Boosting your credit score after bankruptcy isn't about waiting—it's about taking immediate, smart action. The plan is straightforward: get your credit reports squeaky clean, open a few strategic lines of new credit (like a secured card), and prove you can manage your finances responsibly by paying everything on time. The most important thing you can do is start building a new track record of responsible credit use the moment your bankruptcy is discharged.

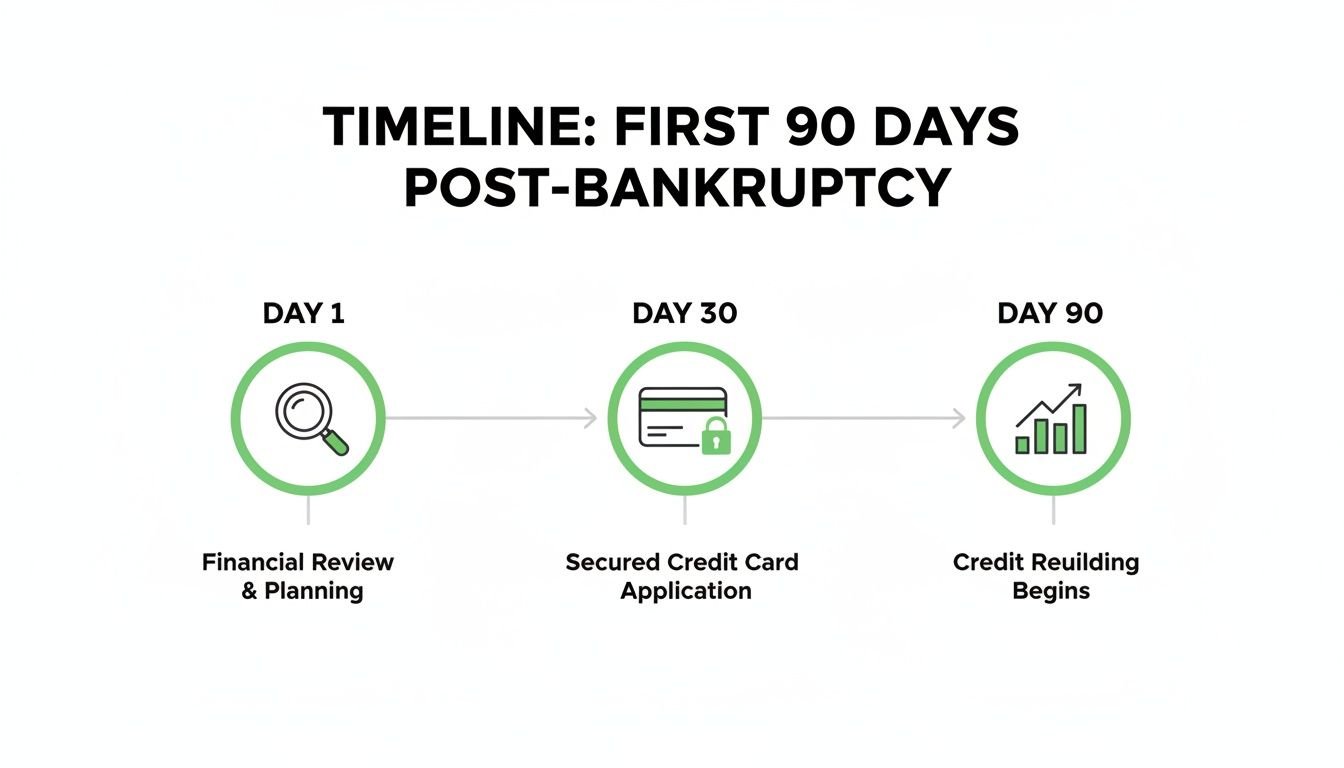

Your Post-Bankruptcy Strategy: The First 90 Days

The first three months after your bankruptcy discharge are absolutely crucial for your financial recovery. Think of it as a fresh start, where every small, deliberate move you make has a major impact. A lot of people assume they're stuck in credit purgatory for years, but that's just not true. You can start building the foundation for a much stronger credit profile right away. This 90-day window is your chance to set the tone for the entire journey ahead.

