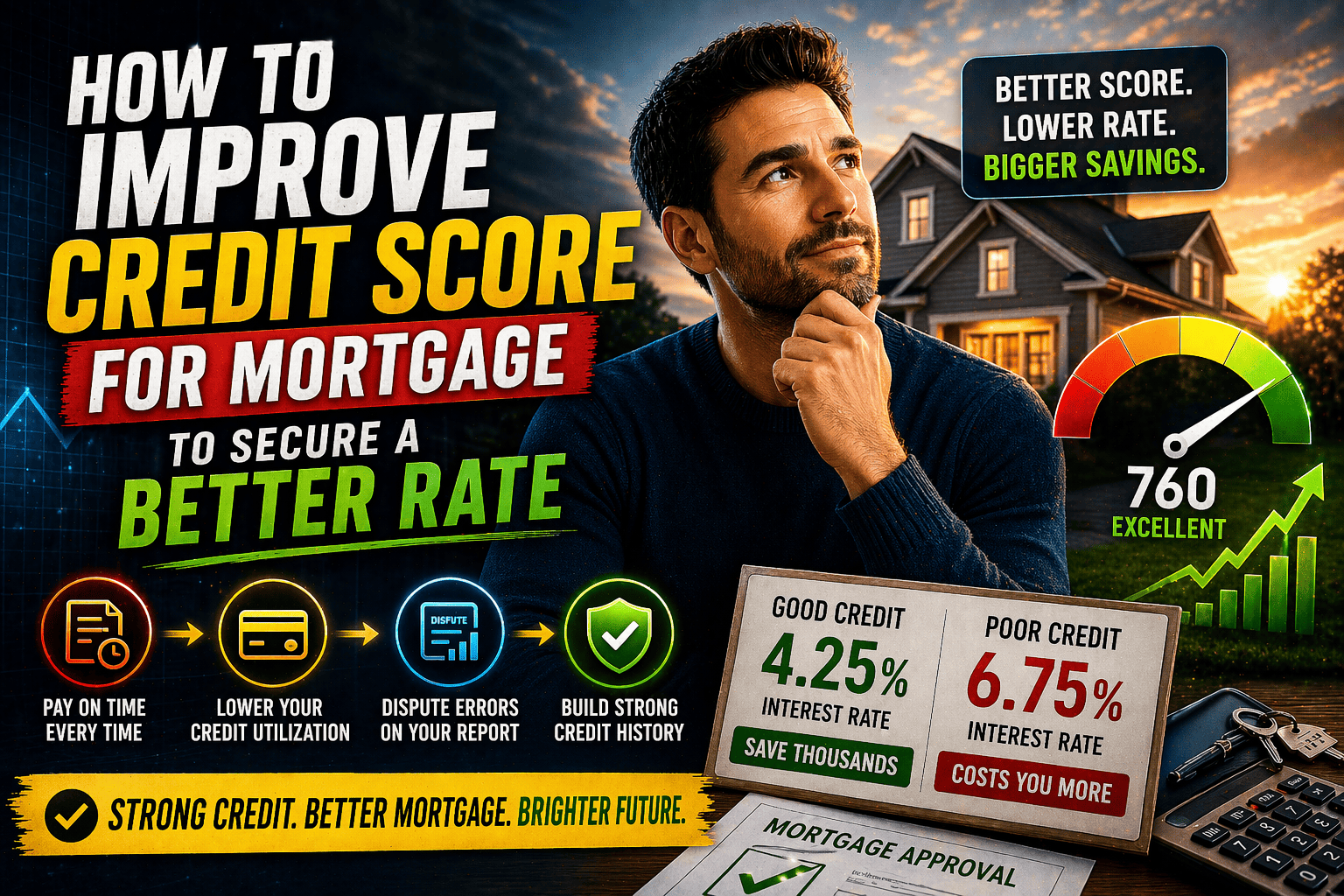

When you’re trying to lock in a great mortgage rate, almost everything comes down to your credit score. This guide is your roadmap to improve your credit score for a mortgage, but we're going to skip the generic advice. Instead, you'll get a practical, step-by-step action plan designed specifically for home buyers. The mission here is to show you exactly how even small, strategic changes can save you thousands over the life of your loan.

