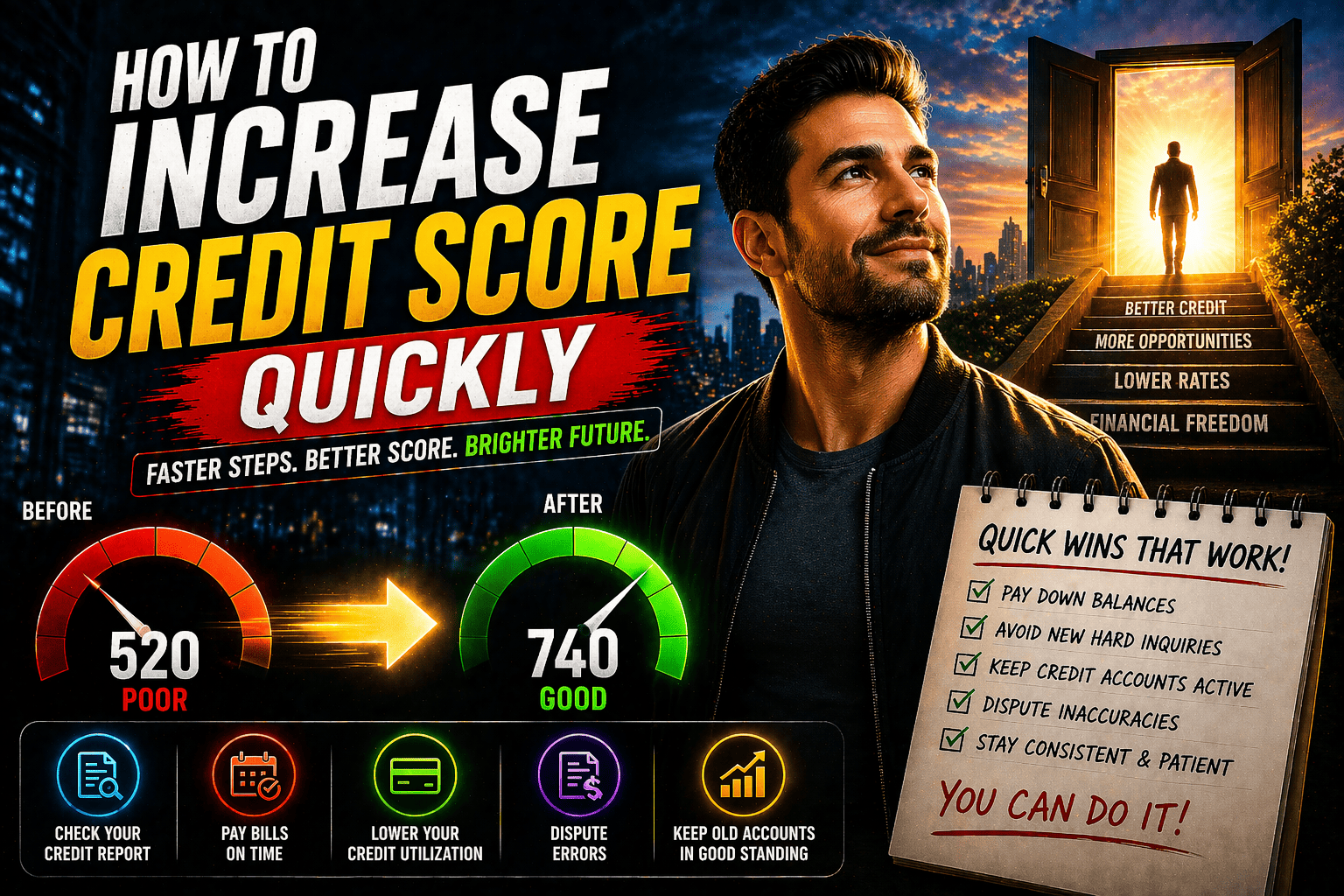

How to Increase Credit Score Quickly: Your Guide to a Better Score

When you're staring down a low credit score, especially when you need financing, it can feel like you’ve hit a brick wall. But here's the thing I've learned from years of experience: you have far more control over that number than you might think. While those "fix your score overnight" promises are pure fantasy, making a real, measurable difference in 30 to 90 days is absolutely possible if you know where to focus your energy.