This isn't just about kicking old habits to the curb. It's about actively creating a new financial identity that lenders will eventually see as trustworthy and low-risk. The steps you take now—from correcting your credit reports to carefully adding new credit—will directly affect how quickly you can hit big financial milestones, like getting a car loan or a mortgage.

This timeline breaks down those critical first steps, showing you what to do from the day of your discharge through the first three months.

As you can see, acting quickly is the best way to build momentum on your path to credit recovery.

The Power of an Underwriting-Style Blueprint

Instead of just guessing what lenders want, what if you had a clear, data-driven plan? This is where modern tools like Score Machine can make a huge difference. It looks at your credit file the same way a loan underwriter would, assessing your "fundability" rather than just spitting out a score. The result is a personalized blueprint showing your exact strengths, weaknesses, and the specific steps you need to take.

This kind of analysis is incredibly useful for funding companies, too. When they run a potential client's report through Score Machine, they can pinpoint the exact issues causing a denial. Instead of just saying no, the company can give the applicant a clear, actionable roadmap to getting approved in the future.

This strategy turns a hard 'no' into a 'not yet, but here's how.' It helps funding companies cultivate a pipeline of future clients, boosting their long-term approval rates and building real trust by offering genuine, helpful guidance.

By educating applicants who would have otherwise been turned away, companies can ultimately increase their funding approvals.

Post-Bankruptcy 90-Day Action Plan

The following table outlines your immediate priorities. Work through this checklist to ensure you're building a solid foundation from the very beginning.

| Action Item | Why It's Critical | Tool or Resource |

|---|---|---|

| Pull all 3 credit reports | You need to see exactly what lenders see. Errors are common after bankruptcy and can drag your score down. | AnnualCreditReport.com (official source for free reports) |

| Dispute all reporting errors | Discharged debts must show a $0 balance and be marked "Included in Bankruptcy." Incorrect data hurts your score. | Credit bureau online dispute portals (Equifax, Experian, TransUnion) |

| Open a secured credit card | This is the fastest way to start building a new, positive payment history. It's the #1 rebuilding tool. | Major bank or credit union secured card offerings |

| Consider a credit-builder loan | Adds a different type of credit (installment loan) to your file, which helps your credit mix and shows stability. | Self, Credit Strong, or local credit unions |

| Become an authorized user | If you have a trusted family member with excellent credit, this can add their positive history to your report. | Ask a family member with a long-standing, low-balance credit card |

| Monitor your credit score | Tracking your progress keeps you motivated and helps you spot new issues or errors immediately. | Free services like Credit Karma or your credit card's dashboard |

Sticking to this plan for the first 90 days will put you miles ahead in your credit recovery journey.

Your Immediate Post-Discharge Checklist

Your very first move is to get copies of your credit reports from all three main bureaus: Equifax, Experian, and TransUnion. By law, you can get them for free once a year. Your job is to go through them line by line to make sure every account included in your bankruptcy is now reporting correctly.

- Zero Balance Reporting: All discharged debts must show a $0 balance.

- "Included in Bankruptcy" Notation: The accounts should have a note like "Discharged in Chapter 7/13 Bankruptcy."

- No Late Payments Post-Discharge: Check that there are no new late payments reported on these accounts after your filing date.

If you spot any mistakes, dispute them right away. An account still showing a balance can crush your score and get you denied for the new credit you need. Interestingly, it's not uncommon to see a score jump right after discharge. A study from the Federal Reserve Bank of Philadelphia found that the average credit score for Chapter 7 filers increased by 82.1 points soon after discharge. You can discover more insights about these recovery timelines and what they signal for your financial future.

Choosing the Right Tools to Rebuild Credit

Okay, with the bankruptcy discharged, you're looking at a fresh start. Every financial move you make from here on out is a direct message to future lenders. This is where your strategy has to get tactical. We're moving past generic advice and picking the specific tools that will actively prove you're a responsible borrower now.