Your Path to a Mortgage-Ready Credit Score

Let's turn the abstract idea of "credit" into a real financial advantage. That three-digit score is way more than just a number—it’s a snapshot of your financial habits that lenders use to predict how likely you are to repay a home loan. A higher score tells them you’re a low-risk borrower, which is your key to unlocking better interest rates and friendlier loan terms.

This isn’t just theory; the real-world impact is huge. A seemingly small bump in your score can save you a surprising amount of money every single month. Over 30 years, that adds up to tens of thousands of dollars. Think of this as a strategic journey with a clear destination: homeownership on the best possible terms.

The Power of Data-Driven Credit Improvement

As the lending world gets more competitive, homebuyers are getting smarter about their credit. The data proves it. Back in 2016, the average FICO Score for someone with a mortgage was 739. Fast forward to the second quarter of 2024, and that average has climbed to a solid 758. That 19-point jump shows a clear trend: focusing on credit health is a direct path to getting a mortgage. You can dig into the numbers yourself with Experian's research on mortgage borrower credit scores.

This is where sophisticated tools can make all the difference. For funding companies, the ability to turn a near-miss applicant into a funded loan is the key to growth. A credit intelligence platform like Score Machine can be a game-changer. It uses AI to analyze a credit file just like an underwriter would, creating a blueprint of specific actions a person needs to take to get approved. This process directly increases funding by identifying a clear path to qualification for applicants who would otherwise be denied.

Instead of just saying "no," a lender can offer a clear, actionable path to "yes." This doesn't just increase funded loans; it builds trust and loyalty with clients for the long haul.

Here’s a real-world example: A business loan applicant gets denied because their credit utilization is too high. Score Machine can instantly pinpoint which accounts need to be paid down and by exactly how much. With that targeted guidance, the applicant can quickly fix their credit profile, allowing the funding company to turn a denial into an approval, increase its funding volume, and boost its reputation in the market.

Taking a Hard Look at Your Credit Reports

Before you can even think about building a mortgage-ready credit profile, you have to see exactly what a lender sees. This means going way beyond that three-digit score you see on an app. We're talking about a full audit of your credit reports from all three major bureaus: Equifax, Experian, and TransUnion.

It’s an absolute must to review all three. I’ve seen cases where two reports are clean, but one has a forgotten medical collection or an old late payment that torpedoes an application. Don't let that be you.

You're legally entitled to get your reports for free every single week. The only place to do this safely and without getting roped into a paid service is the official, federally authorized source: AnnualCreditReport.com. Steer clear of any look-alikes.

Playing Detective: What to Look for Beyond the Score

Once you have the reports in hand, your job is to become a credit detective. You are hunting for any and all inaccuracies that could be unfairly dragging down your score and putting your mortgage approval in jeopardy. Even one seemingly small error can have a huge impact.

Here's your checklist for what to scrutinize on each report:

- Personal Info: Is your name (and any old variations), address history, and Social Security number perfect? Identity mix-ups are far more common than you'd think.

- Account Status: Go line by line. Are accounts you paid off still showing a balance? Are there any late payments listed for months you know you paid on time?

- Account Ownership: Do you recognize every single account? Be ruthless here. A credit card you never opened is a massive red flag for identity theft.

- Outdated Bad News: Most negative marks, like late payments or collections, are supposed to fall off after seven years. Bankruptcies can hang around for up to ten. Make sure these old blemishes have actually been removed.

- Cloned Accounts: It happens. Sometimes a single debt gets listed twice by mistake, which can incorrectly inflate what you owe and double its negative impact.

A particularly nasty error I've seen is the "zombie mortgage"—a second mortgage that was supposedly discharged years ago but suddenly reappears on a report. The Consumer Financial Protection Bureau has even flagged a rise in these cases. They can completely derail a new mortgage application out of the blue.

