If you want to build business credit, the very first move—the one you absolutely can't skip—is to draw a clear, undeniable line between your personal finances and your business finances. It's all about setting up a distinct legal entity, getting a federal tax ID for it, and then opening a bank account in its name. Getting these basics right is the only way to unlock real funding and keep your personal assets safe.

Laying the Groundwork for Business Credit

Before you even think about applying for a vendor account or a business card, you need to prove to the world that your business is a real, standalone operation. Think of it like pouring the foundation for a house. You can't start framing the walls until the concrete is set. Rushing past these first steps is a classic mistake I see entrepreneurs make all the time, and it almost always leads to denied applications and puts their personal assets on the line.

This isn't just about shuffling papers. You're creating a unique financial identity for your company—one that credit bureaus and lenders can see and track. Every move you make, starting now, builds that identity and signals whether you're a serious, fundable business or just a high-risk gamble.

Why You Must Separate Business and Personal Identity

Mixing your personal and business money is a surefire way to create chaos. When you run business transactions through your personal checking account, you end up with a tangled mess that makes it impossible for any lender to figure out how your company is actually doing.

Even more critical, it "pierces the corporate veil," which is the legal barrier between you and your company.

By setting up a distinct business entity, you're not just getting organized—you're building a legal firewall. That's what protects your home, your car, and your savings if the business ever runs into debt or legal trouble.

This separation is the heart and soul of business credit. It lets your company build its own reputation based on its own performance, completely separate from your personal credit score.

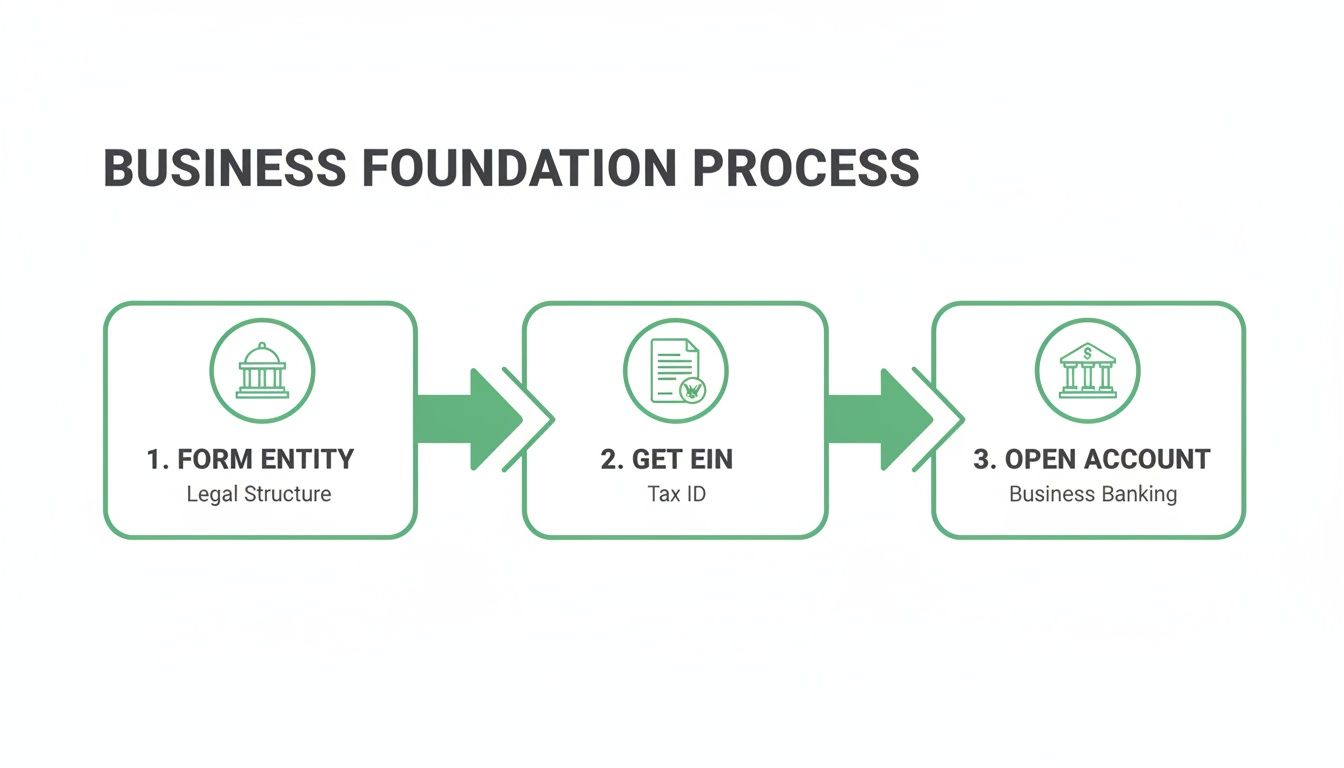

The Three Pillars of a Fundable Foundation

Getting this foundation right is pretty straightforward, but it takes intentional effort. The whole system of building business credit stands on three critical pillars. You have to put them in place before you do anything else.

