Here's something nobody warns you about on delivery day.

You sign the paperwork, grab the keys, pull out of the dealership — and by the time you park in your driveway, your brand-new car is already worth less than what you owe on it. That's not an exaggeration. That's just how depreciation works.

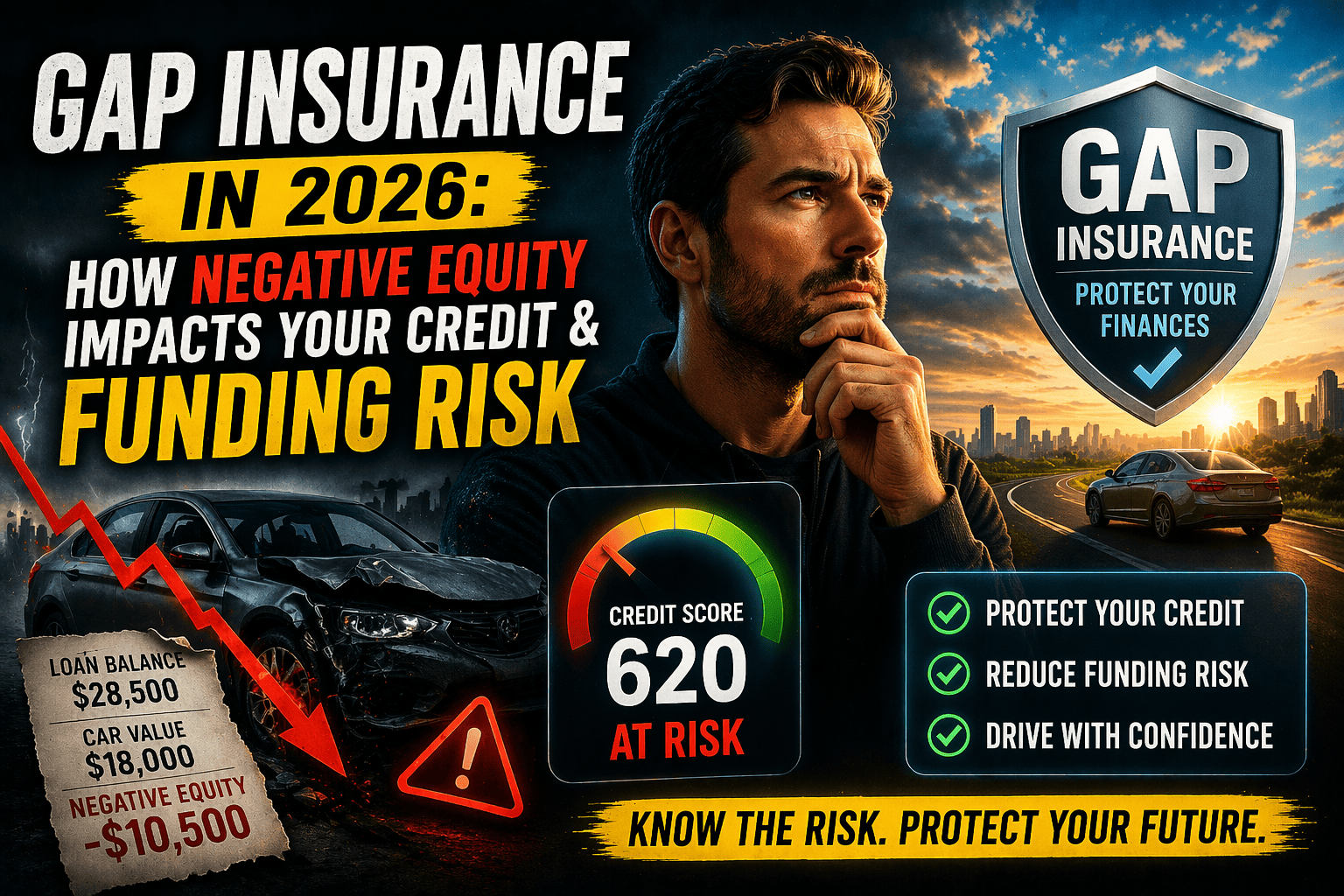

Now imagine three months later, someone runs a red light and totals your car. Your insurance pays what the car is currently worth — not what you still owe the bank. And that difference? That's your problem. Out of pocket. On a car you can't even drive anymore.

That's the gap we're talking about. And in 2026 — with new-car prices still hovering above $50,000, loan terms getting stretched past 60 and 72 months, and interest rates varying wildly by credit tier — this gap is bigger, lasts longer, and affects more borrowers than most people realize.

This isn't a sales pitch for an insurance product. We're breaking down how Guaranteed Asset Protection (GAP) insurance fits into your overall credit risk picture — how it affects your loan structure, what it means for underwriting, and whether having it (or skipping it) actually changes your chances when you go after your next approval.

