Ali Badi, CTO / Credit Risk Strategist at Score Machine — 12+ years in fintech and credit analysis Reviewed by: TheScoreMachine Editorial Team — Reviewed against FCRA, CFPB, and FICO guidance Last updated: June 2026 Reading time: ~12 min

Written by Ali Badi, CTO / Credit Risk Strategist at Score Machine — 12+ years in fintech and credit analysis. Reviewed by the TheScoreMachine Editorial Team against FCRA, CFPB, and FICO guidance. Last updated June 2026.

This article is for educational purposes only and does not constitute financial, legal, or credit advice. Individual outcomes vary. Consult a licensed professional for guidance specific to your situation.

Most derogatory marks stick around for seven years from the date you first missed a payment. That's the rule laid out by the Fair Credit Reporting Act (FCRA), with one notable exception: Chapter 7 bankruptcy, which stays for 10 years.

But there's more to this than just knowing the numbers. The clock starts from a specific date that trips most people up. The score damage is not equal across mark types or score tiers. And your options for getting off the 7-year waiting list early are real — if you use them right.

Here's a complete, honest breakdown.

Table of Contents

- Derogatory mark timelines at a glance

- How many points does each mark drop your score?

- The 7-year clock — when does it actually start?

- The real-world example: one $500 medical bill

- Understanding each type of derogatory mark

- Bankruptcy and the 10-year exception

- How derogatory marks affect your mortgage eligibility

- FICO Score 9 and VantageScore 4.0 — the exceptions

- Proactive ways to remove derogatory marks early

- How to rebuild your credit while you wait

- FAQ

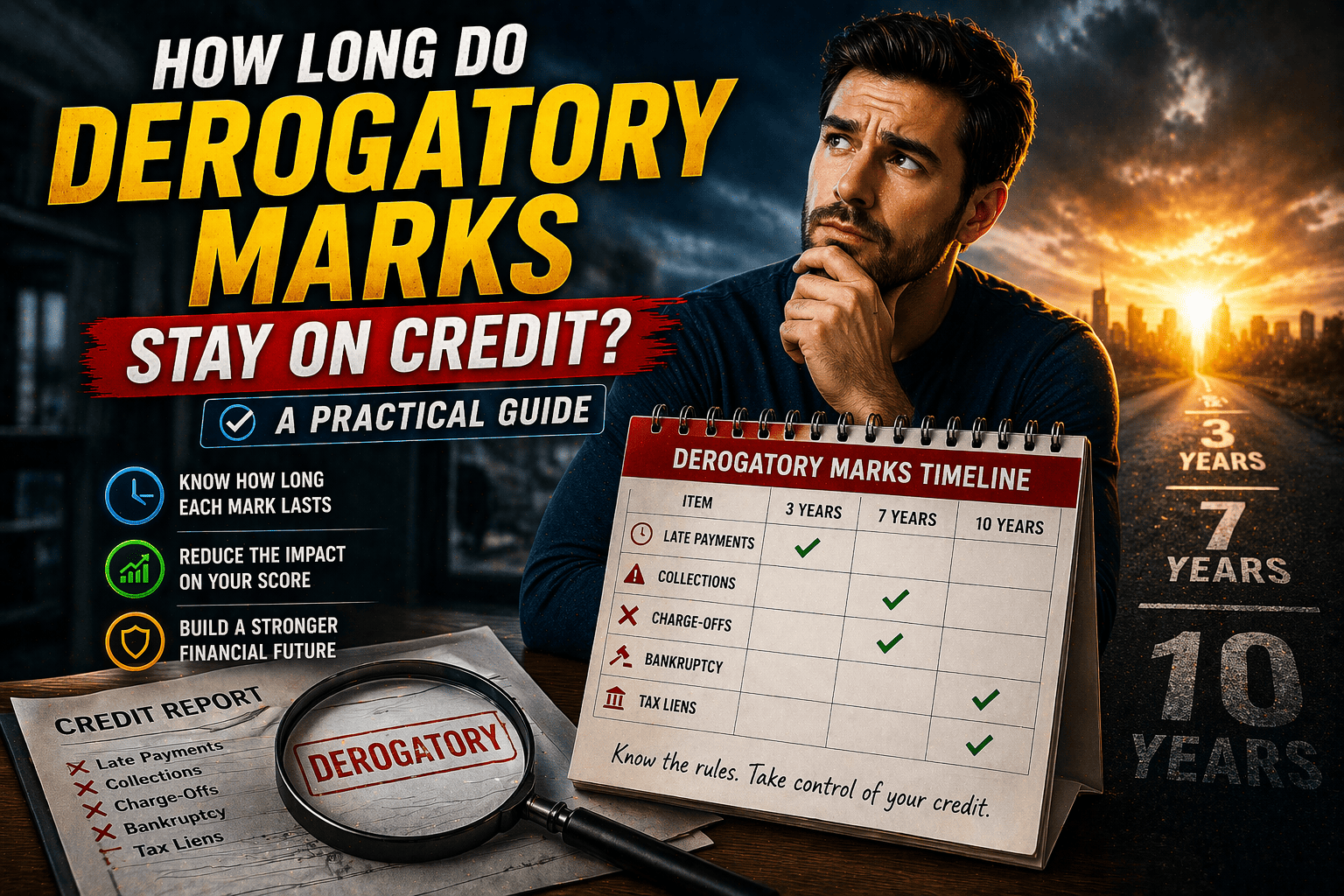

Derogatory Mark Timelines at a Glance {#timelines}

Quick answer: Most derogatory marks stay for 7 years from the original missed payment date. Chapter 7 bankruptcy is the only type that stays for 10 years.

| Derogatory Mark Type | Time on Report | Clock Starts From | Key Impact |

|---|---|---|---|

| Late payments (30/60/90+ days) | 7 years | Date first payment was missed | Damages payment history — 35% of FICO score |

| Collections | 7 years | Original missed payment date | Major red flag; signals creditor gave up |

| Charge-offs | 7 years | Original missed payment date | Shows original creditor wrote debt off as loss |

| Repossessions | 7 years | Original missed payment date | Affects score + auto loan eligibility |

| Foreclosures | 7 years | Date of first missed mortgage payment | Severely limits future mortgage eligibility |

| Debt settlement | 7 years | Original delinquency or settlement date | Shows partial repayment — still negative |

