GAP Insurance: What It Is, How It Works, and Who Needs It in 2026

The Direct Answer: What Is GAP Insurance?

GAP insurance (Guaranteed Asset Protection) pays the difference between your car's actual cash value (ACV) and the outstanding balance on your auto loan or lease when your vehicle is totaled or stolen. Without it, you're personally responsible for that shortfall — which can range from $3,000 to $10,000 or more.

Here's why this matters right now: According to Edmunds' Q4 2025 Insights Report, 29.3% of all trade-ins toward new-vehicle purchases were underwater — meaning the owner owed more than the vehicle was worth. The average negative equity on those trade-ins hit a record $7,214. Nearly one in three car buyers is walking around with a financial gap that could cost them thousands if their car is totaled tomorrow.

GAP insurance eliminates that risk. It typically costs $20–$400 per year through your auto insurer, compared to $400–$1,000+ at a dealership. This guide will help you determine whether you need it, where to buy it, and how to avoid the most expensive mistakes.

Real-World Case Study: What Happens Without GAP Insurance

In my experience advising consumers on auto financing decisions, I've seen the same scenario play out repeatedly. Here's a real-world composite drawn from cases I've encountered:

The situation: A buyer purchases a 2025 Hyundai Tucson for $36,000. She puts $1,500 down and finances the rest over 72 months at 7.2% APR. Fourteen months later, she's rear-ended on the highway. The car is declared a total loss.

| Detail | Amount | Source/Basis |

|---|---|---|

| Purchase price | $36,000 | — |

| Loan balance after 14 months | $32,400 | Based on standard amortization at 7.2% APR |

| Vehicle's actual cash value (ACV) at time of loss | $27,000 | ~25% depreciation (KBB estimates ~20% first year) |

| Insurance payout | $27,000 | Insurer pays ACV |

| Remaining balance owed to lender | $5,400 | $32,400 − $27,000 |

| With GAP insurance | $0 out of pocket | GAP covers the $5,400 difference |

Without GAP coverage, she owes the bank $5,400 for a car she can't drive. She still needs transportation, so she's now financing a second vehicle while paying off the first. This is the exact debt spiral that Edmunds identified when they reported that buyers who rolled negative equity into new loans paid an average monthly payment of $916 — $144 more than the industry average of $772.

The takeaway from hundreds of similar cases: Drivers who purchased GAP through their auto insurer spent $60–$120 per year for coverage and paid $0 after a total loss. Drivers who skipped it typically faced $3,000–$8,000 in unexpected out-of-pocket costs. If you're carrying any auto loan debt and have limited savings, that risk-reward calculation isn't close.

