Yes, debt consolidation does affect your credit score—but it's not a simple yes or no answer. Think of it as a two-act play: a small, temporary dip at the beginning, followed by the potential for a significant, long-lasting improvement if you play your cards right.

The Real Answer to How Consolidation Affects Your Credit

If you're feeling buried under a mountain of different bills—credit cards, store cards, personal loans—you're not alone. I’ve seen countless people staring at a stack of statements, each with its own due date and high-interest rate, wondering if there’s a smarter way out. You've probably heard about debt consolidation, but the big question is always the same: will it help or hurt my credit score?

Let's cut through the noise. The process is a bit like renovating a room. First, you have to clear everything out and maybe even tear down a wall. It looks messy for a little while (that's the temporary score drop), but it's a necessary step to build something far better and more stable for the long haul.

This guide is your straightforward, no-jargon roadmap. We're going to break down exactly what happens to your credit score, why it happens, and how you can steer the process to come out financially stronger on the other side.

Why Your Score Changes in the First Place

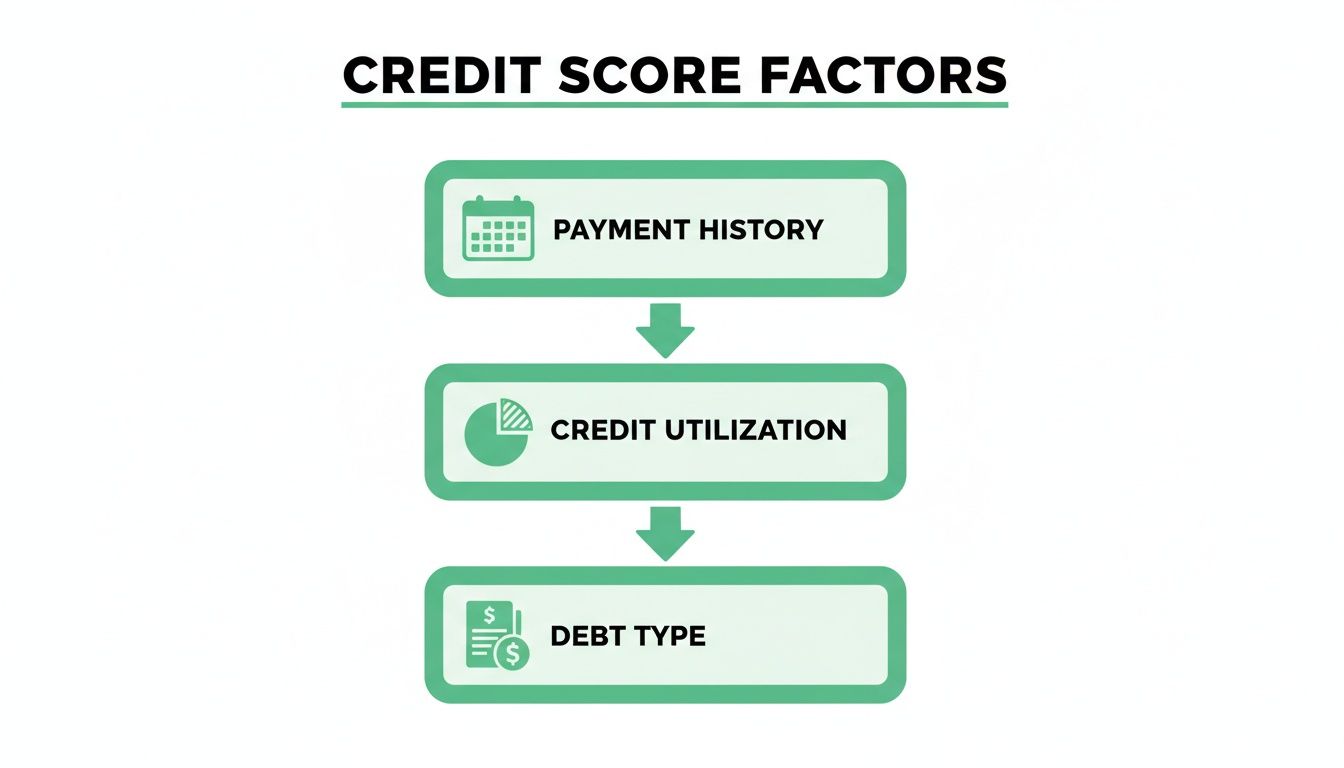

Your credit score isn't just one random number; it's calculated using five key ingredients. Debt consolidation happens to touch on nearly all of them, which is why you see those score movements. Understanding this is the key to using consolidation as a powerful tool instead of a source of stress.