Your Blueprint for a Higher Credit Score

Forget the generic advice you’ve heard a thousand times. This guide is all about high-impact actions that get you the biggest bang for your buck, fast. We'll dig into the five factors that make up your score—payment history, credit utilization, credit age, credit mix, and new inquiries—but we're going to zero in on the ones you can actually change right now. This is your roadmap for turning financial guesswork into a clear, actionable plan. A better score isn't just a number; it's the key that unlocks lower interest rates and better opportunities.

This isn’t just talk. We saw real-world proof of how quickly focused efforts can work during the pandemic. From late 2019 to early 2022, the percentage of Americans with good credit scores jumped by nearly 5 points. Even with all the economic uncertainty, people who concentrated on paying down debt and keeping their accounts current saw their profiles improve significantly. It’s a powerful reminder that the right moves can rebuild your financial standing much faster than you’d expect. You can even check out the detailed analysis from the St. Louis Fed to see the data for yourself.

How Score Machine Increases Funding for Lenders

For funding companies, leveraging a credit intelligence platform like Score Machine is a direct strategy to increase funded loan volume. The platform transforms the lending process from a simple "approve/deny" transaction into a dynamic, opportunity-driven system. It identifies applicants who are just shy of qualifying—often the largest pool of denials—and provides an exact, data-driven roadmap to get them approved. By showing a client that paying down a specific credit card by $750 will boost their score by the 15 points needed for approval, a lender turns a denial into a closed deal. This proactive approach salvages otherwise lost revenue, expands the customer base, and builds lasting client relationships, directly contributing to a measurable increase in overall funding.

This strategic approach does more than just build goodwill; it directly impacts the bottom line by increasing the number of funded loans. By understanding how Score Machine works, funding companies can spot these opportunities, deliver real value to applicants, and ultimately, close more deals. It creates a true win-win, turning what would have been rejections into profitable, lasting partnerships.

Mastering the Two Levers That Control Your Score

If you want to raise your credit score quickly, you need to cut through the noise. Forget all the little tips and tricks for a moment and focus on just two things. An incredible 65% of your FICO score comes down to your payment history (35%) and how much of your available credit you're using (30%). These are the big levers. Pull them correctly, and you’ll see fast, significant results.

This isn’t just theory—it’s a massive strategic advantage, especially for funding companies. When you have an applicant who's right on the edge of qualifying, understanding these core factors is everything. Instead of a vague "your score is too low," a lender using a tool like Score Machine can pinpoint the exact problem.

Suddenly, the conversation changes. Imagine seeing that a client has a perfect payment history but their credit utilization is stuck at 45%. You can give them precise guidance: "Pay down your Visa card by $800, and your score should jump enough to get you approved." This turns a near-miss into a funded deal and directly boosts revenue. It’s all about focusing on what truly moves the needle.

Solidify Your Payment History

Your payment history is the single biggest piece of the credit score pie, making up a full 35% of the total. It’s simple, really: it’s a record of whether you've paid your bills on time. Just one late payment reported to the bureaus can tank your score and hang around on your report for up to seven long years.

But what if a late payment has already happened? Don't panic. You have options.

- Bring Accounts Current: This is priority number one. If you have any past-due accounts, get them paid immediately. The damage from a late payment gets worse as it ages from 30 to 60 to 90 days late.

- Write a Goodwill Letter: If you have an otherwise solid track record with a creditor but slipped up once, a "goodwill letter" can work wonders. You simply write to them, politely explain what happened, and ask for a "goodwill adjustment" to remove the negative mark.

- Set Up Autopay: The best defense is a good offense. Set up automatic payments for at least the minimum due on all your accounts. This simple step eliminates the risk of human error and protects this huge chunk of your score.

Master Your Credit Utilization Ratio

Right behind payment history in importance is your credit utilization, which accounts for 30% of your score. This ratio is just a fancy way of saying how much of your available revolving credit—think credit cards—you’re actually using. From a lender's perspective, high utilization is a major red flag that you might be financially overextended.

Calculating it is easy: divide your total credit card balances by your total credit limits. For instance, if you owe $2,000 on a card with a $5,000 limit, your utilization on that card is 40%.

The common advice is to keep your overall credit utilization below 30%. But if you want the fastest possible score boost, aim for under 10%. That's the gold standard. A super-low ratio sends a powerful signal to lenders that you manage your credit responsibly.