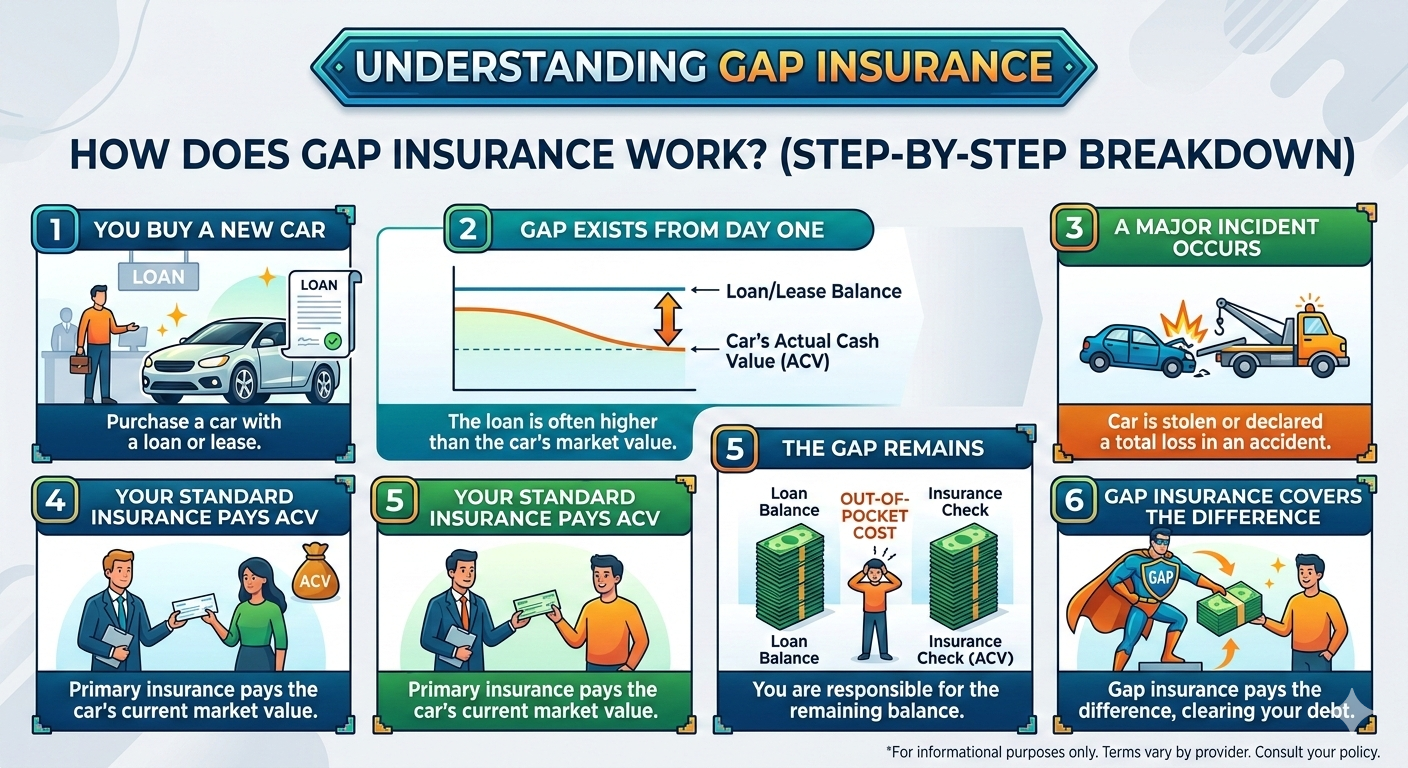

How Does GAP Insurance Work? (Step-by-Step Breakdown)

GAP insurance is a secondary coverage that activates only after your primary auto insurance (comprehensive and collision) has paid out. Here's the exact sequence:

- Your car is totaled or stolen. This triggers a claim with your regular auto insurer.

- Your insurer determines the ACV. They calculate your vehicle's fair market value based on depreciation, mileage, condition, and comparable sales.

- Your insurer pays the ACV to your lender. This satisfies the "market value" portion of your loan.

- A shortfall remains. If you owe more than the car was worth, the leftover balance is still your responsibility.

- GAP insurance pays the difference. Your GAP provider sends the remaining balance directly to your lender, closing out the loan.

Important: You must carry comprehensive and collision coverage for GAP insurance to work. GAP never replaces your primary auto policy — it supplements it.

Why the "Gap" Exists: The Depreciation-Amortization Mismatch

Two financial forces collide to create negative equity:

Force #1 — Depreciation moves fast. According to Kelley Blue Book, new cars lose approximately 20% of their value in the first year. After five years, the average 2025 model-year vehicle retains only about 45% of its original value, per KBB's 2025 Best Resale Value Awards analysis.

Force #2 — Loan amortization moves slow. Auto loans are front-loaded with interest. In the first year of a 72-month loan at 7% APR, roughly 40% of each payment goes to interest, not principal. Your balance barely budges while your car's value drops rapidly.

This creates a predictable window — typically the first 2–4 years — where you owe significantly more than the car is worth.

| Ownership Year | Approximate Value Retained | Typical Loan Balance ($36K, 72-month, 7% APR) | Estimated Gap |

|---|---|---|---|

| Day 1 (off the lot) | ~$32,400 (−10%) | $36,000 | $3,600 |

| Year 1 | ~$28,800 (−20%) | $32,400 | $3,600 |

| Year 2 | ~$24,500 (−32%) | $28,500 | $4,000 |

| Year 3 | ~$21,600 (−40%) | $24,200 | $2,600 |

| Year 4 | ~$19,400 (−46%) | $19,500 | ~$100 (near breakeven) |

Values are illustrative estimates. Actual figures depend on vehicle make/model, down payment, and APR. Depreciation rates sourced from Kelley Blue Book and Experian.

How Much Does GAP Insurance Cost in 2026?