According to Experian, the main components of your score are payment history, amounts owed (utilization), length of credit history, new credit, and credit mix. Here’s a quick rundown of how consolidation interacts with them:

-

The Application: When you apply for a consolidation loan or balance transfer card, the lender pulls your credit report. This is called a "hard inquiry," and it can ding your score by a few points right away.

-

The New Account: Opening a brand-new loan lowers the average age of all your credit accounts. Since older accounts are generally better for your score, this can also cause a small, temporary dip.

-

The Big Payoff: Here’s where the magic happens. When you use that new loan to wipe out your high-interest credit card balances, you slash your credit utilization ratio. This ratio—how much you owe versus your total credit limit—is a huge deal, making up 30% of your FICO score. Lowering it can give your score a major boost.

-

The Simplified Future: Juggling multiple due dates is stressful and makes it easy to slip up. Consolidating into one single payment makes it far easier to build a flawless payment history, which is the single most important factor for a healthy credit score.

Key Takeaway: The small, short-term negatives (the hard inquiry and newer account age) are usually a small price to pay for the huge long-term wins: a dramatically lower credit utilization and a rock-solid payment history.

Let's dig into the details to see exactly what to expect.

Quick Look: How Consolidation Impacts Your Credit Score

To give you a clearer picture, here’s a table that breaks down the immediate bumps you can expect versus the positive changes that develop over time.

| Credit Score Factor | Short-Term Impact (First 1-3 Months) | Long-Term Potential (After 6+ Months) |

|---|---|---|

| New Credit / Hard Inquiry | Negative (Minor drop) | Effect fades, typically gone in 12-24 months. |

| Credit Utilization | Positive (Major boost) | Sustained positive impact as long as you keep card balances low. |

| Age of Accounts | Negative (Minor drop) | The new account starts to age, contributing positively over time. |

| Payment History | Neutral | Becomes a major positive as you make consistent, on-time payments. |

| Credit Mix | Potentially Positive | Adding an installment loan can diversify your credit mix. |

While the initial score drop can be unnerving, it’s the long-term column where your focus should be. A few points lost today is a small trade-off for a much healthier and higher score in the near future, all thanks to responsible management of your new, simplified debt.

Decoding the Initial Credit Score Dip

Let's get right to the part that makes everyone a little nervous: the temporary drop in your credit score right after you consolidate. It’s almost guaranteed to happen, and it’s completely normal.

When you apply for a new loan or credit card, the lender does what’s called a hard inquiry—a formal peek at your credit report to see how you’ve handled debt in the past. This necessary step can knock your score down by a few points. Think of it as a small, short-term investment for a much bigger long-term gain.

Why the Initial Drop Happens

So, what’s really going on behind the scenes? The dip usually comes down to two key factors that credit scoring models are designed to watch closely.

-

The Hard Inquiry: Every time you officially apply for credit, it leaves a small mark on your report. A flurry of applications in a short period can look like you're desperate for cash, which lenders see as a red flag.

-

Average Age of Accounts: This one is simple math. When you open a brand-new account, it lowers the average age of all your accounts combined. Lenders like to see a long, stable credit history, so a younger average age can temporarily lower your score.

Thankfully, the credit scoring systems have gotten pretty smart about this. They know that savvy consumers shop around for the best loan rates.

If you apply for several similar consolidation loans within a tight window—usually 14 to 45 days—the scoring models will often bundle them together and treat them as a single inquiry. This is a huge help, as it prevents your score from taking a hit for each individual application.

The key is to do your rate shopping efficiently. While both the hard inquiry and the new account's impact on your credit age can cause a temporary dip, these effects are usually minor. You can find more great insights on this from the experts at Money Management International.

Over time, as you make consistent, on-time payments on your new consolidation loan, your score will not only recover but will likely climb higher than it was before.

As you consistently make timely payments on your consolidation loan, your credit score will gradually recover and potentially increase beyond its previous level. For more information on managing loans and improving credit scores, you can visit these resources: Consumer Financial Protection Bureau and Federal Trade Commission.

How Consolidation Can Boost Your Score Long-Term

Once you get past that initial, temporary dip, this is where debt consolidation really starts to pay off. The most significant and lasting boost to your score comes from tackling a huge piece of the credit puzzle: your credit utilization ratio.

Think of this ratio as a measure of how much of your available credit you’re using. It's a massive deal, influencing a whopping 30% of your FICO score. When you take out a new installment loan to wipe out those high credit card balances, you're essentially performing a little financial alchemy. You're moving the debt from a "revolving" bucket (credit cards) into an "installment" one (the loan).

This one move can drastically lower your credit utilization, often giving your score a surprisingly quick lift.

Slashing Your Credit Utilization

Let's make this real. Imagine you have two credit cards, each with a $5,000 limit and a $4,000 balance. That's $10,000 in available credit, but you're using $8,000 of it. Your credit utilization is a sky-high 80%, which lenders see as a major red flag.