The Right Way to Dispute Inaccuracies

Finding an error is half the battle; getting it fixed is the other. Thanks to the Fair Credit Reporting Act (FCRA), you have the right to dispute anything that’s inaccurate. While clicking the "dispute" button online is tempting, sending a formal dispute letter via certified mail gives you a paper trail that’s hard to ignore.

Here’s how to do it effectively:

- Write a Simple, Factual Letter: State the facts clearly. Identify the bureau, the account number in question, and exactly why the information is wrong. Keep emotion out of it—just the facts.

- Attach Your Proof: Include copies (never send your originals!) of any evidence you have. This could be a bank statement showing you paid on time, a letter from a creditor confirming a zero balance, or a police report if you suspect fraud.

- Send It Certified Mail: Mail your letter and documents to the credit bureau. Using certified mail with a return receipt requested is your proof that they received your dispute and when the clock started ticking.

The bureaus generally have 30 to 45 days to investigate your claim. They have to notify you of the results and send you a free, updated copy of your report if a change was made. This is how you systematically improve your credit score for a mortgage—by knocking down the errors that are holding you back.

Nail Your Payment History and Credit Utilization

If you’re going to focus your energy anywhere, this is it. Your payment history and how much credit you're using are the two heavy hitters in your credit score. Together, they account for a massive 65% of your FICO score, so any improvements you make here will give you the most bang for your buck.

Getting these two areas right is the fastest way to improve your credit score for a mortgage. Lenders look at these first and foremost because they tell a clear story about how you handle your financial obligations.

The Power of a Perfect Payment History

Your payment history is king. It makes up 35% of your FICO score, and mortgage lenders are obsessed with it. You absolutely must avoid any new late payments when you're preparing for a home loan. The numbers show why: first mortgage delinquencies (60+ days past due) hit 1.27% in Q2 2025, with FHA loans making up 35% of those late payers.

On the flip side, consistent on-time payments work wonders. The average credit score for people with mortgages climbed from 739 to 758 by Q2 2024, and that’s largely thanks to good payment habits. You can dig into more of these industry trends in TransUnion's latest report.

But what if you already have a blemish on your record, like a late payment or a collection? Don't panic. You have a couple of solid options.

One of my favorite lesser-known strategies is the goodwill letter. If you've been a great customer for years but had one slip-up—maybe you were in the hospital or lost a job—you can write to the creditor. Politely explain what happened and ask for a "goodwill adjustment" to remove the negative mark. It’s not guaranteed, but for a single mistake in an otherwise clean history, it’s always worth the effort.

For something more serious, like an account in collections, you can try negotiating a "pay for delete." This is exactly what it sounds like: you offer to pay the debt (or a settled amount) in exchange for the collection agency completely removing the account from your credit report. This is huge. A "paid" collection is better than an unpaid one, but a deleted collection is like it never happened.

Crucial tip: Always, always get the pay-for-delete agreement in writing before you send them a dime.

Taming Your Credit Card Balances

Your credit utilization ratio (CUR) is the second-biggest piece of the puzzle, accounting for 30% of your score. It’s simply the total of your credit card balances divided by your total credit limits. A high ratio screams "financial stress" to lenders.

You've probably heard the advice to keep your utilization below 30%. That’s good general advice, but for a mortgage, the bar is much higher.

When you're prepping for a mortgage application, your target for overall credit utilization should be under 10%. Anything higher can raise red flags. Lenders see low utilization as a sign of rock-solid financial health, which gets you better interest rates.

This doesn't mean you need a zero balance on every card. Lenders actually like to see that you can use credit responsibly. The trick is to keep the balances that get reported to the credit bureaus as low as possible.

Here are a few pro moves to get your utilization down fast:

- Pay Before Your Statement Date: Most people wait for their bill and pay by the due date. The problem is, your card issuer reports your balance to the bureaus after the statement closing date. To beat the system, make a payment a few days before your statement closes. This way, a much smaller balance gets reported, and your utilization plummets instantly.