This is another area where funding companies can get a serious edge. Instead of guessing, they can use Score Machine to simulate what happens when debt is paid down. They might see that helping an applicant pay a specific card down from 80% utilization to 25% could trigger a 40-point score increase. That kind of data-driven insight creates a clear, predictable path to getting the client funded.

Here’s how you can drop your utilization fast:

| Tactic | How It Works | Speed of Impact |

|---|---|---|

| Pay Down Balances | The most direct route. Every dollar you pay down on your balance immediately lowers your utilization ratio. | High (within 30-45 days) |

| Request a Limit Increase | Call your card issuer and ask for a higher credit limit. If they say yes, your available credit expands, which instantly drops your ratio. | High (can be immediate) |

| Pay Before Statement Closing | Most card issuers report your balance to the bureaus on your statement closing date. By making a payment before that date, a lower balance gets reported. | High (next reporting cycle) |

Find and Fix Hidden Credit Report Errors

You can't fix a problem you don't know you have, and your credit report could be hiding a big one. It’s a frustrating truth, but errors on credit reports are way more common than people think. These mistakes can unfairly drag down your score, killing your chances of getting approved for funding or locking you into a higher interest rate.

Think of it like trying to drive somewhere new with a GPS that has the wrong street names—you'll get lost, frustrated, and you definitely won't end up where you want to be. Your credit report is the map lenders use. If it's wrong, they get a completely skewed picture of who you are financially. Finding and fixing these inaccuracies is like correcting the map, and it's one of the most direct ways to boost your score fast.

The Most Common Report Errors to Look For

When you pull your reports from Experian, Equifax, and TransUnion for the first time, it's easy to feel overwhelmed by all the data. Don't try to read every single line. Instead, go in with a plan and hunt for the most common and damaging mistakes.

- Wrong Personal Details: Are your name, address, and Social Security number all correct? Even a simple misspelling can cause major mix-ups, like merging your file with someone else's.

- Accounts You Don't Recognize: This is a huge red flag. If you see a credit card or loan you never opened, it could be a sign of identity theft.

- Zombies on Your Report: Negative information, like a late payment, is only supposed to stick around for seven years. Check the dates on everything. If something is older than that, it shouldn't be there.

- Double Trouble: Sometimes a single debt, especially a medical bill, gets reported twice by mistake. This makes it look like you owe double what you actually do.

Sifting through years of data manually is a real grind. Thankfully, technology has made this part of the process much easier. A good AI credit file analysis can scan your entire report in seconds, automatically flagging potential errors for you. It saves a ton of time and points you directly to what needs to be disputed. You can check out the features of an AI credit analysis tool to see how it can make this process faster and more effective.

How to Formally Dispute an Error

Found a mistake? Great. Now it's time to take action. You need to file a formal dispute with the credit bureau that's reporting the error. All three bureaus—Equifax, Experian, and TransUnion—have online dispute portals, which are hands-down the quickest way to get the ball rolling.

The Fair Credit Reporting Act (FCRA) is on your side here. It legally requires the credit bureaus to investigate your claim, usually within 30 days. They'll reach out to the company that reported the information and ask for proof. If that company can't prove it's accurate, or if they just don't respond, the bureau must remove the item from your report.

It's hard to overstate the impact of this. Getting a single incorrect negative mark removed—like a collections account that never belonged to you—can be a total game-changer. We've seen scores jump 20, 50, or even more points from this one fix alone.

The Impact on Funding Companies

This isn't just a strategy for individuals; it's a massive opportunity for funding companies, too. Think about an applicant who is right on the edge of getting approved. A hidden error on their credit report could be the one thing pushing them into the "denied" pile.

By helping that client spot and dispute the mistake, a funding company can flip a denial into an approval. This creates a powerful win-win. The applicant gets the loan they desperately need, and the company closes a deal it was about to lose. It changes the dynamic completely—you're no longer just a lender, you're a partner helping your client succeed. That builds incredible loyalty and, just as importantly, increases your funded loan volume.