| Judgments | 7 years | Filing date | Public record; lenders find these in deeper searches |

| Chapter 13 bankruptcy | 7 years | Filing date | Court-approved repayment plan |

| Chapter 7 bankruptcy | 10 years | Filing date | Most severe — full liquidation of assets |

Source: Fair Credit Reporting Act (FCRA) Section 605; Equifax, Experian, and TransUnion reporting guidelines.

The key thing most guides miss: The clock starts from the date you first missed a payment — not when the account was charged off, not when it was sold to a collector, and not when you made your last payment. That distinction can mean the difference between thinking you have four more years to wait and realizing you only have two.

For more detail on late payment timelines specifically, see our guide on how long late payments stay on your credit report.

How Many Points Does Each Mark Drop Your Score? {#points-dropped}

Quick answer: The higher your starting score, the harder the fall. A bankruptcy can drop a score above 780 by 150–240 points. A single 30-day late payment on the same score can cost 90–110 points.

| Derogatory Mark | Excellent (780+) | Good (670–739) | Fair (580–669) |

|---|---|---|---|

| 30-day late payment | −90 to −110 pts | −60 to −80 pts | −17 to −37 pts |

| 60-day late payment | −105 to −125 pts | −70 to −100 pts | −27 to −47 pts |

| 90-day late payment | −115 to −135 pts | −80 to −110 pts | −27 to −47 pts |

| Collection / charge-off | −100 to −125 pts | −85 to −105 pts | −40 to −70 pts |

| Repossession | −100 to −125 pts | −85 to −105 pts | −40 to −65 pts |

| Foreclosure | −105 to −130 pts | −85 to −110 pts | −50 to −75 pts |

| Chapter 13 bankruptcy | −130 to −150 pts | −95 to −115 pts | −55 to −80 pts |

| Chapter 7 bankruptcy | −150 to −240 pts | −130 to −150 pts | −80 to −130 pts |

Estimates based on published FICO research and industry data via myFICO.com. Exact impact depends on your full credit profile.

Why higher scores fall harder: Scoring models measure the deviation from your established pattern. A borrower with a spotless 10-year history suddenly missing a payment is a statistically significant anomaly. A borrower who has already missed multiple payments shows much less statistical change from one more. This is why two people with similar current scores can see very different drops from the same event.

The good news is that the damage fades — especially in the first two years of clean payment behavior. The mark stays for 7 years, but the active score drag is most severe in the first 6 to 24 months.

For a comprehensive look at how late payment damage specifically fades over time, our guide on how late payments affect your credit score covers the year-by-year recovery data.