- Ask for a Higher Limit: Have a card you've managed well for a while? Call the issuer and ask for a credit limit increase. If they approve it, your utilization ratio drops immediately without you paying off any debt. Just ask if they'll do it with a "soft pull" so you can avoid a hard inquiry on your credit.

- Spread the Debt Around: If you have one card that's nearly maxed out and others with zero balances, it can hurt your score. Consider moving some of that balance to another card with plenty of available credit. This lowers the high utilization on the one card and can improve your overall ratio.

Putting your efforts into these two key areas will deliver the biggest and fastest improvements to your credit score. This isn't just about playing a game with numbers; it's about building the kind of strong financial profile that underwriters love to see.

How Your Credit Score Impacts Mortgage Costs

A few points on your credit score can mean the difference of tens of thousands of dollars over the life of your loan. This table shows just how much you can save by boosting your score before you apply for a mortgage.

| Credit Score Range | Example APR | Monthly Payment (on $300k loan) | Total Interest Paid |

|---|---|---|---|

| 760-850 (Excellent) | 6.25% | $1,847 | $364,920 |

| 700-759 (Good) | 6.50% | $1,896 | $382,560 |

| 660-699 (Fair) | 7.10% | $2,016 | $425,760 |

| 620-659 (Needs Work) | 7.85% | $2,168 | $480,480 |

As you can see, jumping from a "Fair" score to an "Excellent" one could save you $171 every month and more than $115,000 in total interest. That's real money you can put toward other financial goals. It’s why taking the time to work on your credit is one of the smartest financial moves you can make.

Building a Stronger Credit History From the Ground Up

A low credit score is an obvious red flag for lenders, but a "thin" credit file can be just as problematic. If you don't have much credit history, underwriters get nervous. They want to see a long, consistent track record of you responsibly handling debt, so a sparse file makes it hard for them to predict how you'll manage a mortgage.

If your file is looking a little empty, it’s time to be proactive. This isn't just about avoiding late payments; it's about strategically adding positive information to your credit report to build the kind of robust profile that gets a lender's attention.

Get a Quick Boost as an Authorized User

One of the fastest ways to add some serious history to your file is to become an authorized user on a credit card held by a family member with a stellar credit record. When they add you to their account, you essentially inherit its history. The entire positive track record of that card—its age, high credit limit, and perfect payment history—suddenly appears on your credit report.

Think of it like getting a credit history transplant. If your parent has a credit card they've paid on time for 15 years and they keep the balance low, that positive history can instantly lengthen your own and drop your overall credit utilization. It's a powerful first step.

A quick word of caution: Before you jump on this, double-check two things. First, make sure the credit card company actually reports authorized user activity to all three credit bureaus (most do, but not all). Second, and this is crucial, confirm the primary cardholder has a perfect payment history and keeps the balance well below 30% of the limit. If they slip up and miss a payment or run up the balance, it will damage your score, not help it.

Build Your Own Track Record

Being an authorized user is a great hack, but lenders ultimately want to see that you can manage credit on your own. This is where tools designed specifically for credit building come in handy. Secured credit cards and credit-builder loans are fantastic for creating a new, positive payment history from scratch.

Here’s a quick look at how they work:

-

Credit-Builder Loans: These are almost like a reverse loan. You make small, consistent payments to a lender, who holds the funds for you in a savings account. Once you've paid the full amount over a set term (usually 6-24 months), the money is released back to you. The real magic is that all those on-time payments have been reported to the credit bureaus.

-

Secured Credit Cards: To get one of these, you'll put down a small cash deposit, often around $300, which then becomes your credit limit. You use it just like a regular credit card. Make small purchases, pay the bill on time, and that responsible behavior gets reported. After a while, many issuers will upgrade you to a standard, unsecured card and refund your deposit.

Both of these are low-risk methods for adding a brand-new tradeline with a perfect payment history, which is precisely what you need to improve your credit score for a mortgage.

The New Frontier: Using Alternative Data

The world of credit scoring is finally catching up with real life. Lenders are starting to recognize that traditional credit reports don't paint a complete picture. This is where alternative data—things like your rent and utility payment history—is changing the game.