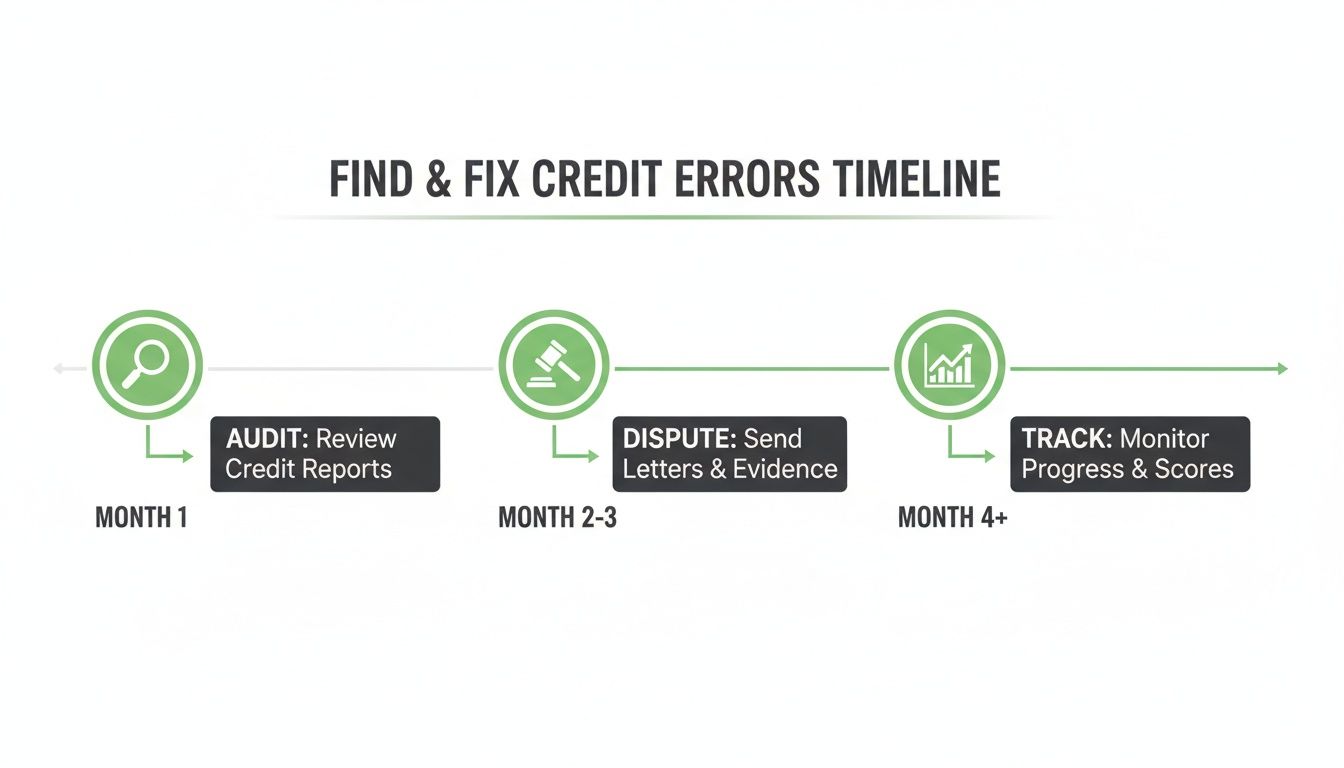

A 30-60-90 Day Plan for Measurable Progress

Knowing what to do is one thing, but actually putting it into practice is another challenge entirely. The best way I've found to turn knowledge into real, measurable progress is to use a structured, time-based plan. Instead of getting overwhelmed trying to do everything at once, we'll break down your credit-building journey into manageable 30-day sprints.

This phased approach creates a clear, motivating path. By zeroing in on specific goals for each stage, you'll start seeing tangible results that keep you pushing forward.

This timeline breaks down those critical first moves into a simple process: audit your report, dispute every error you find, and then track the results.

Following this sequence is non-negotiable. It ensures you're building your strategy on a solid foundation of accurate information, which is the only way to maximize the impact of your efforts.

Your First 30 Days: The Immediate Wins

Month one is all about triage. We’re going after the highest-impact items—the quick wins that can deliver the most significant score boosts in the shortest amount of time. Your entire mission is to scrub your report clean and slash your credit utilization ratio.

- Dispute Every Single Error: Go through the credit report you audited and file a dispute for every inaccuracy you found. A bogus collection account or an incorrect late payment can be a massive anchor on your score. Removing it is like taking your foot off the brake.

- Pay Down Balances Strategically: Don't just spread your money around. Concentrate your available funds on the credit card with the highest utilization. If one card is maxed out at 90% capacity, paying it down below 30% will have a much bigger impact than making small payments across several cards with lower balances.