The 7-Year Clock — When Does It Actually Start? {#seven-year-clock}

Quick answer: The 7-year clock starts from the date of first delinquency — the date you first missed the payment that started the whole negative chain. Not the charge-off date. Not the collection date. Not the last payment date.

This is the single most important thing to understand about derogatory marks. Getting it wrong can make you think a negative item is going to haunt your report for years longer than it actually will — or it can leave you blindsided when something you thought was close to falling off gets updated and appears to reset.

Here's how it plays out in practice. You miss a credit card payment on January 15, 2020. That is the date of first delinquency. In July 2020, the original creditor charges off the debt. In August 2020, they sell it to a collection agency, and a new collection account appears on your report. None of those events move the clock. The entire negative history from that single bill — both the charge-off and the collection — falls off your credit report in January 2027. Seven years from that first missed payment in January 2020.

Three common mistakes people make:

Paying the debt restarts the clock. This is false. Paying a collection or charge-off changes the status to "paid" and may help with newer scoring models, but the 7-year reporting period is unchanged. The original delinquency date is fixed by law.

Each collection from the same debt adds its own 7-year timeline. Also false. When a debt is sold to a third-party collector, the new collection account must follow the same 7-year clock as the original debt. If a collector tries to report a more recent date to extend how long the mark appears, that is illegal re-aging.

Disputing restarts the clock. No. Filing a dispute pauses the mark temporarily while the bureau investigates, but the 7-year clock continues running. Successfully disputing an inaccurate item removes it entirely — it does not give the creditor a fresh timeline.

The Real-World Example: One $500 Medical Bill {#real-example}

Quick answer: One missed payment can generate two separate derogatory marks from the same debt — and neither one resets the timeline no matter what happens next.

Here's a scenario that plays out for millions of Americans every year:

- January 2020: A $500 medical bill gets lost during an insurance dispute. You miss the payment. This is the date of first delinquency — the only date that matters for the 7-year clock.

- July 2020: The hospital charges off the debt. A charge-off appears on your credit report. Your 7-year clock is still running from January 2020.

- August 2020: The hospital sells your debt to a collection agency. A brand-new collection account appears on your report. You now have two marks from one bill.

- October 2020: You pay the collection agency in full. Both accounts update to show zero balance. Your 7-year clock is still running from January 2020.

- January 2027: Both the charge-off and the collection account automatically fall off your report. Seven years from that first missed payment.

No matter when the charge-off happened, when the collection appeared, or when you paid — the end date was always January 2027.

One thing to watch for: some debt collectors illegally attempt to "re-age" a delinquency by reporting a more recent date to extend how long the mark shows up. If you notice that the dates on your credit report have shifted from what your own records show, that is a Fair Credit Reporting Act violation. Dispute it with the bureau immediately and file a complaint with the CFPB.

Understanding Each Type of Derogatory Mark {#mark-types}

Late Payments: The Most Common One

A late payment shows up when you are at least 30 days past due. Creditors report late payments in escalating increments — 30, 60, 90, and 120+ days — and each escalation causes additional score damage beyond the initial hit.

This is the most common derogatory mark, and payment history makes up 35% of your FICO score, making it the single most impactful factor in your credit profile. One 30-day late payment on an otherwise clean file can knock a good score down significantly. The silver lining is that it is also the mark most likely to be removed via a goodwill letter, particularly if it was a one-time incident with a long history of on-time payments before it.

For a deep dive on late payment removal strategies, see our guide on how to remove late payments from your credit report.

Collections and Charge-Offs: The Escalation Point

When an account reaches 120 to 180 days past due, a creditor typically takes one or both of these steps:

Charge-off: The original creditor writes your debt off as an accounting loss. This is not debt forgiveness — you still owe every dollar. A charge-off signals to any future lender that you failed to repay the original creditor, and it is a severe mark. It stays on your report for seven years from the original delinquency date.

Collections: After charging off the debt, the original creditor often sells it to a third-party collection agency. That agency now owns your debt and reports a separate collection account on your credit report. The result: one unpaid bill creates two separate derogatory marks. Both follow the same 7-year timeline, starting from your original missed payment — not from when the collection appeared.

A common myth: paying off a collection makes it vanish from your report. Paying updates the status to "Paid Collection" and may help with newer scoring models, but the mark itself stays for the full seven years. The only way to remove it early is a successful dispute for inaccuracies or a pay-for-delete negotiation, which we cover below.