What GAP Insurance Really Does — And Why Your Lender Pays Attention

At its core, GAP insurance is pretty simple. It covers the difference between your car's actual cash value (ACV) and whatever you still owe on your auto loan if the vehicle gets totaled or stolen. Your regular collision or comprehensive policy only pays what the car is worth right now — not the full loan balance. GAP picks up the rest.

But here's where it gets interesting from a credit and lending standpoint.

If your loan balance is higher than your car's value — and for most people in the first couple years, it is — you're sitting in what's called negative equity. You're "underwater." And in real lending environments, that's a red flag. It tells the lender their collateral (your car) doesn't fully back the loan anymore. The loan-to-value (LTV) ratio has tipped past 100%, and their position is weaker because of it.

Cars lose roughly 20% of their value in the first year alone, then keep dropping 10–15% each year after that. Pair that steep depreciation curve with a long loan — say 72 months at a decent APR — and your loan balance and the car's actual value might not meet in the middle until year three or four. That entire stretch? You're exposed. A total-loss event during that window without GAP means you're writing a check for a car that's sitting in a junkyard.

And if you're planning to apply for more credit down the line — a mortgage, a business loan, a refinance — lenders are going to see that high-LTV auto loan with no protection and read it as unhedged risk. That's not a label you want on your profile.

The 2026 Lending Reality: What the Numbers Actually Look Like

Knowing whether GAP insurance makes sense for you starts with understanding what the lending market looks like right now. So let's get into the actual numbers.

Where Auto Loan Rates Land by Credit Tier in 2026

As of early 2026, the average interest rate on a 60-month new car loan is sitting around 6.98%, per Bankrate's weekly survey. For used cars, it's noticeably steeper — around 11.40% according to Experian's most recent State of the Automotive Finance Market report.

But here's the thing — averages don't tell your story. What really drives your rate (and your GAP risk) is where you fall on the credit spectrum:

-

Super Prime (781+): You're looking at rates as low as 4.88–5.25% on new cars. Folks in this tier usually put 20% or more down and go with shorter terms, so they climb out of negative equity faster. GAP is less urgent here — but on a $55,000+ vehicle, the math can still surprise you.

-

Prime (661–780): This is the biggest chunk of auto borrowers out there. Rates typically land between 5.5–8.5% on new vehicles. Most prime buyers put down 10–15%, which means they're underwater for roughly 18–30 months. That's a real window where GAP earns its keep.

-

Near Prime (601–660): Now we're pushing into 9–14% APR territory. Loan terms get longer, down payments shrink, and the negative equity window can stretch past three years. If there's one credit tier where GAP insurance makes the most obvious difference, it's this one.

-

Subprime (501–600): Rates for new vehicles run 13–15%, and used car rates can blow past 18%. The gap between what you owe and what the car is worth stays wide for a long time. Plenty of subprime lenders actually require GAP coverage before they'll fund the deal.

-

Deep Subprime (Below 500): Rates can clear 20% on used vehicles. Options are thin, terms are tight, and while GAP would help the most here, a lot of standard insurers won't even offer it at this tier.

Monthly Payments and Loan Terms Keep Climbing

The average monthly payment on a new car hit about $748 in Q3 2025 — that's from Experian data reported through LendingTree. Average loan terms have pushed past 68 months, and roughly 34% of all auto loans now run longer than 72 months. The Federal Reserve's consumer credit data backs this up — auto loan debt keeps growing as a share of what households owe overall.

The longer your loan, the longer you're underwater. And the longer you're underwater, the longer GAP coverage actually matters.

Let's Talk About the LTV Problem

Say you finance $45,000 on a car that's technically worth $48,000 after taxes and fees get rolled in. You're already above 100% LTV on day one. Fast forward 12 months — your car might be worth $38,000–$40,000, but your loan balance on a 72-month term at 7% APR? Still hovering around $39,500.

If that car gets totaled during this window, you're on the hook for $1,500–$3,500 on a vehicle you'll never drive again. Without GAP, that money comes straight out of your pocket.

How Your Auto Loan Actually Shows Up on Your Credit Report

This part matters more than most people think. Understanding how your auto loan gets reported to the bureaus helps explain why GAP insurance quietly protects your credit — not just your wallet.

The Basics of Installment Loan Reporting

Your auto loan shows up as an installment account. Every month, your lender sends an update to Equifax, Experian, and TransUnion — your original loan amount, current balance, whether you paid on time, and if anything's gone sideways. All of that feeds into your FICO and VantageScore calculations.

Here's how the pieces connect:

-

Payment History (35% of your FICO score): This is the big one. If a total-loss event leaves you with a deficiency balance you can't pay, that unpaid balance turns into a delinquent installment account on your report. Short of a full charge-off or repossession, it's one of the most damaging marks you can carry.