- Pay Before the Statement Date: This is a pro tip many people miss. Make a payment on your credit cards a few days before your statement closing date. This forces a lower balance to be reported to the bureaus, which can give your utilization an immediate boost.

This 30-day blitz is designed to stop the bleeding and build positive momentum. By hammering away at errors and high utilization first, you're targeting the factors that carry the most weight and can change the fastest.

For funding companies, walking a "near-miss" applicant through this exact 30-day plan can be a game-changer. Using a platform like Score Machine, you can actually simulate the impact of these actions. You can show a client exactly how paying down a specific card by $500 could be the key to their loan approval, turning a potential rejection into a funded deal.

The Next 60 Days: Building Momentum

With a cleaner report and lower utilization, the next 30 days are all about building on that strong foundation. Now it's time to introduce strategies that add positive history and depth to your credit file. This is where you can leverage existing good credit to your advantage.

One of the most powerful moves at this stage is becoming an authorized user. If you have a trusted family member with a long-standing credit card that has a perfect payment history and a very low balance, ask them to add you.

This "credit piggybacking" technique lets their positive history—including the account's age and stellar utilization—appear on your credit report. It’s not uncommon to see a score jump of 20-50 points from this one move, often in just a few weeks.

The Final 90 Days: Optimizing and Maintaining

By day 90, you should be seeing some serious progress. The focus now shifts from aggressive repair to long-term health and optimization. This is about cementing the good habits you've built and fine-tuning your overall credit mix.

- Maintain Low Balances: Don't let your utilization creep back up. Continue to keep all your credit card balances below 10% for the best possible results.

- Optimize Your Credit Mix: Lenders love to see that you can responsibly manage different types of credit—both revolving accounts (like credit cards) and installment loans (like an auto or personal loan). If you only have credit cards, this might be a good time to consider a small, manageable installment loan, but only if it genuinely aligns with your financial goals.

- Track Your Progress: Keep a close eye on your score. A tool like Score Machine helps you monitor your progress and see how your actions are paying off. Consistent tracking helps you catch any new issues early and, just as importantly, keeps you motivated.

Achieving an elite score is more attainable than most people think. As of March 2025, while only 1.76% of U.S. consumers have a perfect 850 FICO score, a much larger 23% have scores of 800 or higher. The common threads among these high achievers? No late payments, credit utilization under 10%, and a long credit history—all things this 90-day plan helps you build. You can discover more insights about what top-scorers have in common.

How Lenders Use Credit Insights to Turn "No" into "Yes"

So far, we've talked about how you can raise your own credit score. But what if you're on the other side of the desk? For funding companies, credit repair pros, and financial coaches, understanding the full story behind a credit report is the secret to growing your business. It’s about more than just a simple yes or no; it's about finding a clear path to getting a deal done.

This is exactly where credit intelligence tools like Score Machine change the game. Instead of just seeing a single, flat number, you get an instant, underwriting-level analysis that shows you the why behind the score. Suddenly, those borderline applicants who were almost there can become funded clients.

From Near-Miss to Funded Deal

Picture this common scenario: a small business owner applies for a loan, but their score is just 20 points too low. In the old days, that was it. A denial letter goes out, and you both move on.

But what if you could dig a little deeper? A quick analysis might show that their payment history is spotless, but their credit utilization is sky-high—over 80% on a couple of business credit cards.

Instead of a hard "no," you can now offer a precise, actionable roadmap. You can confidently tell the applicant that paying down a specific $1,500 balance will very likely give them the score boost they need to get approved.

This small shift in approach has a massive impact on your business:

- You fund more deals. Plain and simple. You start salvaging applications that would have been lost, which goes straight to your bottom line.

- You build incredible loyalty. You've just turned a rejection into a collaborative, positive experience. That person isn't just a client; they're a client for life.

- You create a predictable pipeline. Nurturing these near-miss applicants gives you a reliable stream of future business you can count on.

This strategy transforms your role from a simple gatekeeper into a true financial partner. It’s a powerful way to stand out in a crowded market by offering real value that goes far beyond just the money.

A Smarter Way to Work for Credit Professionals

If you're a credit repair specialist or a financial coach, this kind of insight is a total game-changer. I know from experience that manually tearing apart a credit report to build an action plan for a client can take hours of painstaking work.