This is a huge deal, especially with the rollout of newer scoring models. Models like FICO 10T and VantageScore 4.0 are designed to give more people a fair shot at a mortgage by predicting risk more accurately. For instance, FICO 10T is expected to increase mortgage approvals by 5% while simultaneously cutting delinquency rates by 17% for borrowers with scores over 680. VantageScore 4.0 goes even further by analyzing up to 24 months of trended data and incorporating information like rent payments, which helps provide a score to people who were previously "unscorable." You can read more about how these new models are changing lending and opening up new opportunities.

For funding companies, this shift represents a massive opportunity to increase their funding volume. Instead of relying on old, rigid systems, platforms like Score Machine allow them to analyze these expanded data sets. This empowers them to identify high-quality, fundable applicants who might have been automatically rejected by outdated models.

Imagine a borrower with a thin file being turned away. A funding company using Score Machine can see that same applicant has a perfect rental payment history. Armed with that insight, they can guide the applicant on how to get that positive data reported to the bureaus, turning a potential "no" into a definite "yes." This proactive approach doesn't just save a single deal—it unlocks a new pool of qualified borrowers, directly increasing the company's funded loans.

Managing Your Credit in the Final Stretch: The Pre-Application Phase

Think of the last few months before you apply for a mortgage as a "quiet period" for your credit. This is where all your hard work comes together, and the primary goal is simple: stability. Underwriters are looking for a predictable, responsible financial history, and any sudden moves now can send up a red flag and jeopardize your approval.

The progress you've made is valuable, so now it's time to protect it. That means you absolutely must avoid applying for any new credit. It doesn't matter how great the offer is—a new car, a retail card with a 20% discount, a personal loan—each application generates a hard inquiry that can ding your score. One inquiry might not seem like a big deal, but a cluster of them signals financial distress to a lender.

On that same note, don't close old credit card accounts, even the ones you haven't touched in years. It might seem like a good housekeeping move, but it can backfire badly. Closing an old account shrinks your average credit age and, just as importantly, reduces your total available credit. This can cause your credit utilization ratio to spike overnight, dropping your score right when you need it most.

Your Final Approach to Mortgage Readiness

In the 6 to 12 months leading up to your target application date, your focus should shift from major credit repair to careful maintenance. You're no longer performing surgery; you're just keeping the patient healthy. This means locking in your debt reduction plan, putting a freeze on any new credit applications, and keeping a close eye on your reports for any surprises.

This is also where savvy lenders use specialized tools to increase funding by ensuring more applications make it through underwriting. A platform like Score Machine can run a final, pre-underwriting analysis on an applicant's file. It acts as a safety check, quickly verifying that they haven't opened any new accounts or suddenly maxed out a credit card, confirming the profile is still stable and strong.

This final check is a game-changer for funding companies. It allows a loan officer to catch any last-minute problems before the file hits the underwriter's desk, which massively boosts the odds of a smooth, one-touch approval. For the lender, it means fewer rejections and more funded loans. For you, it means less stress and fewer nasty surprises.