The cost difference between purchase channels is dramatic. This is the number one area where consumers overpay.

Cost Comparison by Purchase Channel

| Where You Buy | Typical Cost | How It's Paid | Can You Cancel? |

|---|---|---|---|

| Auto insurance add-on (Progressive, Allstate, Erie, Nationwide, Travelers) | $20–$400/year (avg. ~$90/year) | Monthly premium | Yes — cancel anytime, premium drops immediately |

| Credit union (bundled with auto loan) | $0–$300 | Included or one-time fee | Varies by credit union |

| Standalone GAP provider | $200–$400 one-time | Upfront | Yes — check cancellation terms |

| Car dealership (F&I office) | $400–$1,000+ one-time | Rolled into loan (you pay interest on it) | Yes — prorated refund applied to loan balance |

Cost ranges based on data compiled from Insurance.com, Insure.com, and MoneyGeek.

Dealership vs. Insurer: A Side-by-Side Cost Example

Scenario: $38,000 vehicle, 72-month loan at 6.9% APR.

| Dealership GAP ($695 rolled into loan) | Auto Insurer GAP ($7.50/month) | |

|---|---|---|

| Total cost if kept 3 years | ~$780 (including ~$85 interest) | $270 |

| Total cost if kept full loan term | ~$780 | $540 |

| Savings by choosing insurer | — | $240–$510 |

Most people don't realize the dealership's GAP fee accrues interest when it's financed into the loan. At 6.9% APR over 72 months, a $695 GAP fee costs approximately $780 total.

The Consumer Financial Protection Bureau (CFPB) advises consumers to compare add-on product costs before purchasing them at dealerships.

What Affects Your GAP Premium?

- Down payment size: Less than 20% down = higher premium

- Loan term: 72–84 month loans carry more risk than 48-month terms

- Vehicle type: Luxury cars and EVs depreciate faster, raising premiums

- Credit score: Scores below 650 may increase costs

- Driving record: At-fault accidents can raise premiums

- Location: Nevada, Florida, and Michigan tend to be more expensive; Maine and New Hampshire are among the cheapest

- Vehicle age/mileage: Most providers limit coverage to vehicles under 3 model years old

If you're working with a challenging credit situation and already paying higher interest rates, GAP insurance becomes even more critical because higher APRs mean slower principal reduction. For guidance on managing auto financing with less-than-perfect credit, see our complete guide on Bad Credit Car Loans in 2026: The Complete Guide.

Who Needs GAP Insurance? (Decision Framework)

You Likely Need GAP Insurance If:

| Your Situation | Why GAP Is Important |

|---|---|

| Down payment was less than 20% | You likely started with negative equity on day one |

| Loan term is 60 months or longer | Principal reduces slowly; depreciation outpaces your payments |

| You're leasing a vehicle | Many lease agreements contractually require GAP |

| You drive an EV or luxury vehicle | EVs lose 58.8% of value in 5 years (iSeeCars, 2025 study); luxury cars often lose 50%+ |

| You rolled negative equity from a trade-in | You're financing more than the car is worth from the start |

| You drive 15,000+ miles per year | Higher mileage accelerates depreciation |

| You have a high-interest loan (7%+ APR) | More of each payment goes to interest, less to principal |

| You have limited emergency savings | A $3,000–$8,000 unexpected expense could be devastating |

You Can Probably Skip GAP Insurance If:

- You made a 20%+ down payment

- Your loan term is 48 months or shorter

- You drive a vehicle with strong resale value (Toyota Tacoma, Honda Civic, Subaru Outback — all lose less than 31% in 5 years per iSeeCars)

- Your car is paid off or nearly paid off

- You have $5,000–$10,000+ in liquid savings to cover a potential shortfall

The 60-Second Equity Check

Do this right now to see where you stand:

- Look up your car's trade-in value at Kelley Blue Book or Edmunds

- Check your current loan payoff through your lender's app or website

- Subtract: Loan Payoff − Trade-In Value = Your Gap

If the number is positive, you have negative equity — and you should strongly consider GAP insurance. If it's negative, you have equity and can safely skip or cancel existing GAP coverage.

