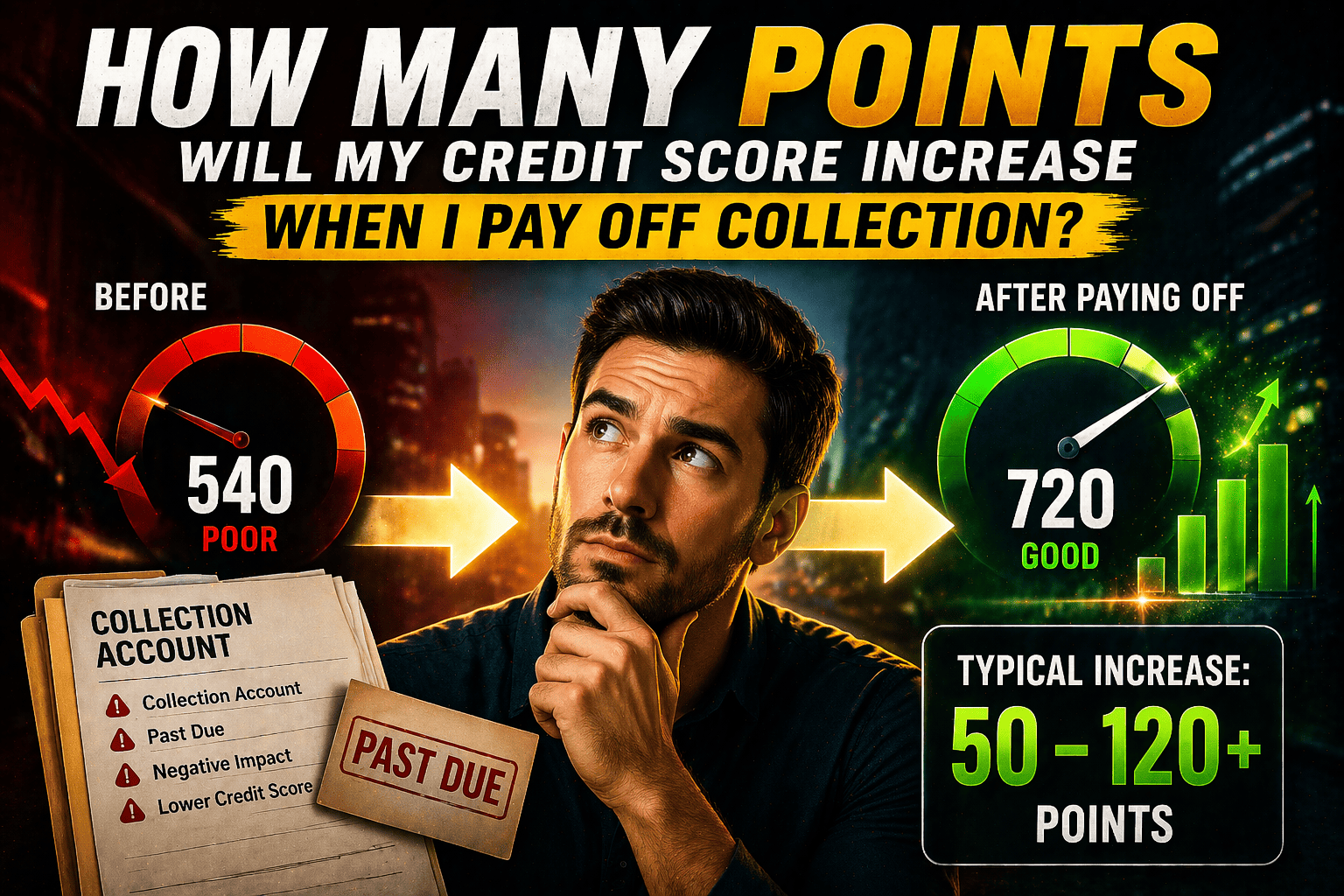

The most honest—and admittedly, frustrating—answer to how many points your credit score will jump after paying a collection is this: it completely depends on your unique credit file. There’s no magic number or universal increase because every situation is different. Factors like the specific credit scoring model, how old the debt is, and the rest of your credit history all play a huge role in the final outcome.