Each of these rebuilding tools has a specific job to do. The goal isn't to rack up as many accounts as you can. It’s about carefully building a balanced credit profile that shows you can handle different kinds of credit. A secured card demonstrates you can manage a revolving balance, while something like a credit-builder loan proves you're reliable with fixed payments.

The Power of Secured Credit Cards

A secured credit card is, without a doubt, the single most powerful tool you can use to rebuild credit after bankruptcy. It functions just like a standard credit card, but with one key difference: you put down a refundable security deposit, and that amount usually becomes your credit limit. This simple step removes the lender's risk, which is why they are so much easier to get approved for.

So, why is this so effective? Because your entire payment history with that card gets reported to all three major credit bureaus. Every single on-time payment creates a new, positive mark on your credit file, directly helping to offset the negative impact of the bankruptcy.

Think of it this way: you get a secured card with a $300 deposit, giving you a $300 credit limit. Use it for a small, predictable monthly bill—like a Netflix subscription—and then pay the balance in full every month. Just like that, you're building a flawless payment history.

Adding an Installment Loan to the Mix

Secured cards are fantastic for handling revolving credit, but lenders also want to see proof you can manage an installment loan—one with fixed payments over a set term. This is where credit-builder loans are incredibly useful.

These loans are unique because they work backward. You don't receive any cash upfront. Instead, the lender puts the loan amount into a locked savings account for you. You then make regular monthly payments on that amount. Once you've paid off the entire "loan," the money is released to you.

The real benefit is that every one of those on-time payments is reported to the credit bureaus. This adds a positive installment loan to your report, which diversifies your credit mix—a factor that makes up 10% of your FICO score. Having both revolving (credit cards) and installment (loans) accounts on your report makes you look like a much more stable and reliable borrower.

A common misconception is that all debt is bad after bankruptcy. In reality, strategically using tools like credit-builder loans is one of the most proactive ways to prove your creditworthiness and accelerate your score's recovery.

This two-pronged approach shows you can juggle different financial responsibilities, which is exactly what underwriters want to see. Before you jump in, it's smart to gauge where you stand. You can get a clearer picture of your financial situation by reviewing a detailed guide on credit readiness.

The Authorized User Strategy

If you have a trusted family member or friend with a rock-solid credit history, becoming an authorized user on one of their credit cards can give you a quick leg up. When they add you to their account, the card's positive history—its age, low utilization, and perfect payment record—can be mirrored on your credit report.

This can be a great boost right after bankruptcy when your own credit file feels a little empty. But it's not a silver bullet. Lenders are savvy; they know you aren't the one primarily responsible for the payments, so this tradeline carries less weight than an account in your own name. Think of it as a helpful supplement, not a replacement for building your own credit.

Finally, don't fall for the myth that bankruptcy locks you out of major goals like buying a home. It's simply not true. Many people successfully qualify for FHA loans just two years after a Chapter 7 discharge because the guidelines are more forgiving. The key is to know the specific waiting periods for different types of loans so you can set a realistic timeline for yourself.

Mastering Your Credit Habits for Score Growth

Getting approved for that first secured card or credit-builder loan feels like a huge win, and it is. But that's just the opening act. The real work—the part that actually rebuilds your score—begins now. It all comes down to how you manage these new accounts.

Two factors absolutely dominate your credit score, making up a combined 65% of the entire calculation: your payment history (35%) and your credit utilization ratio (30%). If you can nail these two things, you're on the fastest and most reliable path to a great score after bankruptcy. Every on-time payment you make is a fresh, positive mark that starts to bury the bankruptcy in your past.

Make Every Payment on Time, Without Fail

Your payment history is, without a doubt, the heavyweight champion of credit scoring factors. After a bankruptcy, you have to assume lenders are watching this one thing more than anything else. They want to see if you’ve truly turned a corner. A single late payment can wipe out months of progress, so this part is non-negotiable: you must pay on time, every time.

Don't overcomplicate it. Building a perfect payment history is all about creating a system that makes it impossible to fail.