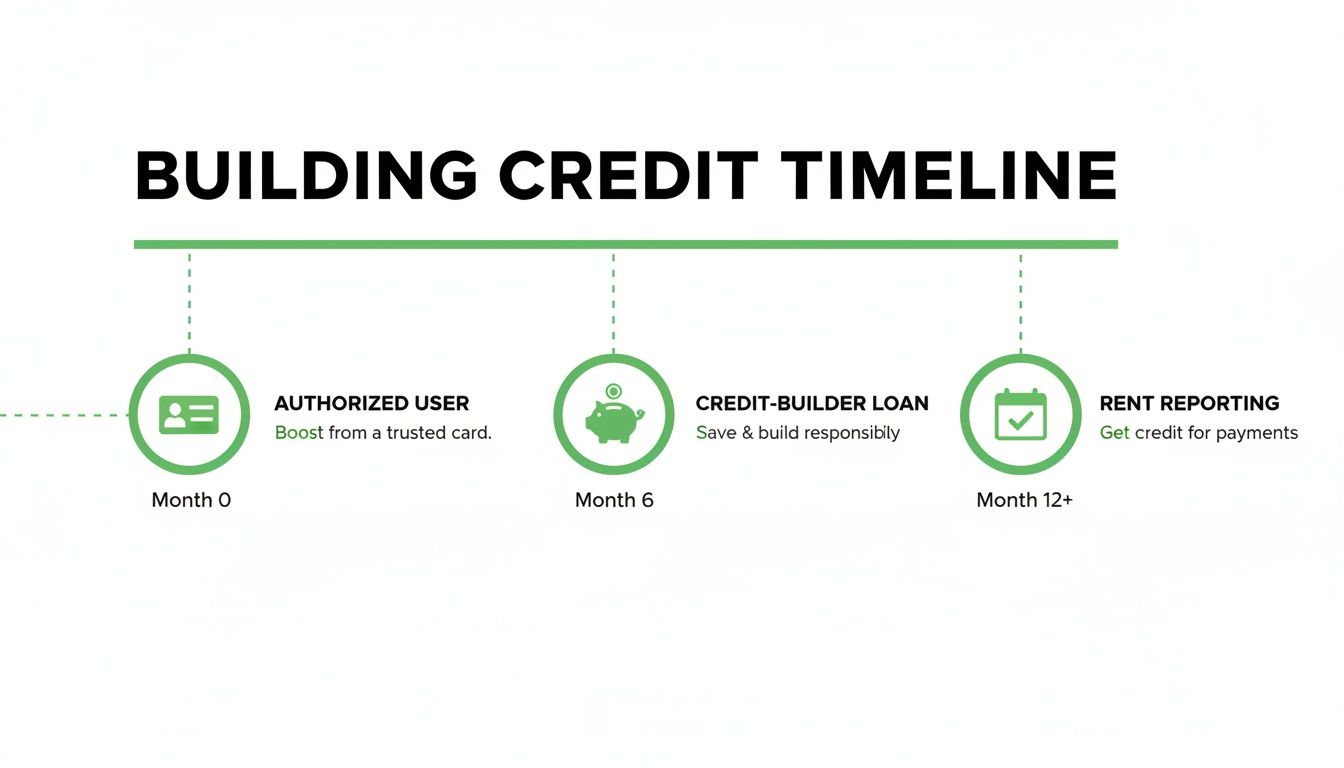

A Visual Timeline for Building Credit

Not everyone starts with a perfect credit file. If you're building from the ground up, this visual shows a few powerful ways to add positive history to your report over time.

As you can see, things like becoming an authorized user on a family member's account, taking out a small credit-builder loan, or using a service to report your rent payments can be fantastic strategies for creating a more robust credit profile.

Your Mortgage Credit Improvement Timeline

To give you a clear roadmap, I've put together a checklist outlining the key moves to make in the year before you apply for your mortgage. Think of this as your game plan for getting your credit score into prime condition for underwriting.

| Timeline | Action Item | Why It's Important |

|---|---|---|

| 12 Months Out | Pull all three credit reports and begin disputing errors. | Gives you plenty of time for bureaus to investigate and correct inaccuracies without rushing. |

| 6-9 Months Out | Focus on aggressive debt paydown, targeting high-utilization cards first. | Systematically lowering your credit utilization ratio delivers the biggest score boosts. |

| 3-6 Months Out | Freeze all new credit applications. No car loans, no new cards. | Prevents new hard inquiries from temporarily lowering your score right before you apply. |

| 1-3 Months Out | Keep all credit accounts open and active with small, regular charges. | Shows lenders you can responsibly manage existing credit without taking on new debt. |

| Application Month | Monitor your credit weekly for any fraudulent activity or unexpected changes. | Ensures your file is clean and stable at the exact moment the lender pulls your report. |

Following this timeline doesn't just help your score—it builds the kind of clean, stable credit history that underwriters love to see, making your path to homeownership that much smoother.