For more on how late marks on closed accounts work specifically, see our guide on late payments on closed accounts and your credit score.

Repossessions and Foreclosures: Asset Seizures

Both of these marks are tied to secured loans — debt backed by physical collateral.

A repossession happens when you default on an auto loan and the lender takes the vehicle. A foreclosure happens when you stop making mortgage payments and the lender seizes your home. Both stay on your report for seven years from the date of the first missed payment that triggered the process — not from the date the asset was actually taken.

Beyond the credit damage, both create loan eligibility problems that go beyond what the score number alone shows. Mortgage underwriters and auto lenders flag these marks specifically because they show you did not repay a secured obligation, which is treated as a higher-risk signal than unsecured debt defaults.

Judgments: Public Record Problems

A judgment is a court record showing a lender or collector sued you for non-payment and won. While recent changes to credit bureau data policies have made civil judgments less common on standard credit reports from the three major bureaus, lenders who run deeper public records searches — which is standard practice for mortgage applications — will find them. A judgment can stay on your report for seven years from the filing date.

Bankruptcy and the 10-Year Exception {#bankruptcy}

Quick answer: Chapter 7 bankruptcy stays for 10 years from the filing date. Chapter 13 follows the standard 7-year rule. Both cause severe score damage — but recovery is possible faster than most people expect.

Chapter 7 vs Chapter 13: What the Difference Means for Your Credit

Chapter 7 is liquidation bankruptcy. Most of your unsecured debts get discharged — wiped out — in exchange for selling non-exempt assets. Because it completely eliminates debt without full repayment, it is the harsher option in the eyes of lenders. It stays on your credit report for 10 years from the filing date.

Chapter 13 is reorganization bankruptcy. You keep your assets and commit to a 3 to 5-year repayment plan. Because you are repaying at least part of what you owe, it is treated as less severe. It falls off your credit report seven years from the filing date.

The immediate score impact of a Chapter 7 bankruptcy is typically 150 to 240 points for someone starting above 780. The impact is smaller for those already in lower score tiers because the deviation from the pattern is less dramatic. Either way, the hit is significant and immediate.

Recovery After Bankruptcy

Despite the 10-year mark, the path back starts on day one. Two years of consistent, positive payment behavior after a bankruptcy discharge can move your score back into the 620 to 680 range for many borrowers. The specific timeline depends on what else is on your file, but recovery is realistic — and it is possible to qualify for certain types of credit well before the 10-year mark falls off.

The tools that work: secured credit cards (where your deposit becomes your credit limit), credit-builder loans from credit unions, and becoming an authorized user on a family member's long-standing account. These build new positive payment history that steadily dilutes the weight of the bankruptcy in your score.

How Derogatory Marks Affect Your Mortgage Eligibility {#mortgage-waiting}

Quick answer: Every major derogatory event comes with a mandatory waiting period before mortgage lenders will approve you. These periods vary by loan type and by the specific event.

This is one of the most practical questions readers have — and one that almost no credit guide answers directly. Here are the standard waiting periods based on Fannie Mae Selling Guide guidelines (B3-5.3-07) and FHA/VA requirements. Individual lenders may have stricter policies.

| Derogatory Event | Conventional Loan | FHA Loan | VA Loan |

|---|---|---|---|

| Chapter 7 bankruptcy | 4 years from discharge | 2 years from discharge | 2 years from discharge |

| Chapter 13 bankruptcy (discharged) | 2 years from discharge | 1 year from start of repayment | 1 year from start of repayment |

| Chapter 13 bankruptcy (dismissed) | 4 years from dismissal | 2 years from dismissal | 2 years from dismissal |

| Foreclosure | 7 years from completion | 3 years from completion | 2 years from completion |

| Deed-in-lieu / short sale | 4 years from completion | 3 years from completion | 2 years from completion |

| Multiple bankruptcies (2+) | 5 years from most recent discharge | Standard 2-year rule applies | Standard 2-year rule applies |

Source: Fannie Mae Selling Guide B3-5.3-07 (selling-guide.fanniemae.com); FHA Single Family Housing Policy Handbook 4000.1. Extenuating circumstances may shorten waiting periods — consult a mortgage professional for your specific situation.

What "extenuating circumstances" means: For conventional loans, documented one-time hardships beyond your control — sudden medical emergency, job loss, death of a co-borrower — may allow shorter waiting periods in some cases. This requires substantial documentation and lender discretion. It is the exception, not the rule.