- Set Up Autopay: The very first thing you should do with any new account is set up automatic payments for at least the minimum amount. Think of this as your ultimate safety net. It ensures you’ll never miss a due date because life got busy.

- Use Calendar Alerts: Autopay is great, but don't rely on it alone. I always tell people to set a reminder on their phone's calendar for a few days before the due date. This gives you a chance to look over the statement and, more importantly, pay the entire balance off.

- Always Pay More Than the Minimum: While your autopay safety net covers the minimum, your personal goal should be to pay the full statement balance every single month. This is how you avoid debt, sidestep interest charges, and keep your utilization in check.

A flawless payment history becomes your new financial reputation. After a bankruptcy, think of each on-time payment as a vote of confidence you are casting for yourself. It’s the most powerful signal you can send to future lenders.

This kind of consistent behavior proves you're a low-risk borrower, which is exactly the story you need to tell during your recovery.

The Power of Low Credit Utilization

If payment history is about consistency, credit utilization is all about restraint. This ratio is simply a measure of how much of your available credit you’re using at any given time. It's calculated by dividing your total credit card balances by your total credit limits.

You’ll hear a lot of advice to keep it below 30%. That’s not bad advice, but for someone rebuilding after bankruptcy, you need to be more aggressive. Your target should be under 10%.

Let’s make this real. Say you have a secured card with a $500 limit.

- Scenario A (50% Utilization): You end the month with a $250 balance. To a lender, this can look like you're stretched thin and relying on credit to get by.

- Scenario B (9% Utilization): You use the card for a $45 streaming subscription and pay it off. This tells lenders you're in total control—using credit as a convenient tool, not a financial crutch.

The difference in your score between those two scenarios can be staggering. Keeping your utilization super low is one of the quickest ways to see a jump in your score, sometimes in just a couple of months.

It’s completely normal to feel shocked by the initial score drop after a bankruptcy. But that damage isn't permanent, and its influence fades over time. A FICO study showed that someone with a 680 score might see it fall by 130-150 points, whereas a person with a 780 score could see a massive 220-240 point drop.

The key thing to remember is that as the bankruptcy gets older, its negative power shrinks. This makes all the new, positive habits you're building even more impactful. You can discover more insights about bankruptcy's effect on your score to get a better handle on the road ahead. Knowing what to expect makes it easier to stay focused on the consistent, positive actions that will fuel your comeback.

A Better Way for Lenders to Get More Funding Approvals

As a lender, you're constantly walking a tightrope. You have to manage risk, but you also need to approve loans to grow your business. For decades, the process has been brutally simple: if an applicant doesn't fit the box, they get a denial letter. That's the end of the road. It’s a dead-end interaction that helps nobody.

But what if you could turn that denial into your next approval?

This isn't just wishful thinking. With the right approach and technology, you can shift from a rigid "yes" or "no" system to a more dynamic one. Instead of just looking at a static credit score, platforms like Score Machine can give you a full underwriting-style blueprint of an applicant's real fundability in just a few seconds.

This changes everything. Suddenly, you can offer real value even when you can't offer a loan today, setting yourself up for a much stronger business down the line.

Turn Today's Denials into Tomorrow's Pipeline

Let's get practical. Say an applicant comes to you with a recent bankruptcy. Their profile is close, but not quite there. The old way? A flat "no." The new way is to give them a clear, personalized roadmap to get them approval-ready—based on your specific underwriting rules.

By using a tool like Score Machine, you can see exactly what’s holding them back. It's not a guess; it's data. This lets you give them concrete steps to take.

- Pinpoint the Real Problem: The analysis might reveal their recent bankruptcy isn't the main roadblock. The bigger issue could be two discharged accounts that are still incorrectly reporting a balance.

- Give Actionable Advice: You can tell them, "Your profile is solid, but you need to dispute those two specific errors with the credit bureaus." This is direct, helpful guidance.

- Provide a Clear Timeline: The system can also show that if they open a secured credit card and keep the balance low for six months, they'll likely meet your criteria for another look.