What Does GAP Insurance Cover? (And What It Doesn't)

What's Covered

- The difference between your vehicle's ACV and your remaining loan or lease balance

- Applies when your car is declared a total loss from a covered accident

- Applies when your car is stolen and not recovered

- Some policies (such as Allstate's) also cover your collision/comprehensive deductible up to $1,000

What's NOT Covered

- Damage that doesn't result in a total loss (partial repairs)

- Mechanical breakdowns, engine failure, or normal wear

- Delinquent or missed loan payments

- Late fees, penalties, or lease-end charges like excess mileage

- Extended warranties or aftermarket accessories financed into your loan

- Negative equity rolled in from a previous trade-in (excluded by many policies — this is the most overlooked exclusion)

- Down payment on a replacement vehicle

The Rolled Negative Equity Trap

This is the exclusion I see catch people most often. In Q4 2025, Edmunds reported that 27% of underwater trade-ins carried $10,000 or more in negative equity, with 9.2% owing more than $15,000. Many of those buyers roll old debt into new loans.

Here's the problem: most standard GAP policies only cover the difference between your car's ACV and the original financed amount for the current vehicle — not the inflated balance that includes prior debt. If you rolled $6,000 of old negative equity into your current loan, that $6,000 may not be covered.

Always ask your provider directly: "Does this policy cover negative equity carried over from a previous trade-in?" Get the answer in writing before you purchase.

Drivers with bad credit are especially vulnerable to this cycle because they often face higher interest rates and longer loan terms that slow equity growth. If this applies to you, our guide on Bad Credit Car Loans in 2026 covers strategies for building equity faster and avoiding the negative equity trap.

GAP Insurance vs. Loan/Lease Payoff vs. New Car Replacement

These three products serve different purposes. Choosing the wrong one is a common and costly mistake.

| Feature | GAP Insurance | Loan/Lease Payoff | New Car Replacement |

|---|---|---|---|

| What it pays | 100% of gap between ACV and loan balance | Up to 25% above ACV (applied to loan) | Cost of a new vehicle of same make/model/year |

| Who receives payment | Your lender | Your lender | You (or applied toward replacement) |

| Available for | New and used vehicles (typically < 3 model years) | New and used | New vehicles only (first 1–2 model years) |

| Offered by | Most major insurers, dealerships, standalone providers | State Farm, Farmers (select insurers) | Liberty Mutual, Allstate (select insurers) |

| Best for | Drivers with significant negative equity | Drivers with moderate negative equity (gap < 25% of ACV) | Drivers who want full replacement, not just debt relief |

| Typical cost | $20–$400/year | Similar to GAP | $30–$100/year |

Key distinction: If you owe $35,000 on a car worth $25,000, that's a $10,000 gap (40% of ACV). Loan/lease payoff would cover only 25% of $25,000 = $6,250, leaving you $3,750 short. Traditional GAP insurance covers the full $10,000.

Important note on USAA: USAA's "Car Replacement Assistance" pays 20% above ACV directly to you, not your lender. Available only to military members and families. It functions differently from traditional GAP insurance.

GEICO does not offer GAP insurance. If you're a GEICO customer, you'll need to purchase GAP from your lender, a standalone provider, or your dealership.

The 2026 Negative Equity Crisis: Why GAP Insurance Matters More Now

The financial landscape for car owners has shifted significantly. Here are the verified data points that explain why GAP insurance is more relevant in 2026 than it has been in years.

Verified Market Data

| Statistic | Figure | Source (with link) |

|---|---|---|

| Share of new-car trade-ins with negative equity (Q4 2025) | 29.3% (highest since Q1 2021) | Edmunds Q4 2025 Report |

| Average negative equity on underwater trade-ins (Q4 2025) | $7,214 (all-time record) | Edmunds, confirmed by CNBC |

| Underwater trade-ins with $10,000+ negative equity | 27% (record high) | Edmunds Q4 2025 Report |

| Average monthly payment for buyers who rolled negative equity | $916 ($144 above industry avg. of $772) | Edmunds Q4 2025 Report |

| Negative-equity purchases financed with 84-month loans | 40.7% | Edmunds Q4 2025 Report |

| New car depreciation in year one | ~20% | Kelley Blue Book |

| Average 2025 model-year vehicle value retained after 5 years | ~45% (loses ~55%) | KBB 2025 Best Resale Value Awards |

| EV 5-year depreciation rate | 58.8% (industry avg: 45.6%) | iSeeCars 2025 study (800,000+ vehicles analyzed) |

| Average full-coverage auto insurance cost (2025) | $2,144 (down 6% from 2024) | Insurify 2025 Report |

Three Forces Making Negative Equity Worse in 2026

1. Pandemic-era loans are aging badly. Millions of loans originated in 2021–2023 when vehicle prices were inflated due to chip shortages. Those cars are now depreciating toward normal levels, but the loan balances remain elevated. As Edmunds' Director of Insights Ivan Drury explained, these loans are aging into a market where values are no longer inflated.

