work on. Once they get their finances in order, who do you think they'll come back to? The company that treated them with transparency and respect. This approach builds a loyal pipeline of future business, directly contributing to your bottom line over time.

How Automation Actually Increases Your Funding Volume

Let’s be honest, compliance often feels like playing defense—just a set of rules you have to follow to stay out of trouble. But what if you could flip that script and turn compliance into your best offensive play for growth? Manually handling adverse action letters isn't just a drag on your team's time; it's a major bottleneck that’s actively choking your funding pipeline.

This is where automation stops being a buzzword and becomes a real competitive edge. A platform like Score Machine takes the entire adverse action process from a reactive legal chore and turns it into a proactive engine for funding more deals. It’s not just about sending a rejection letter; it’s about automatically generating compliant, specific, and genuinely helpful notices that boost your total funding volume over time.

This isn't just theory. The system is built to guide applicants toward becoming fundable, turning a denial into a future deal.

The key is moving beyond a simple "no" to giving someone a clear, actionable path forward. That’s how you convert more applicants down the road.

Eliminating Risk and Creating Capacity

First things first: automation gets rid of human error. Every single adverse action letter your team creates manually is a potential landmine. A missed disclosure, a vague reason for denial—one little slip-up can lead to some seriously costly fines and legal headaches.

Score Machine’s AI-driven system generates fully compliant notices in an instant, all based on your specific underwriting criteria. This guarantees that every letter has the right legal language, the correct credit bureau information, and the specific denial reasons required by the FCRA and ECOA. No guesswork involved.

By automating compliance, you’re not just avoiding risk—you’re freeing up your people. Instead of spending hours buried in paperwork, they can focus on what they were hired to do: build relationships and close deals. That shift alone can dramatically increase your team’s capacity to handle more applications.

This is about more than just being efficient. It's about reclaiming valuable time and reinvesting it into activities that actually make you money. The system handles the compliance grunt work so your team can focus on funding.

Turning a 'No' Into a 'Not Yet'

Now for the real game-changer. The biggest impact automation has on your funding volume is how it completely transforms your relationship with denied applicants. A generic, boilerplate denial letter is a dead end. The applicant feels rejected, has no idea what to do next, and you can bet they won't be coming back.

Automation flips this entire dynamic on its head. Instead of a hard "no," you give them a supportive "not yet" by providing a clear, data-driven blueprint for how to get approved. The automated adverse action letter from Score Machine doesn't just list problems; it delivers concrete, actionable advice.

For instance, rather than a vague "high credit utilization," the system can specify which accounts need to be paid down and by how much to meet your underwriting standards. This empowers the applicant with a real plan. You can see a breakdown of Score Machine's process for delivering actionable insights to get a feel for it.

This approach creates a pipeline of future clients by:

- Keeping Applicants Engaged: When you give someone a clear roadmap, they're far more likely to stick with you instead of running to a competitor.

- Building Genuine Goodwill: You're no longer just a gatekeeper; you're a partner invested in their success.

- Creating a Predictable Future Pipeline: Denied applicants become a pool of warm leads who are actively working to meet your specific funding criteria.

The Compounding Effect on Your Bottom Line

This strategy has a direct and measurable impact on the number of deals you close. Think about it: what if just 20% of your denied applicants got a detailed, automated action plan and actually followed it? Within 6 to 12 months, that 20% comes back as qualified, fundable clients.

Over time, this effect snowballs. The pipeline of returning, now-qualified applicants grows, steadily increasing the total number of deals you fund each quarter. And the best part? You didn't have to spend a single extra dollar on marketing to acquire them. You're creating your own source of high-quality leads from a group you used to write off as a loss.

This is how you get a real leg up on the competition. While others treat denials as a dead end, you’re using an automated adverse action letter system to cultivate a loyal, growing base of future customers. Automation doesn't just make compliance easier—it makes your entire funding operation more profitable.

Turning Denials Into a Proactive Growth Strategy

What if a denial wasn't the end of the road for an applicant, but the start of a new conversation? For most funding companies, sending an adverse action letter is just a final, legally required step. It’s a reactive measure that essentially closes the door on someone who came to you for help. But this standard approach leaves a huge amount of future business on the table.