Now, you get a consolidation loan and pay off both cards completely. Your revolving balances instantly drop to $0. Just like that, your utilization plummets to 0%. This is, without a doubt, the single biggest way debt consolidation can boost your credit score over the long haul.

Key Insight: Shifting debt from a high-impact revolving account (like a credit card) to a lower-impact installment loan is a powerful strategy. Even though you owe the same amount of money at first, the type of debt changes, and that's what helps your score.

Building a Flawless Payment History

Beyond the numbers game, consolidation just makes your life simpler. Instead of juggling a handful of different due dates, minimum payments, and interest rates, you now have just one. One loan, one payment, one due date. Simple.

This simplicity makes it so much easier to build a perfect payment history, which happens to be the single most important factor in your credit score, accounting for 35% of it. Every single on-time payment you make on that new loan is a positive mark on your credit report, steadily building a more trustworthy profile over time.

And this isn't just a nice theory. A deep-dive study by TransUnion found that 68% of people who consolidated debt saw their credit scores jump by more than 20 points. The reason? A huge drop in their credit card utilization.

By focusing on that one payment every month, you are actively repairing and strengthening your credit. If you're wondering whether your profile is in the right shape for a move like this, it's always a good idea to evaluate your overall credit readiness first.

Choosing the Right Debt Consolidation Method

When it comes to consolidating debt, there's no one-size-fits-all solution. The path you take will directly determine how your credit score reacts—for better or for worse. It’s all about matching the strategy to your financial situation and, just as importantly, your personal discipline.

Personal Loans

For most people, a personal loan is the most straightforward route. You apply for a new loan, and once approved, you get a single lump-sum deposit. You then use that money to pay off all your other high-interest debts, like credit cards or medical bills.

What you're left with is one simple, predictable monthly payment. Because it’s an installment loan with a fixed interest rate, your payment never changes, which makes budgeting so much easier. It's clean and simple.

Balance Transfer Credit Cards

A balance transfer credit card can be a powerful tool, but it's a bit like playing with fire. These cards lure you in with a 0% introductory APR, often for 12 to 18 months. If you have the discipline to pay off the entire balance before that intro period ends, you can save a small fortune in interest.

But here’s the catch: if you don’t pay it off in time, the remaining balance gets slapped with a very high standard interest rate. This option requires a rock-solid plan and the commitment to stick to it.

Home Equity Loans (HELOCs)

Tapping into your home's equity with a Home Equity Loan or HELOC (Home Equity Line of Credit) can get you a fantastic low interest rate. The reason it’s so low is that you’re putting your house up as collateral.

This introduces a serious risk. If life throws you a curveball and you can't make the payments, the lender can foreclose on your home. It's a high-stakes game that should only be considered if you have an extremely stable financial foundation.

A Word of Warning About Debt Settlement

It’s crucial not to confuse debt consolidation with debt settlement. With settlement, a company negotiates with your creditors to let you pay back less than what you originally owed. While it sounds tempting, this is incredibly damaging to your credit report and score for years to come.

Debt settlement is a last-resort option for those in extreme financial distress and is not a strategy for building or protecting your credit.

Debt Consolidation Methods and Their Credit Score Impact

To make things clearer, here’s a quick breakdown of how these common methods can affect your credit score.

| Consolidation Method | Typical Credit Impact | Best For... |

|---|---|---|

| Personal Loan | Short-term dip (hard inquiry, new account), then long-term positive (lower utilization, better credit mix). | Individuals who want a single, fixed payment and a clear end date for their debt. |

| Balance Transfer Card | Short-term dip (hard inquiry, new account), then positive if paid off during the 0% APR period. | Financially disciplined individuals who can aggressively pay off the balance before the intro period expires. |

| Home Equity Loan / HELOC | Short-term dip (hard inquiry). Can improve credit mix. | Homeowners with significant equity and a very stable income who are comfortable using their home as collateral. |

| Debt Settlement | Severe negative impact. Recorded as "settled for less than full amount," which is a major red flag to lenders for 7 years. | Individuals facing extreme financial hardship who have exhausted all other options and are not concerned with their credit score in the short-to-medium term. |

For anyone focused on improving their credit, a personal loan or a well-managed balance transfer is almost always the way to go. When handled correctly, both can set you on a path to a much healthier financial future. Making the right choice upfront is a huge part of a successful loan preparation strategy.

How Funding Companies Increase Approvals with Credit Intelligence

For funding companies, every denied application is a lost opportunity. But what if you could turn a significant portion of those "no's" into future "yes's"? This is where leveraging a credit intelligence platform like The Score Machine becomes a game-changer for increasing funded loans.