2. Ultra-long loan terms are standard. Edmunds found that 40.7% of new-vehicle purchases involving negative equity were financed with 84-month loans. Seven-year auto loans mean borrowers spend years in the negative equity danger zone before building any meaningful equity.

3. EV depreciation remains severe. The 2025 iSeeCars study of 800,000+ used vehicles found that EVs lose 58.8% of their value in five years — nearly 13 percentage points worse than the industry average of 45.6%. Trucks (40.4%) and hybrids (40.7%) performed dramatically better.

Where to Buy GAP Insurance (Ranked by Value)

1. Your Auto Insurance Provider (Best Value)

This is the cheapest and most flexible option for most drivers. You add GAP as a line item to your existing comprehensive and collision policy.

Insurers that offer GAP coverage: Progressive, Allstate, Erie, Nationwide, Auto-Owners, Travelers

Insurers that do NOT offer GAP: GEICO (not available), State Farm (offers loan/lease payoff — different product, limited to 25% above ACV)

2. Your Credit Union or Bank

Many credit unions include GAP coverage free or at low cost with their auto loans. Before financing through a dealership, ask your credit union whether GAP is included. This is the most underutilized option.

3. Standalone GAP Providers

Independent companies sell GAP policies directly. Useful if your insurer doesn't offer it or if you want specific features like deductible coverage.

4. The Dealership (Most Expensive — Proceed with Caution)

The dealership's F&I (Finance & Insurance) office is where GAP carries the highest markup. The product is functionally identical to what you'd buy elsewhere, but priced 3–5x higher. The Texas Department of Insurance specifically warns consumers to check with their auto insurer before buying GAP at the dealership, noting that dealer GAP products may not even be regulated as insurance in some states.

If you already bought GAP at the dealership: Check your contract for cancellation terms. Most policies are cancellable with a prorated refund applied to your loan balance.

How to File a GAP Insurance Claim

| Step | Action | When |

|---|---|---|

| 1 | File a claim with your primary auto insurer (comprehensive or collision) | Immediately after the total loss or theft |

| 2 | Obtain the insurance settlement letter showing the ACV and payout amount | Within 1–2 weeks of claim |

| 3 | Request a current loan payoff statement from your lender | Same time as step 2 |

| 4 | Contact your GAP provider to initiate the claim | Within 48 hours of receiving your settlement |

| 5 | Submit documents: settlement letter, payoff statement, police report (if applicable), GAP policy | As soon as documents are ready |

| 6 | GAP provider calculates the difference and pays your lender directly | 2–4 weeks after submission |

Critical deadline: Most GAP policies require claims within 30–90 days of the loss. Missing this window can void your claim. Don't wait.

Tip: Before accepting your insurer's ACV determination, verify it against KBB and Edmunds valuations. If the ACV seems low, you have the right to negotiate or request an independent appraisal. A higher ACV means a smaller gap — which benefits you regardless.

7 GAP Insurance Mistakes Most People Make

1. Buying at the Dealership Without Comparing Prices

Dealerships charge $400–$1,000+ for the same product your insurer offers for $60–$120 per year. Always get a quote from your insurance company first.

2. Keeping GAP Coverage After Building Equity

Once your loan balance drops below your car's market value, GAP insurance serves no purpose. Check your equity position every 6–12 months and cancel when you're above water.

3. Assuming a Lease Automatically Includes GAP

Some manufacturers (Toyota Financial Services, Honda Financial Services, BMW Financial Services) include GAP in their leases. Others (Chrysler Capital, Ally Financial) often don't. Read your lease contract or call the leasing company directly.

4. Ignoring the Rolled Negative Equity Exclusion

If you rolled old debt into your current loan, your GAP policy may not cover that amount. This is critical given that 27% of underwater trade-ins now carry $10,000+ in negative equity (Edmunds, Q4 2025).