Important: These are minimum waiting periods. Your score, debt-to-income ratio, and the rest of your credit file still need to meet the lender's full requirements. Meeting the waiting period only gets you to the starting line.

FICO Score 9 and VantageScore 4.0 — The Exceptions {#fico9-exceptions}

Quick answer: If you pay off a collection account, FICO Score 9 and VantageScore 4.0 will no longer penalize you for it. The problem is that most mortgage lenders do not use these newer models yet.

Two of the more recent scoring models treat paid collections differently from their predecessors:

FICO Score 9 ignores collection accounts that have been paid off and show a zero balance. This means paying a collection can give your FICO 9 score a meaningful boost — sometimes 20 to 50 points depending on the size of the collection and your overall file.

VantageScore 4.0 goes further — it excludes paid collections entirely, and it also gives significantly reduced weight to medical collections compared to other debt types. Medical debt is heavily discounted in this model because research shows it is a poor predictor of default behavior compared to credit card or auto loan debt.

The catch for mortgage applicants: The mortgage industry still relies predominantly on older FICO models — specifically FICO 2, FICO 4, and FICO 5, one from each bureau — which do not give paid collections the same treatment. When you apply for a mortgage, the score your lender pulls may be 30 to 60 points lower than the VantageScore you see on a free monitoring app. A paid collection still shows up as a derogatory mark in these older models.

This is worth knowing when you're planning strategy. Paying a collection is still generally the right move — it clears your legal obligation, it helps with newer models, and lenders view a paid collection more favorably than an unpaid one during manual underwriting. But do not assume paying will erase the damage from your mortgage application score.

Proactive Ways to Remove Derogatory Marks Early {#remove-early}

Quick answer: Two methods work — disputing inaccuracies under the FCRA, and requesting goodwill removal from the original creditor. A third method, pay-for-delete, applies specifically to collection accounts.

1. Dispute Inaccurate Items Under the FCRA

Under the Fair Credit Reporting Act, every consumer has the right to an accurate credit report. If a derogatory mark contains an error — wrong date, wrong balance, account that is not yours, or a mark that has passed its legal reporting period — you can dispute it with the credit bureau reporting it.

Each consumer reporting agency (Equifax, Experian, TransUnion) must complete its reinvestigation within 30 days of receiving your dispute, or 45 days if you submit additional documentation. If the item cannot be verified by the information furnisher, the bureau must remove it.

Dispute directly with: Experian, Equifax, and TransUnion.

For a free copy-paste FCRA-compliant dispute letter and step-by-step walkthrough, see our dispute letter template.

A Federal Trade Commission study found that roughly one in five consumers had an error on at least one of their three credit reports. Errors are common. Check your reports at AnnualCreditReport.com — you're entitled to free weekly reports from all three bureaus.

2. Goodwill Letter to the Original Creditor

If the derogatory mark is accurate, a goodwill letter asks the original creditor to remove it as a courtesy. It works best when: the late payment was a genuine one-time incident caused by a specific hardship (job loss, medical emergency, autopay failure), and you have a long history of on-time payments with that creditor before and after the incident.

Success rates are roughly 10 to 30 percent, with credit unions and smaller lenders responding more often than large banks. Always send the letter directly to the original creditor — not to the credit bureau. The bureau reports what the creditor tells it; only the creditor can request removal.

If you are considering professional help with this process, our honest guide on whether credit repair companies really work walks through exactly what they can and cannot do for you. For professionals managing credit files for multiple clients, credit repair software can help track disputes and goodwill requests systematically.

3. Pay-for-Delete (Collections Only)

If a collection account is still showing on your report, you can sometimes negotiate with the collection agency to remove the mark entirely in exchange for payment. This is called a pay-for-delete agreement.

The key rules: always get the agreement in writing before sending payment — verbal promises from collectors are unenforceable. Pay-for-delete success rates are low (roughly 5 to 15 percent), but for a significant balance the potential payoff is worth the attempt. Note that pay-for-delete applies to the collection account, not necessarily to the original charge-off from the initial creditor, which may still appear separately.

How to Rebuild Your Credit While You Wait {#rebuild}

Quick answer: You do not have to wait for marks to fall off before your score improves. Building positive payment history now progressively dilutes the weight of old derogatory marks.

The most effective rebuilding tools:

Secured credit cards. You deposit a small amount as collateral, and that becomes your credit limit. Use it lightly, pay it in full every month, and every on-time payment builds your positive history. Look for cards that report to all three bureaus and have low or no annual fees.