Instead of a simple denial, you can provide applicants with a clear, data-driven roadmap to becoming fundable. By simulating the impact of actions like debt consolidation, you transform a rejection into a strategic plan. This builds immense trust and ensures that when the applicant is ready, they come back to you.

Turning Denials into a Profitable Pipeline

When a funding company uses The Score Machine, it can analyze an applicant's credit profile and show them exactly how specific actions will improve their credit score. You're no longer just a lender; you're a partner in their financial journey.

Imagine telling an applicant, "Right now, your credit utilization is too high at 85%. If you consolidate that debt with a personal loan, we project your score will increase by 40 points in three months, making you eligible for funding."

This approach has a direct impact on the bottom line:

-

Increases Client Retention: Applicants with a clear path forward are far more likely to return to your company for funding instead of starting their search over with a competitor.

-

Reduces Acquisition Costs: You retain promising leads that would otherwise be lost, converting them into funded loans without additional marketing spend.

-

Builds a Stronger Portfolio: You cultivate a pipeline of more qualified, financially savvy applicants, leading to higher-quality funded loans and better performance.

By integrating credit intelligence, funding companies can significantly increase their funded volume. They create a loyal client base and a sustainable pipeline of pre-qualified applicants. You can learn more about how it works and see how this strategic shift can boost your business. Empowering clients with actionable insights isn't just good service—it's smart business that leads to more funded deals.

Don't Make These Common Mistakes That Can Wreck Your Credit

Getting that debt consolidation loan can feel like a huge weight off your shoulders. It's easy to think the hard part is over, but what you do next is what really counts for your credit score.

From what I’ve seen over the years, the number one mistake people make is a simple one: they see their zero-balance credit cards as a green light to start spending again. They start racking up new debt, which totally defeats the purpose of the loan.

Before you know it, your credit utilization is right back in the red, and you’re in a financial hole that’s even deeper than the one you just got out of.

How to Dodge Post-Consolidation Traps

Besides the obvious temptation to spend, a few other slip-ups can easily derail your credit-building journey. Watch out for these common traps.

-

Closing Old Credit Cards: It seems like a clean, responsible thing to do, right? Pay off a card, close the account. But this can seriously backfire. When you close a card, you lose its credit limit, which makes your overall credit utilization shoot up. You also erase a piece of your credit history, which can shorten the average age of your accounts—another big factor in your score.

-

Missing a Loan Payment: That new consolidation loan is now a huge piece of your payment history. Even one late payment can undo all your hard work and send your score tumbling. My advice? Set up automatic payments from day one. It’s the easiest way to ensure you're never late.

-

Going on a Credit Application Spree: It's smart to shop around for a good loan rate. But don't follow that up by applying for new store cards, another loan, or anything else. Every application adds a hard inquiry to your report, and too many in a short time makes you look risky to lenders.

Think of consolidation as a fresh start, not just a financial transaction. It's your chance to build better habits. Steering clear of these common mistakes is the most critical part of turning that opportunity into a real financial comeback.

Got Questions? We've Got Answers

Let's tackle some of the most common questions people have when they're thinking about consolidating debt and what it all means for their credit score.

How Long Will a Consolidation Loan Show Up on My Credit Report?

A debt consolidation loan is treated just like any other installment loan—think car loans or mortgages. It will stay on your credit report for the entire time it’s open and you're making payments.

But here's the good part: once you've paid it off and the account is closed, it can remain on your report for up to 10 years. This is actually a huge benefit. That long history of on-time payments continues to work in your favor, boosting your payment history and increasing the average age of your accounts, both of which are major ingredients in a strong credit score.

Will My Credit Score Jump Up After I Pay Off the Loan?

You'll almost certainly see a positive bump in your credit score after paying off a consolidation loan. That final payment closes out the loan successfully, which is a big green flag for any future lender.

But the real magic happens during the life of the loan. Every single on-time payment you make builds a rock-solid payment history. Since payment history is the single most important factor in your credit score, this proves you're a responsible borrower who can be trusted with credit.

Is It Even Possible to Get a Debt Consolidation Loan with Bad Credit?

Yes, it's possible, but you'll have to navigate some hurdles. If your credit is on the lower end, lenders will likely see you as a higher risk, which means they'll probably offer you a loan with a steeper interest rate and less attractive terms. Some lenders do specialize in working with people who have shaky credit, so you have options.

My advice? If you find yourself in this boat, it might be smarter to pause and focus on improving your credit first. A few months spent cleaning up your report and establishing a better payment record could help you qualify for a much better interest rate. That simple move could save you thousands of dollars over the life of the loan.

Tired of guessing how debt consolidation might affect your credit? Get a clear, personalized roadmap. Score Machine uses AI to analyze your credit report and shows you exactly what moves to make to boost your score and get the funding you need.