With this strategy, you’re not just sending people away. You're building a pipeline of future clients who see you as a partner, not a gatekeeper, because you offered a solution instead of a rejection.

You’re no longer losing a lead; you’re cultivating a future customer. By turning a denial into a 'not yet, and here's how,' you build incredible trust and dramatically increase the odds they'll come back to you when they're ready.

You’re actively de-risking your future applicant pool. You’re teaching them how to improve credit score after bankruptcy in a way that directly aligns with your own lending requirements. It's a win-win.

The Staggering Cost of Bad Data

This kind of guidance is critical, especially when you consider how often credit reports are wrong after a major financial event like bankruptcy. The cost of this inaccurate data is huge. A Consumer Reports investigation found that a shocking 34% of volunteers discovered at least one error on their credit reports.

For someone just getting back on their feet, an error showing a discharged debt as active can be a killer. It tanks their score and can block them from getting the very tools they need to rebuild. Our guide on loan preparation digs deeper into getting financials in order before applying. These errors are precisely why proactive monitoring and correction are so vital.

When you help applicants spot and fix these problems, you're not just improving their odds of approval. You're showing them you’re committed to their financial health. In a sea of transactional lenders, that makes you a trusted advisor—and that’s a powerful competitive advantage.

Planning for the Big Stuff: Your Long-Term Strategy for Major Purchases

Rebuilding your credit isn't just an exercise in watching a three-digit number climb. It’s about getting your life back on track and unlocking your future. The real prize is being able to confidently apply for major life purchases—a reliable car, and especially, your own home.

This means shifting gears from the immediate, short-term repair tactics to a deliberate, long-range strategy. You need to build a financial profile that can withstand the intense scrutiny of an underwriter. It’s about more than just paying your bills on time; it's about understanding the game and playing it strategically.

Knowing the Lender's Timelines After Bankruptcy

One of the biggest questions I hear is, "How long until I can get a real loan again?" It's a source of a lot of anxiety, but the good news is there are clear, established waiting periods. They just vary depending on what you're trying to buy. Knowing these timelines gives you a realistic roadmap.

When it comes to mortgages, the waiting periods are pretty standard across the board:

- FHA & VA Loans: You’ll typically need to wait two years after a Chapter 7 is discharged. If you filed Chapter 13, you might be eligible after just one year of making your plan payments on time, though you'll need the court's approval.

- Conventional Loans: These have a longer fuse. Expect to wait four years from the discharge date of a Chapter 7.

Auto loans, on the other hand, are a different story. Lenders are generally more flexible. While the best lenders will want to see a year or two of solid credit history, you can often get a car loan much sooner. I've seen people get approved within six months of discharge, but be prepared for a higher interest rate.

The key takeaway here is that homeownership isn't a decade away—not even close. Think of these waiting periods as your runway. They give you a concrete timeframe to execute your rebuilding plan so that when the eligibility window opens, your application is as strong as it can possibly be.

Before you get too far down the road, it helps to see what your potential monthly payments might look like. A good mortgage calculator can help you estimate costs and set realistic savings goals that fit your timeline.

Your Timeline for Building a Loan-Ready Profile

To make your application pop, you need to show an underwriter a consistent pattern of responsible behavior. It's all about building a story of recovery and reliability.

Here’s a checklist of actions to take at key milestones, designed to build a profile that lenders love to see.

The First 6 Months Post-Discharge Your entire focus here is on laying a flawless foundation. No exceptions.

- Get Active Tradelines: You should have one or two open accounts reporting, like your secured card and a credit-builder loan.

- Achieve 100% On-Time Payments: Not a single late payment. This is absolutely non-negotiable.

- Keep Utilization Under 10%: Show lenders you aren’t desperate for credit. Live well below your means.

The 1-Year Mark Now you can start to carefully branch out and add a little more depth to your profile.

- Consider a Second Credit Card: If you started with just one secured card, you could apply for an unsecured card or even a second secured one. This proves you can juggle multiple revolving accounts responsibly.

- Ask for a Credit Limit Increase: Call your current card issuer and request a higher limit. The trick is to not increase your spending. This move instantly drops your credit utilization ratio.