- Form a Legal Business Entity: Your first real step is to officially structure your business. Creating a Limited Liability Company (LLC) or a Corporation (S-Corp or C-Corp) is what legally separates the business from you as a person. Trying to build business credit as a sole proprietorship is incredibly difficult because everything is tied directly to your personal credit file.

- Obtain an Employer Identification Number (EIN): The IRS issues this unique nine-digit number. Think of it as a Social Security Number for your business. You'll need it to file taxes, hire people, and—most importantly—open a business bank account and apply for credit under the company's name.

- Open a Dedicated Business Bank Account: Once you have your entity paperwork and your EIN, you have to open a business checking account. From that moment on, all business income and expenses must flow through this account. This creates the clean paper trail that lenders need to see when they're deciding whether to give you money.

This simple, linear process is how you establish your business's financial identity from the ground up.

Each step builds on the one before it, creating a legitimate foundation that both credit bureaus and lenders can easily recognize.

The demand for business funding is exploding. In fact, the global market for business credit cards hit $33.5 billion in 2023 and is expected to climb to $59.9 billion by 2032. This tells you just how much opportunity is out there when your business has strong credit.

Getting these foundational steps right is what positions you to tap into that growing market. It’s what elevates your company’s readiness for loans and cards, much like how a platform like Score Machine can analyze reports to flag fundability risks early on. To get a better sense of the opportunity, you can explore more data on the business credit card market.

Securing Your First Vendor and Trade Accounts

Okay, your business is legally set up, you have your EIN, and your finances are separate. Now it's time for the fun part—actually building your credit profile. This is where we move from paperwork to real-world action by opening your first vendor accounts, which you'll also hear called trade lines.

Think of these as the first building blocks for your business credit score. They're typically much easier to get than a traditional bank loan or a business credit card, and they have one critical job: to start reporting your positive payment history to the major business credit bureaus.

What Exactly Are Vendor and Trade Accounts?

At its core, a vendor account is just a line of credit from a company that sells goods or services. Instead of you paying with a card at checkout, they'll invoice you and give you net terms—like net-30, net-60, or net-90. All this means is you have 30, 60, or 90 days to pay the bill in full.

Every time you pay that invoice on time (or even better, early), the vendor reports that positive activity. Each payment acts like a vote of confidence, telling the credit bureaus that your company is reliable and meets its financial commitments. This is the absolute foundation of a strong business credit report.

Finding the Right "Starter" Vendors

Here’s a crucial detail many new business owners miss: not all vendors report your payments. You could be a perfect customer, paying every bill early for a year, but if that vendor doesn't report to the business credit bureaus, it does absolutely nothing for your credit profile.

The trick is to find "starter vendors." These are well-known suppliers that are friendly to new businesses and, most importantly, are known to report your payment history.

To get you started, here’s a quick look at some of the most common and effective starter vendor accounts. These are popular because they're relatively easy to qualify for and report to at least one major business credit bureau.

Starter Vendor Accounts for Building Business Credit

| Vendor Name | Products Offered | Typical Credit Terms | Reports To |

|---|---|---|---|

| Uline | Shipping, packaging, and industrial supplies | Net-30 | Dun & Bradstreet, Experian |

| Grainger | Industrial supplies, MRO, and safety products | Net-30 | Dun & Bradstreet |

| Quill | Office supplies, furniture, and technology | Net-30 | Dun & Bradstreet |

| Creative Analytics | Digital marketing and business products | Net-30 | Dun & Bradstreet, Equifax, Experian, Creditsafe |

| Summa Office Supplies | General office and breakroom supplies | Net-30 | Dun & Bradstreet, Equifax |

Remember, this isn't an exhaustive list, but it’s a solid starting point for finding accounts that will actually help you. Always do your own due diligence before applying.

The real secret here is to open accounts with companies that sell things you actually need. Don't just buy junk to get a trade line. Making small, strategic purchases for your real business operations creates a legitimate and sustainable payment history, which is exactly what lenders want to see.

Once this payment data starts hitting your credit reports, you can begin to see a clear picture of your company's financial credibility. This is where specialized tools come in handy. For instance, funding advisors often use platforms with advanced AI-powered credit analysis features to instantly assess a business's fundability based on this early trade line data.