The Real Answer to Your Credit Score Question

It's common to hope for a big 50-point leap the second you pay off that nagging collection, but the reality is usually a lot more nuanced. While paying off a collection is always a good move for your financial health, its direct impact on your score isn't a sure thing.

Think of it less like flipping a switch for an instant boost and more like planting a seed. You’ve done the right thing, but it will take time for that positive action to grow and reflect on your report. The single biggest variable determining how much—or how little—growth you see is the credit scoring model a lender uses to look at your file.

Why Scoring Models Matter Most

The way paid collections are treated varies wildly from one scoring model to the next, and this is where most of the confusion comes from.

Newer models like the latest versions of FICO® and VantageScore® are designed to completely ignore paid collection accounts. That's fantastic news. If a lender is using one of these up-to-date models, paying off a collection could give you a very significant score increase. You can find a deeper dive into this topic in Experian’s analysis of scoring models and collections.

The crucial takeaway is this: An older scoring model might see your payment and barely budge your score, while a newer model could reward you significantly. Knowing which version is being used is key.

This is where guesswork can really hurt you. Instead of just paying and hoping for the best, you need a strategy backed by data. That’s what makes a tool like The Score Machine so powerful. Its AI-driven analysis cuts through the noise, showing you exactly how to tackle the issues on your specific credit file for the biggest impact. It essentially gives you a personalized blueprint for credit improvement.

For funding companies, this kind of clarity is a game-changer. By using The Score Machine to provide applicants a clear, actionable plan, you can dramatically increase funding approvals. Rather than turning away promising but not-quite-there applicants, you can show them a clear path to becoming fundable. This strengthens your client pipeline, increases your deal flow, and ultimately drives business forward.