- Check for Pre-Approvals: Use the soft-pull tools that many card issuers offer. This lets you see what you might qualify for without the ding of a hard inquiry.

The 2-Year Mark and Beyond At this point, you're shifting into pre-approval mode. The name of the game is stability.

- Go on a "Credit Freeze": For at least six months before you plan to apply for a mortgage, stop opening any new accounts. Lenders get really nervous when they see a flurry of recent credit-seeking.

- Pay Down Balances: Get all your credit card balances as close to zero as you possibly can.

- Build Up Your Savings: A great credit profile is only half the equation. Underwriters need to see that you have the cash for a down payment, closing costs, and reserves.

This strategic patience shows underwriters you haven't just recovered—you've become a meticulous and reliable borrower. The great news is this hard work pays off relatively quickly. Data shows that 43% of people with a bankruptcy on their record reach a score of 640 or higher within just one year. By the two-year mark, that number jumps to nearly two-thirds of filers. You can learn more about these credit score recovery findings and see just how fast a dedicated strategy can turn things around.

Common Questions About Credit After Bankruptcy

Going through bankruptcy brings up a ton of questions, and honestly, there's a lot of bad information out there. It creates stress you just don't need right now. Let's cut through the noise and get you some straight answers so you can move forward with a real plan.

So many people are convinced that filing for bankruptcy is a financial death sentence. It’s not. The whole point is to give you a clean slate, and your credit repair journey can begin the moment your case is discharged.

How Much Will My Score Drop After Bankruptcy?

There’s no magic number here—the hit your score takes really depends on where you were standing before you filed. If you had a high score, say 750, you could see a painful drop of 200 points or more. But if your score was already down around 580, the drop will be much less dramatic.

Think of it like this: the higher the climb, the longer the fall. But the most important thing to remember is that this impact fades. As you start adding new, positive payment history to your credit reports, the bankruptcy's influence shrinks month by month.

Can I Really Get Credit Again After Filing?

Yes. Absolutely, one hundred percent. The idea that you’ll never get a credit card or loan again is probably the biggest myth about bankruptcy. You'll likely be surprised to see credit card offers, especially for secured cards, show up in your mailbox just a few months after your discharge.

It might sound strange, but in a way, you can look like a less risky borrower to some lenders. They know you have minimal debt and can't file for bankruptcy again for several years. Seizing these opportunities and managing them perfectly is the foundation of rebuilding your credit.

What Is a Score Machine and How Can It Help Funding Companies?

A Score Machine is an advanced credit intelligence platform designed to give lenders and funding companies a deeper, more actionable understanding of an applicant's financial health. It moves beyond a simple credit score to provide a full "fundability" analysis, which mimics the detailed review an underwriter would perform.

This is a game-changer for funding companies because it helps them increase approvals. By identifying the specific issues holding an applicant back—like old accounts reporting incorrectly—the platform allows the company to provide a clear, step-by-step recovery plan. Instead of losing a lead to a denial, they cultivate a future customer.

By turning denials into a guided path toward approval, funding companies build a loyal pipeline of qualified applicants. This strategy directly leads to an increase in their overall funding volume because more applicants successfully return ready for approval.

It transforms the lending process from a simple "yes/no" transaction into a valuable, advisory relationship that drives future business.

Chapter 7 vs. Chapter 13: How Do They Affect My Score?

Both will ding your credit, but the reporting rules are a bit different. A Chapter 7 bankruptcy will stay on your credit report for up to 10 years. A Chapter 13, on the other hand, falls off after 7 years.

Because Chapter 13 includes a 3-to-5-year repayment plan, some creditors see it a little more favorably than a Chapter 7 liquidation. But when it comes to your actual recovery, the type of bankruptcy is far less important than what you do next. Your new, positive credit habits are what will truly drive your score back up.

Ready to stop guessing and start building? Score Machine digs into your credit report just like an underwriter would, giving you a clear, step-by-step plan to boost your fundability. Get your personalized blueprint today at https://thescoremachine.com.