A platform like Score Machine automates all of that, spitting out professional, easy-to-digest reports in just a few seconds.

This efficiency means you can scale your services without ever cutting corners on the quality of your advice. The system identifies the exact moves a client needs to make, complete with a timeline and simulated results.

Imagine being able to tell a client, "If we get this incorrect collection removed and you pay down your Visa by $700, we project your score will jump 45 points within 60 days." That kind of specific, confident advice is how you build trust and get the referrals that grow your business.

A Real-World Example: How One Funder Boosted Volume by 15%

Let me give you a concrete example. A mid-sized business lender was getting frustrated by the number of applicants who were just on the edge of qualifying. They were turning away a lot of good people.

They started using Score Machine during their pre-qualification process to analyze these borderline files.

Instead of issuing an immediate denial, their loan officers used the platform's analysis to find the root cause—usually high card balances or a few small, fixable errors. They then gave these applicants a simple, step-by-step plan generated right from the system.

The result? Within six months, the company saw its funded loan volume climb by 15%. That entire increase came from the pool of applicants they would have previously rejected. By showing people the exact path to becoming fundable, they created a win-win that turned missed opportunities into profitable, long-term relationships.

Getting your credit score up is a huge win, but the real challenge—and the real prize—is keeping it there. Your score isn't a static number; it's a living, breathing reflection of your financial habits. Think of it less like a one-time repair project and more like a long-term wellness plan.

From One-Time Fix to Ongoing Partnership

This is a game-changer for funding companies. Instead of treating a client interaction as a single transaction, tools like Score Machine let you build an ongoing relationship. By keeping an eye on a client's credit journey, you can spot new opportunities as they arise.

Imagine this scenario: a client who didn't quite qualify for a loan takes your advice and starts improving their credit. With consistent monitoring, you get an alert the moment their score crosses the threshold for a better product or more favorable terms. You can immediately reach out with a pre-approved offer, locking in a deal that a competitor might have otherwise snagged.

This isn't just about good service; it's about building a robust pipeline of repeat business. It turns a simple analysis tool into an engine for client retention and revenue.

The Power of Paying Attention

For individuals, the payoff for tracking your progress is just as massive. It’s motivating to see the direct results of your hard work, and it allows you to catch small issues before they snowball into big problems. Plus, it's one of your best defenses against fraud.

Don't just take my word for it. A massive global study from TransUnion found that consumers who actively check their credit see their scores improve much more than those who don't. You can read the full study to understand the impact of credit monitoring.

The effort you put into learning how to increase credit score quickly pays off again and again, but only if you keep tracking it. For more ideas on building lasting financial health, check out The Score Machine blog.

Your Top Credit Score Questions, Answered

Once you start working on your credit, a lot of questions pop up. It's totally normal. Here are some straightforward answers to the questions I hear most often, designed to cut through the noise and give you clarity.

How Can Score Machine Increase a Funding Company's Volume?

Funding companies often have to deny applicants who are just a few points shy of qualifying. Using a tool like Score Machine allows them to analyze these "near-miss" files and provide a precise, actionable plan to the applicant. Instead of a denial, the lender can say, "If you pay down this one credit card by $500, your score will likely increase enough for approval." This strategy converts potential rejections into funded deals. By salvaging these applications, the company directly increases its funded loan volume, turns a negative experience into a positive one for the client, and builds a pipeline of future business, all of which contributes to significant revenue growth.

How Long Until I Actually See My Score Change?

You can often see the needle move pretty fast. Most creditors report to the bureaus every 30 to 45 days, so actions like paying down a credit card balance will usually show up in the next cycle.

Correcting an error through a dispute might take a little longer, typically in the 30 to 60-day range, for the bureaus to investigate and update your file. The key is that positive actions get reflected relatively quickly.

Should I Close My Old Credit Cards?

My advice is almost always a hard no. It feels like you're cleaning house, but closing old accounts can backfire.

Here’s why:

- It lowers your total available credit, which can instantly spike your credit utilization ratio—a huge factor in your score.

- It can shorten the average age of your credit history, another key piece of the scoring puzzle.

Unless an old card has a ridiculously high annual fee, it's far better to keep it open. Just tuck it away and don't use it.

Ready to stop guessing and start improving? Score Machine gives you the AI-powered analysis needed to find the quickest path to a higher score. Get your personalized blueprint today.