Why Different Credit Scoring Models Give Different Results

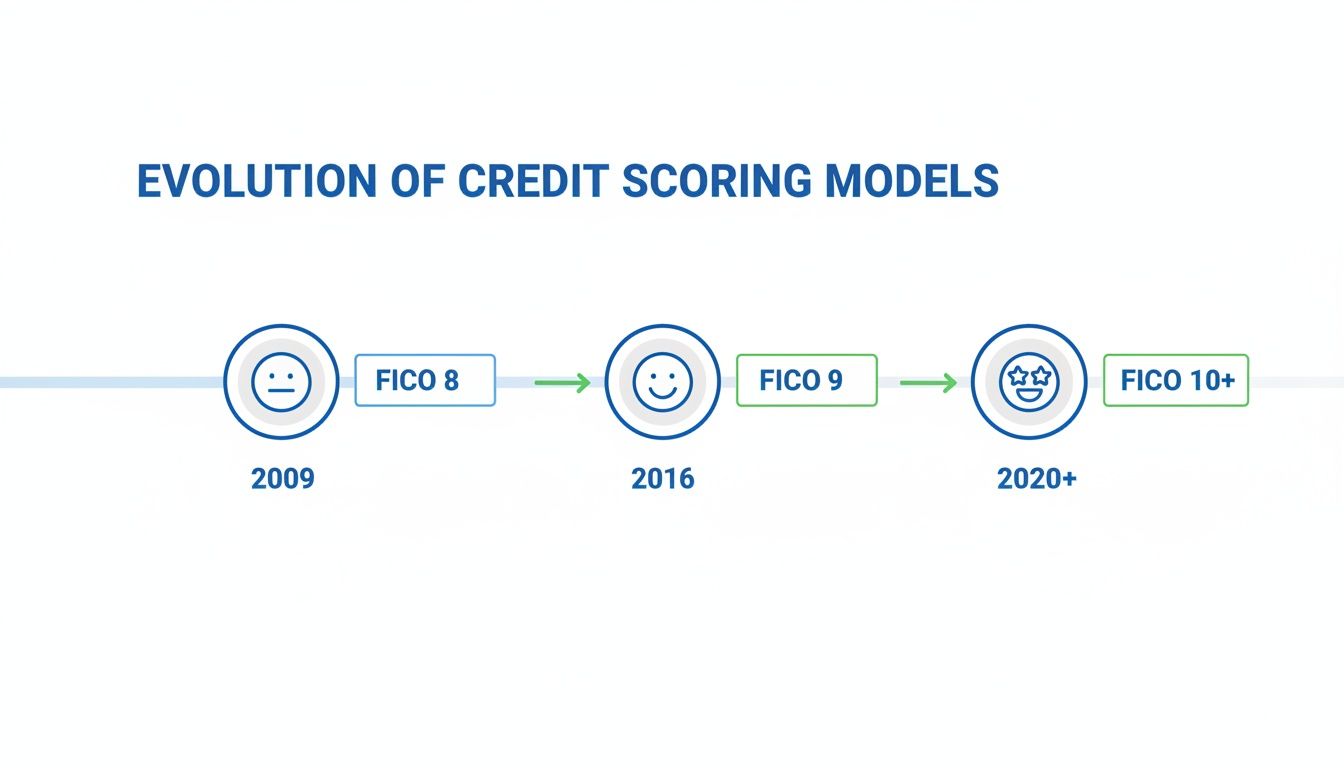

Ever wonder why your credit score seems to change depending on who's looking at it? Think of it like a smartphone. You might have the latest model, but your friend could be using one from 2009. Both make calls, but their operating systems are from different eras. The new phone has features and apps the old one can’t even run.

Credit scoring models work the same way, and it’s the biggest reason for the confusion around paying off collections.

There isn’t just one "credit score." The two big names are FICO and VantageScore, but both have rolled out many different versions over the years. Lenders don't all upgrade at the same time, which means the score a car dealership pulls could be completely different from the one a credit card company sees.

The Old Guard vs. The Newcomers

The most common older model you’ll run into is FICO 8. For a long time, it was the gold standard for most lenders. The problem? FICO 8 has a very black-and-white view of collections: if you had one, it's a sign of risk. That’s it. Whether you paid it off or not, the negative mark stays and drags your score down.

This is where the frustration kicks in. You might pay off a $500 collection account, check your FICO 8 score, and see a tiny bump—or worse, no increase at all. It’s a reality that blindsides a lot of people trying to do the right thing.

Thankfully, newer scoring models have gotten smarter. They’re designed to look at your current financial habits, not just mistakes from the past.

- FICO 9 & FICO 10: These versions completely ignore collection accounts once they’ve been paid. If a lender is using one of these, paying off that same $500 collection could give your score a serious boost because the scoring formula essentially stops seeing it.

- VantageScore 3.0 & 4.0: These popular scores from FICO's main competitor do the same thing. Once a collection account has a zero balance, it no longer hurts your score.

The bottom line is simple: older models punish you for a past mistake, while newer models reward you for fixing it. Your score’s reaction depends entirely on which "operating system" a lender is running.

How This Affects Funding Companies and Your Approval Odds

This isn't just a quirky detail; it has huge, real-world consequences, especially for funding companies. A company could easily deny an applicant because an older scoring model is punishing them for a collection they’ve already paid. But if you look at that same person through the lens of a modern score, they might be a perfect candidate.

This is where sophisticated analysis tools come into play. Instead of just looking at one, potentially outdated score, platforms like The Score Machine can dig into the entire credit file. For a funding company, using The Score Machine means you can spot applicants who are actually "fundable" based on newer models, even if their old score looks bad. This intelligent analysis lets you approve more loans your competitors would have turned away, directly increasing funding.

Using The Score Machine helps turn borderline denials into approvals. It gives you the data to back up a funding decision, showing an applicant’s true creditworthiness. This doesn’t just increase your funding volume—it builds a loyal client base that sees you as a true partner. You can check your own credit score with its AI to get a clear roadmap for resolving these kinds of issues at http://thescoremachine.com.

The Lifecycle of a Collection on Your Credit Report

Think of a collection account on your credit report not as a permanent scar, but as a deep scratch that gradually heals. Its impact is sharpest and most damaging the moment it first appears. That initial drop in your score is the big one—it's a bright red flag for lenders, showing that a debt went seriously delinquent.

But the sting of a collection doesn't last forever. As the account gets older, its negative pull on your credit score starts to weaken. With each passing year, it matters a little less in the scoring calculations, even if you haven't paid it. This slow fade continues for its entire seven-year lifespan on your report.