Got Questions About Your Mortgage Credit Score? We've Got Answers.

As you get closer to applying for a mortgage, you'll inevitably have questions. It’s that critical phase where every point on your credit score feels like it could make or break your chances. Let's walk through some of the most common questions that come up and get you the straightforward answers you need.

"How Fast Can I Actually Raise My Credit Score?"

This is the big one, and the honest answer is: it depends entirely on what’s holding your score back.

If your score is being dragged down by high credit card balances, you’re in luck. You could see a significant jump in as little as 30 to 45 days just by paying them down. As soon as the credit bureaus get the update, your credit utilization ratio plummets, and your score often shoots right up. It’s one of the fastest fixes out there.

On the other hand, if you're wrestling with bigger issues like late payments, collection accounts, or a past bankruptcy, patience is key. These negative marks can linger on your report for seven to ten years. While you can try things like goodwill letters or negotiating a pay-for-delete, the real long-term solution is building a fresh history of on-time payments. That’s what truly rebuilds trust and your score over time.

For a funding company, this timeline isn't just a waiting game—it's a direct threat to their bottom line. Every delayed applicant is a lost funding opportunity. This is why having a precise, actionable game plan is so valuable for increasing their deal flow.

A platform like Score Machine, for instance, doesn't just point out the problems. It builds a custom blueprint that tells a loan officer exactly which accounts a borrower needs to pay and by how much to hit a target score. This turns a vague, multi-month delay into a clear set of instructions, helping the funding company get applicants "mortgage-ready" significantly faster and close more loans.

"What's the Real Minimum Score I Need for a Loan?"

There's no single magic number that works for every loan, as the minimums change based on the loan type and the lender's own rules. But, here are the general goalposts to keep in mind:

- FHA Loans: A favorite among first-time buyers, these government-backed loans have some of the most flexible credit requirements. Most lenders will want to see a score of at least 580, which lets you qualify for a down payment as low as 3.5%.

- VA Loans: These are a fantastic benefit for eligible veterans and service members. While the Department of Veterans Affairs doesn't set a hard credit score minimum, the lenders who actually issue the loans do. You'll typically need a score of around 620 to get approved.

- Conventional Loans: Since these aren't backed by the government, the standards are a bit tougher. The usual starting point for a conventional loan is a 620 credit score. But if you want the best interest rates and lower fees, you really want to be aiming for 740 or higher.

Just remember, these are the scores to get your foot in the door. A higher score always means better options and, more importantly, a lower monthly payment.

A funding company's ability to increase funding often hinges on correctly matching applicants to the right product. By analyzing a credit file, an intelligent platform can identify that an applicant who fails to qualify for a conventional loan might be a perfect fit for an FHA loan. This insight allows the loan officer to pivot, saving the deal and directly increasing the company's funded loan volume.

"Should I Close My Old Credit Cards Before Applying?"

It’s a tempting thought—clean up your finances, right? But for the love of your credit score, do not do this. Closing old credit cards right before applying for a mortgage is one of the most common mistakes and can seriously backfire.

Here’s why. First, you'll shorten the average age of your credit history, a factor that makes up 15% of your FICO score. Lenders love to see a long, stable credit history. Second, you’ll slash your total available credit, which can cause your credit utilization ratio to skyrocket.

Imagine this: you have $2,000 in balances across all your cards and a total credit limit of $10,000. Your utilization is a healthy 20%. If you close an old, unused card with a $5,000 limit, your total credit limit instantly drops to $5,000. Now, that same $2,000 balance represents a 40% utilization rate, which can send your score tumbling.

So, what should you do instead? Keep those old accounts open. Use them for a small, recurring purchase every few months (like a coffee or a subscription) and pay it off immediately. This keeps them active and working for you, not against you.

At Score Machine, we believe getting your credit ready for a mortgage shouldn't be a mystery. Our AI-powered platform shows you exactly what an underwriter sees, turning confusing credit data into a simple, step-by-step plan to get you funded. Start building your score with confidence at https://thescoremachine.com.