Your Strategy for Using These First Accounts

Getting approved is just the first step. How you manage these accounts is what truly builds your credit score. Be disciplined and intentional.

- Always Confirm Reporting First: This is non-negotiable. Before you apply, call the vendor’s credit department and ask them point-blank: "Do you report my company's payment history to Dun & Bradstreet, Experian Business, or Equifax Business?" If the answer is no, move on.

- Keep Your Purchases Small: You don’t need to rack up a huge bill. A simple purchase of $50 to $100 is usually more than enough to establish the account and generate a payment record. The dollar amount is far less important than the act of paying on time.

- Pay Early. Seriously. This is the best pro-tip I can give you for building business credit quickly. Paying a net-30 invoice 15-20 days early is viewed far more favorably than paying it on day 29. Early payments are a powerful way to boost your Dun & Bradstreet PAYDEX Score, a key metric that lenders scrutinize.

Stick to this game plan. Once you have three to five of these starter accounts reporting consistently early payments for a few months, you'll see a solid business credit profile begin to emerge. This is the foundation that will unlock larger and more significant funding opportunities down the road.

Using Financial Credit to Build Momentum

Alright, you've been diligently paying those vendor accounts for a few months. That’s the groundwork. Now it's time to start building the real structure of your business credit profile. We're moving from basic trade credit to financial credit, which is where things like business credit cards and small loans come into play.

Lenders and credit bureaus see these accounts differently. Managing a credit card or a small loan is a much stronger signal of your company's financial health than simply paying a supplier on time. This is the stage where you show the financial world you can handle real debt—both revolving and installment—which is key to unlocking much bigger funding opportunities down the road.

Making the Leap to Business Credit Cards

A business credit card is probably the single most powerful tool you can add to your arsenal right now. It gives you flexible spending power, sure, but the real benefit is the consistent, positive reporting. Every single month you pay on time, that good behavior gets reported to the bureaus, creating a steady pulse of activity on your file.

The trick is to apply for the right cards. You need to find issuers that report your activity specifically to the business credit bureaus. Many of the big players like Chase, American Express, and Capital One do this, but you have to check. Some will even approve you based on your EIN and the trade history you just built, without a hard pull on your personal credit.

How to Manage Your Business Card Strategically

Getting approved is just step one. How you use the card is what actually builds your score. Mess this up, and you can do more harm than good.

Here are the non-negotiables:

- Keep Your Utilization Low: This is a big one. Credit utilization is the percentage of your available credit you're actually using. As a rule of thumb, always try to keep your balance below 30% of your limit. Maxing out your card screams financial distress to lenders.

- Pay On Time, Every Time: Just like with your vendor accounts, this is paramount. No excuses. I always recommend setting up automatic payments for at least the minimum, just in case life gets in the way.

- Aim to Pay in Full: Paying on time is good, but paying the entire statement balance each month is the gold standard. It shows you have strong cash flow and saves you a ton in interest.

I see this mistake all the time: people treat a business credit card like a long-term loan. Don't. Use it for your day-to-day operational costs—things you know you can pay off at the end of the month. That’s how you build a rock-solid payment history without drowning your business in debt.

When Is It Time for a Small Business Loan?

Once your credit profile has some meat on its bones, you might be ready for a small business loan or a line of credit. These are tougher to get than a credit card, but getting one and paying it back responsibly is a massive vote of confidence in your business's favor.

The time to apply is when you have a specific, strategic use for the money—buying a key piece of equipment, stocking up on inventory for a big season, or funding a well-planned marketing push. Going after a loan without a clear plan is a recipe for disaster. A solid history of on-time payments on your vendor accounts and credit cards will dramatically improve your odds of approval and help you land a much better interest rate.

The funding struggle is real for new businesses. In 2023, while 43% of small businesses applied for loans, many were turned away simply because they hadn't built up any business credit. A strong profile is your best defense against this. A Paydex score over 80 is directly linked to much higher approval rates. This is where a tool like Score Machine becomes invaluable, as it can spot risks on your credit report in seconds and show you exactly what to fix to become fundable. If you want to dive deeper, you can find more detailed small business lending statistics to see the current landscape.

Keep Your Hands on the Wheel: Monitoring and Optimizing Your Credit Profile

Building business credit isn't something you can just set and forget. Once you've opened a few vendor accounts and maybe a business card, you've gotten the engine started. But now, you need to actually drive. Actively monitoring your credit profile is the only way to catch problems before they spiral, find opportunities to improve, and make sure all that hard work actually pays off when you need funding.