From Unpaid to Paid

So, what happens when you finally pay it off? Once you make the payment, the collection agency has to report it to the credit bureaus. You can generally expect to see the account status flip from "unpaid" to "paid" within about 30 to 45 days.

This is a huge step in the right direction, but it's crucial to set the right expectations. Seeing that "paid" status pop up doesn't always mean your score will instantly skyrocket, especially if your lender is using an older scoring model.

Paying off a collection turns an active, ongoing problem into a resolved issue from your financial past. For lenders, that's a powerful sign of responsibility. It shows you're making an effort to handle your obligations, which can be just as meaningful as the number on your score.

This evolution in credit scoring is important. Newer models are built to recognize and reward you for taking positive steps like paying off old debts.

The takeaway here is that modern scores like FICO 9 and 10 are designed to ignore paid collections entirely, while older versions like FICO 8 often keep penalizing you for them.

What This Means for Funding Companies

If you're in the business of funding, understanding this lifecycle is a game-changer for boosting approval rates. A client with an unpaid collection might look like an automatic "no" based on their score alone. But when you dig into the details of their credit file, a much smarter path often reveals itself.

Tools like The Score Machine allow you to see past that initial negative item. Its AI can model exactly how paying off a specific collection will affect the score, pinpointing which applicants could become "fundable" with just a bit of guidance. This turns a simple denial into a valuable, long-term partnership.

Instead of just rejecting someone, you can give them a clear, data-backed plan. Imagine showing a client how settling a two-year-old collection could boost their score enough to qualify them for funding in just a couple of months. By providing this guidance, you increase the chances of funding that client later, directly boosting your company's revenue.

This strategy doesn't just increase your funded loans; it builds incredible loyalty. When you need to understand your own credit situation and find solutions, you can get an AI-powered analysis at http://thescoremachine.com.

Ultimately, while the exact point increase can be unpredictable, the act of paying the collection is always a positive signal to the credit world. While older models might not give you an immediate boost, getting that account marked "paid" within 30 to 45 days is a critical move. As you can learn more about how paying debt collectors helps your credit at J.G. Wentworth, it’s clear that a "paid" status builds the foundation for better credit health and future fundability.

Your Game Plan for Tackling Collection Accounts

It's one thing to know that paying off a collection is the right move, but it's another thing entirely to do it in a way that actually helps your credit score. If you just mail a check without a plan, you could be leaving a lot of potential points behind. To get the biggest score boost and make sure your effort pays off, you need to be strategic.

Before a single dollar leaves your bank account, your first move is always to verify the debt. Is it really yours? Is the amount correct? Does this specific agency even have the legal right to collect it? This isn't just about dodging a scam; mistakes are surprisingly common, and you definitely don't want to pay for an error that isn't yours.

Once you've confirmed the debt is legitimate, the real strategy kicks in. Your objective isn't just to mark the debt as "paid"—it's to get the entire negative account wiped from your credit report for good. This is where a pay-for-delete agreement becomes your most powerful tool.

The Magic of a Pay-For-Delete Agreement

A pay-for-delete is exactly what it sounds like: you agree to pay the debt (either in full or a negotiated settlement), and in exchange, the collection agency promises to completely remove the account from your reports with Experian, Equifax, and TransUnion. For your credit score, this is the absolute best-case scenario.

So, why is it so effective?

- It Erases the Past: Instead of the account just being updated to "paid," which still leaves a negative mark for seven years, it vanishes. It's like it never happened.

- It Delivers Maximum Points: This is the only guaranteed way to stop the collection from hurting your score across all scoring models, including older ones used by mortgage lenders.

- It Gives You a Clean Slate: The negative account is gone, which means it can't be seen by loan officers or the automated systems that approve or deny applications.

A word of warning: Always, always get a pay-for-delete agreement in writing before you send any money. A verbal promise over the phone is worthless. If an agency refuses to put the deal on paper, be extremely cautious—they may have no intention of honoring it.

For lenders and funding advisors, guiding a client to secure a pay-for-delete can be the difference between a denial and an approval. When the collection is removed, the applicant's credit profile instantly looks stronger, making them a much better candidate for funding.