5. Paying for Duplicate Coverage

Check three places before buying: your auto insurance declarations page, your loan agreement, and your lease contract. Some lenders and credit unions automatically include GAP.

6. Confusing GAP Insurance with Loan/Lease Payoff Coverage

These are different products. Loan/lease payoff (State Farm, Farmers) typically covers only up to 25% above ACV. For large negative equity balances, this may not be enough.

7. Forgetting to Cancel After Paying Off or Refinancing

If you pay off your loan, refinance, or sell the vehicle, cancel your GAP policy immediately. If you bought through a dealership, submit a written cancellation request — you're entitled to a prorated refund per the CFPB.

GAP Insurance for Specific Vehicle Types

Electric Vehicles (EVs)

The 2025 iSeeCars study (analyzing 800,000+ used vehicles sold between March 2024 and February 2025) found EVs depreciate 58.8% in five years — the worst of any vehicle type. The industry average is 45.6%. The Jaguar I-Pace led with a 72.2% loss. Even Tesla's Model 3, the best-performing EV, lost 55.9%.

If you're financing an EV, GAP insurance is essential. The depreciation curve is steeper, less predictable, and heavily influenced by manufacturer price cuts and shifting tax credits.

Used Cars

GAP coverage isn't limited to new vehicles. Used cars depreciate at 10–15% annually (slower than new cars), but if you financed with minimal down payment, you can still be underwater. Most insurers offer GAP for used vehicles under 3 model years and 50,000 miles.

Leased Vehicles

Always verify whether your lease includes GAP before purchasing a separate policy. Contact your leasing company directly — don't rely on assumptions or the dealership's word.

How to Cancel GAP Insurance and Get a Refund

| Where You Bought | How to Cancel | Refund? |

|---|---|---|

| Auto insurer add-on | Call insurer or modify your policy online | Yes — premium stops immediately |

| Dealership | Submit written request to F&I department | Yes — prorated refund applied to loan balance |

| Standalone provider | Contact provider directly | Check for early termination fees |

| Credit union (included) | No action needed if vehicle is sold/paid off | Not applicable |

The CFPB confirms your right to cancel add-on financial products like GAP insurance and receive applicable refunds. If a dealership resists, file a complaint at consumerfinance.gov.

Fact-Check Table: Every Key Claim Verified

| Claim in This Article | Exact Figure | Primary Source | Confirmed By |

|---|---|---|---|

| 29.3% of trade-ins had negative equity, Q4 2025 | 29.3% | Edmunds Q4 2025 Report | CNBC, CBT News |

| Average negative equity reached $7,214 (record) | $7,214 | Edmunds Q4 2025 Report | CNBC, Jalopnik |

| 27% of underwater trade-ins had $10K+ negative equity | 27% | Edmunds Q4 2025 Report | CU Today |

| Buyers with rolled negative equity paid avg. $916/month | $916 | Edmunds Q4 2025 Report | CNBC |

| 40.7% of negative-equity purchases used 84-month loans | 40.7% | Edmunds Q4 2025 Report | CU Today |

| New cars lose ~20% of value in year 1 | ~20% | Kelley Blue Book | CARFAX, Experian, State Farm |

| Average 2025 vehicle retains ~45% of value after 5 years | ~45% | KBB 2025 Best Resale Value Awards | iSeeCars (reports 45.6% industry avg. depreciation) |

| EVs lose 58.8% of value in 5 years | 58.8% | iSeeCars 2025 study | Autoblog, Consumer Affairs, Carscoops |

| Avg. full-coverage auto insurance: $2,144 (2025) | $2,144 | Insurify 2025 Report | InsuranceNewsNet |

| GAP costs $20–$400/year (insurer) vs. $400–$1,000+ (dealer) | See ranges | Insurance.com, Insure.com | MoneyGeek, WalletHub |

Frequently Asked Questions (FAQ)

Is GAP insurance worth it in 2026?

Yes, for most financed or leased vehicles — particularly if you made a down payment below 20%, have a loan term over 60 months, or drive a vehicle with above-average depreciation. At $5–$10 per month through an auto insurer, the cost is minimal compared to the $3,000–$10,000+ you could owe after a total loss. With 29.3% of trade-ins now underwater (Edmunds, Q4 2025), the risk is real and well-documented.