There’s a much smarter way to handle these situations: shift from reactive compliance to proactive client development. Imagine analyzing a potential applicant’s complete financial picture before you have to make a formal decision. This simple change turns a routine application into a real opportunity to partner with someone and guide them on their journey to becoming fundable.

From Gatekeeper to Funding Partner

The traditional model forces you into the role of a gatekeeper. An applicant comes to you, you run their numbers, and you deliver a simple "yes" or "no." This dynamic can feel adversarial, and a denial often feels like a permanent rejection. The applicant walks away disappointed and probably never thinks of your company again.

But what if you could change that entire interaction? By using a system like Score Machine before making that final call, you can flip the script. Running a borderline applicant's profile through the platform gives you a detailed, underwriting-style blueprint. It pinpoints the exact red flags that would normally lead to a denial, but it does so before one ever becomes official.

This insight completely changes the conversation you can have. Instead of a hard "no," you can offer a clear, data-driven path forward.

This approach redefines your role. You're no longer just a source of capital. You become a trusted advisor who can show an applicant the exact steps they need to take to get approved. That builds incredible loyalty and ensures that when they finally qualify, you’ll be their first call.

Suddenly, your denials aren't dead ends. They become a self-filling pipeline of future clients, boosting your funding volume without you having to spend a single extra dollar on marketing.

Coaching Applicants to Get Qualified

Once you have this pre-denial blueprint from the analysis, you can start proactively coaching those borderline applicants. The system gives you precise, actionable steps they can take to improve their credit profile and meet your specific underwriting guidelines.

This isn't generic advice. The coaching can get very specific, including guidance on:

- Targeted Debt Reduction: Showing them exactly which credit card balances to pay down to improve their debt-to-income ratio or credit utilization.

- Credit History Optimization: Pointing out older, positive accounts that they should be sure to keep open to preserve the length of their credit history.

- Error Correction: Flagging potential mistakes on their credit report that they can dispute with the bureaus.

By offering this kind of clear, helpful guidance, you dramatically reduce application fallout. Applicants who would have been automatically denied are instead nurtured into qualified candidates. This shortens the funding cycle because when they come back to you, they're ready for an approval. You lock yourself in not just as a one-time lender, but as their long-term partner for any future capital needs.

Got Questions About Adverse Action Letters? We've Got Answers.

When you're dealing with something as important as an adverse action letter, it’s natural for questions to pop up. Let's tackle some of the most common ones that funding companies and applicants run into.

How Long Do I Have to Send an Adverse Action Letter?

This is all about timing. According to the Equal Credit Opportunity Act (ECOA), you have 30 days to inform an applicant of your decision after you’ve received their completed application for credit.

Getting that letter out promptly isn't just good customer service—it’s a legal must-have. No one likes being left in the dark, and the law makes sure they aren't.

What’s the Difference Between an FCRA and ECOA Notice?

Think of it this way: they're two different sets of rules that often overlap. An FCRA notice is triggered when your decision is based on information from a consumer credit report. The ECOA notice is broader; it's required for any credit application denial, no matter the reason, to fight against discrimination.

Here’s a simple way to keep them straight: FCRA is about the data (from a credit report), while ECOA is about the decision (on a credit application). A well-drafted adverse action letter will cover the bases for both laws.

Can an Adverse Action Be Based on Something Other Than a Credit Score?

Absolutely. A low credit score is a frequent culprit, but it's far from the only reason. Adverse actions can stem from all sorts of legitimate factors related to an application for employment, insurance, or even housing.

The golden rule is this: whatever the reason, your adverse action letter must state it clearly and specifically.

Do I Need to Send a Letter for an Incomplete Application?

Generally, no. If an application isn't complete, you usually don't have a legal obligation to send a formal adverse action letter.

That said, having a clear, documented process for handling incomplete applications is a smart move. Consistent communication and good record-keeping can head off a lot of confusion and potential compliance headaches later on.

Ready to transform compliance from a headache into a growth engine? Score Machine uses AI to generate fully compliant, data-driven adverse action letters that turn denials into a pipeline of future clients. Explore how Score Machine can increase your funding volume.