Building Your Action Plan

What if you have more than one collection? You need to be smart about which one you tackle first. Credit scoring algorithms don't treat all collections equally. As a general rule, newer collections do far more damage than older ones.

Here’s a simple framework for deciding where to start:

- Prioritize New and Large Debts: Go after the collection accounts that hit your report most recently. These carry the most negative weight and are dragging your score down the most.

- Negotiate Everything: Even if you can afford to pay in full, always start by asking for a pay-for-delete. You have nothing to lose by asking.

- Keep Meticulous Records: Document everything. Save every letter, email, and payment confirmation, and take notes on every phone call.

This can feel like a lot to juggle, but this is where modern tools can give you a serious edge. Instead of guessing which account to pay off for the biggest impact, you can use a platform that gives you a clear, data-driven roadmap.

An AI-powered platform like The Score Machine can analyze your entire credit file and simulate the outcome of different actions. It can pinpoint exactly which collection, if paid, will give you the most significant score increase. It takes the guesswork out of the equation and hands you a clear, step-by-step plan. To learn more powerful credit strategies, check out the other guides on The Score Machine blog. With an intelligent system on your side, you can handle your collections with the confidence of a seasoned expert.

How Lenders See Paid vs. Unpaid Collections

We get so caught up in the three-digit number that it's easy to forget what's behind it. When you apply for a big loan—think a mortgage or business financing—a human underwriter looks at your entire financial story, not just your score. And in that story, an unpaid collection account is a huge red flag.

To a lender, an open collection is a sign of unresolved financial trouble and current risk. It makes them question whether you can handle your debts. So, even if an older scoring model doesn't give you a massive point boost for paying it off, changing that status to 'paid in full' tells a much better story.

That one change proves you're responsible. It shows you’re committed to making things right, which is a massive boost to your "fundability"—how good you look as a borrower. This change in perception is often worth far more than a few extra credit score points.

The Story Your Credit Report Tells

Let's imagine two people apply for a loan. They have the exact same credit score. But one person has an unpaid collection for $800 from two years ago. The other had the same collection but paid it off last month. Who do you think the lender is going to see as a safer bet?

It’s a no-brainer. The paid collection is a closed chapter, a problem that’s been fixed. The unpaid one is still an active risk.

This is exactly why focusing only on "how many points will my credit score increase when I pay off collections" is missing the bigger picture. The real win is changing your story from one of risk to one of reliability.

The Growing Incentive to Pay Off Collections

The financial world is finally starting to catch on. Collection accounts are a reality for millions of Americans, and credit scoring companies are adapting. As more lenders switch to newer models like FICO® Score 10 and VantageScore 4.0—which completely ignore paid collections—the incentive to clear these debts is stronger than ever. For more on this, check out the CFPB’s recommendations on handling collections at Shepherd Outsourcing Services.

A 'paid' collection is more than just a line item on a report; it's proof to a lender that you are a borrower who honors their commitments, making you a more attractive candidate for funding.

If you're a funding company, understanding this is the key to getting more deals done. Instead of an automatic "no" for an applicant with a collection, you can show them how to resolve it. That simple step can turn a denial into a future approval and build a stronger client pipeline.

This is exactly what tools like The Score Machine are designed for. Its AI can scan a credit report and show a client precisely how paying off a collection improves their fundability, not just their score. It creates a clear, actionable roadmap that turns a borderline applicant into a solid one. You can explore the AI-powered features of Score Machine that make this possible. By using a system like this, funding companies can boost their loan volume by spotting and guiding applicants who are just one step away from getting approved.

Turn Today's Denials Into Tomorrow's Deals

For any funding company, a denied application feels like a dead end. It’s a missed opportunity, especially when the applicant is right on the edge of approval. Often, the culprit is something like a nagging collection account that flags them as too risky. Traditionally, that’s where the conversation stops. But what if you could change that?

What if, instead of just a rejection, you could offer a clear, actionable roadmap to approval? This is where a credit intelligence platform completely changes the game. You stop being just a gatekeeper and become a crucial partner in your applicant's financial journey.