Credit-builder loans. Offered by many credit unions and community banks. The loan amount is held in a savings account while you make small monthly payments. You get the money at the end, and you get a clean installment loan payment record added to your credit file.

Authorized user status. If someone with excellent credit adds you as an authorized user on one of their longstanding accounts, their good payment history can appear on your report and boost your score — even if you never use the card.

Keep utilization below 10%. Credit utilization is 30% of your FICO score — the second-biggest factor after payment history. Keeping balances low relative to your credit limits has one of the fastest impacts on your score of anything you can do right now. Paying down existing balances can move the needle in 30 to 60 days.

Set up credit monitoring through AnnualCreditReport.com or your bank's free monitoring tool. This gives you early alerts when account statuses change, inquiries appear, or new marks are added — catching errors before they compound.

For a complete action plan with the highest-impact steps to accelerate your score recovery, see our credit repair tips guide. And if you're working through our full credit repair guide for 2026, derogatory marks are one chapter of a broader recovery process that covers every factor in your score.

FAQ {#faq}

How long do derogatory marks stay on your credit report? Most derogatory marks — late payments, collections, charge-offs, repossessions, foreclosures, and Chapter 13 bankruptcy — stay for seven years from the original delinquency date. Chapter 7 bankruptcy is the one exception at 10 years from the filing date. Their impact on your score fades over time, particularly after the first two years of consistent positive payment behavior.

When does the 7-year clock start? It starts from the date of first delinquency — the date you first missed the payment that triggered the negative chain reaction. Not the charge-off date, not the collection date, not the last payment date. This is one of the most misunderstood rules in credit reporting. Paying a debt, having it sold to a collector, or having it charged off does not reset or extend this clock.

Does paying a collection account remove it from your credit report? No. Paying updates the status to "paid" but does not remove the mark. The derogatory history remains for the full seven years. However, FICO Score 9 and VantageScore 4.0 ignore paid collections, which may improve the score your lender sees if they use one of these models. Most mortgage lenders still use older FICO models where paid collections continue to show up as negatives.

What is re-aging, and is it illegal? Re-aging is the illegal practice of changing the original delinquency date on a credit report to make an old debt appear more recent, effectively extending how long it shows on your report. It is a violation of the FCRA. If you spot a date that has shifted from your own records, dispute it with the bureau immediately and file a complaint at ConsumerFinance.gov.

What is the difference between a charge-off and a collection? A charge-off is an accounting move by the original creditor — they write off your debt as a loss after about 120 to 180 days of non-payment. A collection happens when the creditor sells that debt to a third-party agency. One unpaid bill can generate two separate derogatory marks. Both follow the same 7-year clock starting from the original missed payment date.

How long after bankruptcy can you get a mortgage? For Chapter 7: 4 years for conventional, 2 years for FHA or VA from the discharge date. For Chapter 13 discharged: 2 years for conventional, 1 year for FHA or VA. For foreclosure: 7 years for conventional, 3 years for FHA, 2 years for VA. Extenuating circumstances with documentation may shorten some of these for conventional loans.

Can old derogatory marks reappear after falling off? No. Once a mark has hit its legal reporting limit and been removed, it cannot legally reappear. If it does, that is re-aging — a FCRA violation. Dispute it with the bureau and file a complaint with the CFPB.

How many points does each derogatory mark drop your credit score? It depends on the mark and your starting score. A 30-day late payment can cost 90 to 110 points on a score above 780. A collection or charge-off can drop the same score 100 to 125 points. Chapter 7 bankruptcy causes the most damage — up to 150 to 240 points for a high starting score. Lower starting scores see smaller drops because the statistical deviation from the established pattern is less significant.

Sources

- Fair Credit Reporting Act (FCRA), 15 U.S.C. § 1681c — FTC

- CFPB complaint portal — ConsumerFinance.gov

- FICO Score — how derogatory marks affect your score — myFICO.com

- Fannie Mae Selling Guide B3-5.3-07 — Fannie Mae

- AnnualCreditReport.com — federally authorized free credit reports

- FTC study on credit report accuracy — one in five consumers had an error on at least one report

This article is for general educational purposes only. It does not constitute legal or financial advice. Credit outcomes depend on your individual circumstances. Consult a licensed professional for guidance specific to your situation.

Score Machine CTA

Not sure exactly when each derogatory mark on your report is scheduled to fall off — or which ones are still actively damaging your score vs nearly aged out? Score Machine analyzes your full credit file and gives you a clear, account-by-account picture. Analyze my credit →