Think of it like this: you wouldn't run your business without glancing at your bank statements or P&L. Your business credit reports are every bit as vital. They're the official scorecard of your company's financial reliability, and you need to know exactly what they’re saying about you.

This ongoing cycle of checking in and tweaking your profile is what separates businesses that grow from those that stagnate. It’s the key to unlocking better and better financing down the road.

What to Look for on Your Business Credit Reports

When you first pull your reports from the big three—Dun & Bradstreet, Experian Business, and Equifax Business—it can be a bit overwhelming. You'll be staring at a wall of data, but what really matters to lenders boils down to a few key things.

Here's a quick checklist of where to focus your attention:

- Payment History: This is the big one. Are all your payments showing up as "on time" or "paid as agreed"? Hunt for any late payments, because even a single one can seriously drag down your score.

- Credit Utilization: For your credit cards and lines of credit, how much of your available limit are you using? High utilization, which is typically anything over 30%, can look like a cash flow problem to a lender.

- Public Records: Scan for any liens, judgments, or bankruptcies filed against your business. These are massive red flags and need to be dealt with immediately.

- Company Information: Is your business name, address, and EIN listed correctly? Simple typos or an old address can cause reporting mistakes and make it hard for bureaus to match accounts to your file.

If you find a mistake, don't just shrug it off. You have every right to dispute inaccuracies with the credit bureaus. A single error—like a payment you made on time that got reported as late—could be the difference between getting approved for that equipment loan or getting denied.

The real power in monitoring lies in a simple truth: what gets measured gets managed. Regularly reviewing your reports transforms you from a passive participant into an active manager of your business's financial reputation.

This is where technology can give you a massive leg up. Trying to decode a dense credit report and figure out your next move can be a real headache.

This report, for example, gives a clean, organized breakdown of a credit file, zeroing in on the key risk factors.

Tools like Score Machine use AI to do this heavy lifting instantly, turning that complex data into a clear, actionable plan for building credit the right way.

Using Technology to Streamline the Process

Let's be honest, manually pulling and trying to compare reports from three different bureaus is a tedious chore and it's easy to miss things. A platform like Score Machine automates this whole process, acting as an intelligent filter between you and the raw credit data. It doesn’t just show you a score; it tells you why your score is what it is and gives you the exact next steps to take.

For instance, its AI-powered analysis can instantly flag fundability risks you might otherwise overlook. It could point out a high-utilization account that's hurting you more than you realize or an old collection that needs to be resolved. This allows you to track your progress in real-time and make smart moves before you even think about applying for a loan.

How Funding Companies Use This to Get More Deals Done

This kind of deep analysis isn't just for business owners—it's a game-changer for funding companies and credit specialists, too. By integrating a tool like Score Machine, they can pre-qualify applicants with stunning accuracy. Instead of a simple "yes" or "no," they can generate a precise underwriting blueprint that shows a client the exact steps they need to take to become "bankable." This proactive approach enables funding companies to close more deals by turning previously unqualified applicants into fundable businesses. It creates a clear path to approval, which in turn increases the total funding volume they can facilitate.

For a deeper look at the specific features, you can explore the documentation for Score Machine's platform. This shifts the entire funding process from a transaction into a true partnership focused on getting to "yes."

How Funding Companies Increase Revenue with Score Machine

For anyone in the funding or credit repair business, our world revolves around a single, critical moment: turning a "no" into a "yes." Improving a client's fundability isn't just a side-service; it's the engine that drives your entire operation. But let's be honest—the traditional process of analyzing credit, spotting the deal-breakers, and guiding a client toward approval is a grind. It's manual, slow, and often frustrating for everyone involved.

This is where a tool like Score Machine changes the game. By automating the heavy lifting of credit analysis, your team can handle more clients without dropping the ball on quality. You stop being reactive, putting out fires, and start providing the proactive, strategic guidance that actually gets clients funded. For a funding company, this translates directly to increased funding volume and revenue.

Pre-Qualify with Precision and Reduce Denials

We've all been there. You spend hours, sometimes days, prepping an application, only to have it shot down by underwriting. It's a massive waste of time, it shakes your client's confidence, and it pushes your commission further down the road. Score Machine’s AI-powered underwriting blueprint lets you get ahead of this by pre-qualifying applicants with surgical accuracy right out of the gate.

Instead of just spitting out a generic score, the platform gives you a detailed fundability report that shows you exactly what a lender sees. It immediately flags the red flags—high utilization, old public records, thin credit history—and gives you the precise roadmap to make that client "bankable." This isn't guesswork; it's a proactive strategy that slashes denial rates. More approvals mean more successful deals and a healthier bottom line for your company.