Imagine an applicant gets denied because of a collection. Instead of sending them away empty-handed, you give them a precise plan. A system like The Score Machine can dive into their credit report and show them exactly how paying off that specific collection will boost their score and make them a great candidate for funding.

From Rejected Applicant to Loyal Customer

This strategy does more than just rescue one application; it builds a pipeline of future business. By giving someone a real solution, you're building incredible trust. That applicant, now equipped with a clear plan, is almost certain to come back to you when they’re ready to be funded.

This has a direct impact on your bottom line:

- Boost Your Conversion Rate: You'll turn a much higher percentage of initial applicants into funded deals over the long run.

- Build a Reliable Pipeline: Stop waiting for perfect leads to walk in the door. You can start creating them from the pool you already have.

- Strengthen Your Reputation: You'll be known as the company that helps people get ahead, not the one that just says "no."

Think about it: instead of losing that borderline applicant to a competitor, you're giving them the tools they need to succeed and ensuring they walk right back through your door. You’re turning a single transaction into a long-term, profitable relationship.

The Power of a Data-Backed Plan

The real magic here is clarity. Vague advice like "work on your credit" doesn't help anyone. But showing a client that clearing a $750 medical collection could get them approved in 90 days? That’s specific, powerful, and motivating.

An AI-driven platform takes all the guesswork out of the equation. It runs simulations to show how specific actions will impact a credit profile, giving both you and your client total confidence in the path forward. This level of insight helps you make smarter decisions about your pipeline and ultimately fund more loans.

You can use this kind of analysis to see how different scenarios will play out for your applicants. A funding company can use The Score Machine to convert more leads into funded deals, directly increasing revenue. It's a proactive approach that helps your clients while strengthening your business with a steady flow of fundable applicants. You're no longer turning people away; you're empowering them with a plan from The Score Machine, giving them the tools to check their credit with AI and understand exactly how to clear their funding roadblocks.

Frequently Asked Questions About Collections and Credit

Let's cut through the confusion. When you're dealing with collections, you need straight answers, not financial jargon. Here are some of the most common questions we see, broken down into plain English to help you make the right moves.

Is It Better to Settle a Collection or Pay It in Full?

Paying in full is always the gold standard for your credit report. When you clear the entire balance, the account gets updated to "Paid in Full." Lenders see this and know you met your obligation, even though it was late.

Settling for less than you owe marks the account as "Settled." This tells future lenders you didn't repay the full amount. While it's a huge step up from an unpaid collection, it doesn't look quite as good as a "Paid in Full" status. If you're gearing up for a big loan like a mortgage, paying in full is definitely the way to go.

Does a Pay-For-Delete Agreement Really Work?

Absolutely. A pay-for-delete agreement, when you can get one, is the best possible outcome. If the collector agrees and follows through, the entire negative account vanishes from your credit report like it was never there. This can give your score a serious boost.

But here's the catch: it's a negotiation, not a guarantee. You have to get the collector to agree to it. Crucially, you must get the entire agreement in writing before a single dollar leaves your bank account. That written proof is your only protection to make sure they hold up their end of the bargain.

Should I Pay a Collection That Is Almost Seven Years Old?

Probably not. Most negative marks, including collections, are legally required to fall off your credit report after seven years from the date you first missed a payment.

If a collection is already six and a half years old, paying it might not be worth it. Worse, in some states, making a payment can restart the clock on the statute of limitations for being sued over the debt. When an old collection is just a few months from disappearing on its own, the smartest move is often to just let it fade away naturally.

How Can I Check My Credit and Get an AI Analysis?

To really see what's going on with your credit, you need more than just a score. An AI-powered credit intelligence platform can dig into your entire file, pinpointing the exact problems and mapping out the fastest way to fix them.

This is a game-changer for funding companies. Instead of just denying a borderline applicant, you can give them an AI-driven blueprint from The Score Machine. This turns a "no" into a "not yet," creating a clear path for them to get approved down the line. You're not just increasing funding volume; you're building a loyal pipeline of clients who see you as a partner in their success.

Ready to stop guessing and start improving? Visit The Score Machine at http://thescoremachine.com to check your credit score with AI, understand exactly what’s holding you back, and get a clear, actionable plan to solve it.