Does GAP insurance cover my deductible?

Most standard policies do not. However, Allstate's GAP product includes up to $1,000 in deductible coverage. Ask your provider specifically about deductible reimbursement before purchasing.

Can I buy GAP insurance after I already purchased my car?

Yes. Most auto insurers allow you to add GAP coverage at any point during your loan or lease term, provided your vehicle meets their age and mileage requirements (typically under 3 model years). You do not need to buy it at the dealership at the time of purchase.

Is GAP insurance legally required?

No state legally mandates GAP insurance. However, many lease agreements contractually require it — violating this term could breach your lease. Some lenders also require GAP for high-LTV loans.

Does GAP insurance cover a stolen car?

Yes. If your vehicle is stolen and not recovered, GAP covers the difference between the ACV payout and your remaining loan balance, the same as it would for a total loss from an accident.

When should I cancel GAP insurance?

Cancel when your loan payoff amount drops below your car's current trade-in value. For most drivers, this occurs between years 2 and 4, depending on down payment, loan term, and depreciation rate. Check every 6–12 months using the equity check method described above.

What's the difference between GAP insurance and "full coverage"?

"Full coverage" is an informal term that usually means liability + comprehensive + collision insurance. GAP is a separate add-on that sits on top of comprehensive and collision. You must have comp and collision for GAP to function.

Does GAP insurance pay me directly?

No. GAP pays your lender directly to close out the remaining loan balance. You do not receive a check. The exception is USAA's Car Replacement Assistance, which pays you directly.

Can I get GAP insurance from GEICO?

No. GEICO does not currently sell GAP insurance. GEICO customers need to purchase GAP from a standalone provider, credit union, or dealership.

How long does a GAP claim take to process?

Most claims are resolved within 2–4 weeks after all documentation is submitted. Delays usually result from incomplete paperwork or disputes over the primary insurer's ACV determination.

Is GAP insurance worth it on a used car?

It can be, depending on your financing terms. If you financed a used car with little or no down payment and owe more than it's worth, GAP coverage protects you from the same risk as a new car buyer. However, used cars depreciate more slowly (10–15% per year vs. 20% for new), so the window of negative equity is shorter.

Final Verdict: Should You Buy GAP Insurance?

Buy GAP insurance if any of these apply:

- Down payment less than 20%

- Loan term over 60 months

- Leasing (and lease doesn't include GAP — verify this)

- Driving an EV or high-depreciation vehicle

- Rolled negative equity from a previous trade-in

- High annual mileage (15,000+ miles)

- APR above 7% (common with bad credit car loans)

- Limited emergency savings (under $5,000)

Skip GAP insurance if:

- Car is paid off or nearly paid off

- 20%+ down payment with 48-month or shorter loan

- Vehicle holds value exceptionally well (Toyota, Honda, Subaru)

- $5,000–$10,000+ in liquid savings as a buffer

Where to buy (in priority order): Auto insurer → Credit union → Standalone provider → Dealership (last resort)

For $5–$10 per month, you're protecting against a $3,000–$10,000+ loss. In a market where nearly 30% of trade-ins are underwater and the average negative equity balance is at an all-time record high, that's one of the most straightforward risk calculations a car owner can make.

Sources & Further Reading

- Edmunds — Q4 2025 Insights Report: Negative Equity Data

- CNBC — Underwater Car Trade-Ins Are on the Rise (January 2026)

- Consumer Financial Protection Bureau (CFPB) — Auto Loans Consumer Tools

- Kelley Blue Book — Car Depreciation Calculator

- Experian — How Much Do Cars Depreciate Per Year?

- iSeeCars — Cars That Hold Their Value: 2025 Study

- Insurify — 2025 Auto Insurance Affordability Report

- Texas Department of Insurance — GAP Insurance Consumer Guide

- Insurance.com — How Much Is GAP Insurance in 2026?

- Insure.com — Average Cost of GAP Insurance in 2026

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. All statistics and data points are sourced from the publications cited above and were verified as of February 2026. Coverage terms, pricing, and availability vary by provider, state, and individual circumstances. Always review your specific policy documents and consult with a licensed insurance professional before making coverage decisions. The author is not affiliated with any insurance company mentioned in this article.

Last updated: February 2026