You can see what needs to be fixed before you ever click "submit," saving yourself a ton of headaches and cementing your reputation as someone who delivers.

Turn Analysis into a New Revenue Stream

What happens to clients who get denied? Too often, they’re left in the dark, wondering what went wrong. That’s a huge missed opportunity. With Score Machine, you can take its clear, shareable, and compliant reports and offer them as a standalone service. This instantly creates a new way to make money and keeps potential clients in your ecosystem.

Instead of watching a lead walk away, you can offer them something of real value right then and there by selling them a personalized credit roadmap.

- Generate an initial blueprint that shows them exactly where they stand and the steps they need to take.

- Offer ongoing monitoring to help them track their progress each month as they implement your advice.

- Show them real, tangible improvements with every new report, which builds incredible trust and proves your worth.

This approach keeps clients engaged and turns leads you couldn't help today into successful funding deals tomorrow, maximizing the lifetime value of every single prospect.

The ability to show a client exactly where they stand and provide a step-by-step plan to get them funded is a powerful differentiator. It transforms your service from a simple transaction into a long-term, value-driven partnership.

Bridge the Massive Business Credit Gap

The demand for this kind of expert guidance is staggering. The global finance gap for small and medium-sized businesses is in the trillions, leaving a massive amount of untapped potential on the table. We know from data released by the State Small Business Credit Initiative (SSBCI) that targeted funding programs work. Between 2022 and 2023, just $536 million in program funds helped facilitate $1.8 billion in loans for over 3,000 small businesses. A solid credit profile is what unlocks that capital. You can dig into the numbers yourself in the official Treasury report.

For a funding company, helping a client build business credit is a critical skill. It involves establishing a Dun & Bradstreet profile, paying vendors ahead of schedule, and fine-tuning metrics like their debt-to-income ratio—all things Score Machine’s blueprint lays out clearly. By turning confusion into a clear plan, you help clients get the funding they thought was out of reach, directly boosting the number and size of deals your company can close.

You can see a full breakdown of how Score Machine’s AI-driven analysis works and how it makes this possible. At the end of the day, when you can provide that level of clarity, you close more deals, grow your revenue, and become the go-to partner your clients can't succeed without.

Common Questions About Building Business Credit

As you dive into the world of business credit, you're bound to have questions. It's a landscape with a lot of moving parts, and getting clear answers from the start can save you a ton of headaches and missteps down the road.

Let's tackle some of the most common questions I hear from entrepreneurs every day.

How Long Does It Take to Build Good Business Credit?

This is usually the first thing everyone wants to know. The honest answer? It’s a marathon, not a sprint. While you can start seeing new accounts pop up on your credit reports within 30 to 90 days after opening them, building a truly robust, fundable profile takes patience and consistency.

Think about it in phases. In the first six months of making steady, on-time payments, you’ll establish a foundational score. But to build a profile that lenders and major suppliers truly respect, you should realistically plan for a 6 to 12-month journey of disciplined credit management.

The single biggest way to speed things up is to pay your vendors and creditors early. An early payment on a net-30 account sends a powerful message to the credit bureaus and can give your PAYDEX score a much bigger boost than just paying on time.

Does My Personal Credit Affect My Business Credit?

On paper, your personal and business credit are entirely separate entities. But in the real world, especially when your business is new, the line between them is often blurry.

Many lenders will check your personal credit to get a sense of your financial reliability, particularly if your business doesn't have much of a credit history yet. It's also very common to be asked for a personal guarantee (PG) on your first few business credit cards or loans. A PG means you're personally on the hook for the debt if the business can't pay.

The long-term goal of building business credit is to break this connection. A strong, independent business profile lets your company stand on its own two feet, eventually securing funding without needing your personal score or a PG.

What Is a Duns Number and Do I Really Need One?

A DUNS number is a unique nine-digit ID for your business assigned by Dun & Bradstreet, one of the major business credit bureaus. You can think of it as a Social Security Number for your business's credit file with them.

And to answer the second part of the question: yes, you absolutely need one.

Without a DUNS number, Dun & Bradstreet can't even start a credit file for your business. Since many suppliers, government agencies, and lenders rely heavily on D&B for credit checks, not having one makes you invisible. The good news is that getting a DUNS number is a free and non-negotiable first step.

Ready to stop guessing and start building? Score Machine provides the AI-powered credit intelligence you need to turn complex credit data into a clear, actionable plan. Elevate your score and unlock funding with confidence. Learn more and get started at https://thescoremachine.com.