-

Amounts Owed (30% of FICO): Installment utilization doesn't hit as hard as credit card utilization, but lenders still notice when you owe a high percentage of your original loan amount. It signals you're early in the loan and haven't built any equity yet — and that's a softer spot in your profile.

-

Credit Mix (10% of FICO): A healthy installment loan in good standing actually helps your score. But if a total-loss event turns that account into a charge-off or collection entry, that positive boost flips into a serious drag.

-

How Often It Gets Reported: Most auto lenders update the bureaus every month. After a total loss where the insurance payout falls short, the remaining balance can trigger 30-day, 60-day, and 90-day late marks in quick succession — each one stacking more damage onto your score.

What Happens When There's a Deficiency Balance and No GAP

Here's the chain of events nobody wants to think about:

- Your car gets declared a total loss.

- Your insurer cuts a check for what the car is worth (minus your deductible).

- There's still a balance left on the loan. That's your deficiency.

- You're responsible for paying it directly to the lender.

- If you can't — or don't — the lender starts reporting late payments.

- Eventually, the account gets charged off and potentially sent to collections.

That kind of sequence can tank your credit score by 100 points or more, and it sticks around on your report for up to seven years under FCRA (Fair Credit Reporting Act) guidelines.

GAP insurance takes step 3 off the table entirely. The shortfall gets paid, the loan closes clean, and your credit report stays intact.

How GAP Exposure Can Shift Your Future Funding Odds

Here's where a lot of people miss the bigger picture. Whether you're eyeing a mortgage, shopping for a business line of credit, or looking to refinance something else — lenders don't just look at one account. They look at everything.

The Consumer Financial Protection Bureau (CFPB) emphasizes that auto loan performance directly feeds into broader creditworthiness assessments. An underwater car loan with no protection sitting on your report can absolutely move the needle — in the wrong direction.

Risk Profile Side by Side

| Factor | Stronger Profile | Weaker Profile |

|---|---|---|

| Credit Score | 680+ | Below 600 |

| DTI Ratio | Below 35% | Above 50% |

| Revolving Utilization | Below 30% | Above 70% |

| Auto Loan LTV | Below 90% | Above 120% |

| GAP Coverage | Active | None |

| Loan Term | 48–60 months | 72–84 months |

| Down Payment | 20%+ | 0–5% |

| Deficiency Risk | Minimal | Significant |

Two Borrowers, Same Car — Very Different Outcomes

Borrower A — Has GAP:

She's got a 710 score, finances $42,000 at 6.5% over 60 months with 10% down. Fourteen months in, another driver totals her car. Insurance pays $31,000 (the ACV). She still owes $33,800 on the loan. GAP covers the $2,800 difference. Loan closes at $0. Her credit report shows a paid-in-full installment account. DTI drops. Three months later, she applies for a mortgage and qualifies at a solid rate.

Borrower B — Doesn't Have GAP:

Same score, same car, same accident. But that $2,800 gap? It's all hers. She can't cover it right away. The lender reports a 30-day late, then a 60-day. Her score drops from 710 to around 620. When she applies for that same mortgage, she's now in near-prime territory — facing a higher rate, tighter terms, and she might not even clear the DTI threshold with the deficiency balance dragging things down.

Same person. Same car. Completely different financial trajectory — all because of one coverage decision.

So When Does GAP Insurance Actually Make Sense?

Not every car loan needs GAP coverage. The smart move is to base the decision on your actual risk exposure — not on a dealer's upsell or a blanket "everyone needs it" recommendation.

You Probably Want GAP If:

- You put less than 20% down on the purchase

- Your loan term is longer than 60 months

- You rolled negative equity from a trade-in into your new loan

- Taxes, fees, or dealer add-ons got financed into the loan (pushing your LTV up from the start)

- Your car is a model that depreciates fast

- You're leasing (a lot of lease agreements require it anyway)

- You're in a near-prime or subprime credit tier without a thick financial cushion

You Might Not Need GAP If:

- You put 20%+ down and chose a short loan term (48 months or less)

- Your car holds its value well (certain trucks, SUVs, and specific brands depreciate slower)

- Your loan balance is already at or below what the car's worth today

- You've got enough in savings to comfortably cover a potential shortfall

- You own the car free and clear — no loan at all

Where You Buy It Matters More Than You'd Think

Here's a detail that trips people up: the cost of GAP insurance swings wildly depending on where you get it.

Adding it through your existing auto insurance carrier typically runs $20–$100 per year. That's it. But dealership GAP policies? Those usually land between $400–$800 as a one-time charge that gets baked right into your financing — which means you're paying interest on the GAP premium itself for the entire life of the loan.

From a credit standpoint, buying through your insurer is almost always the better call. It keeps your financed amount lower, starts your LTV in a better spot, and doesn't inflate your monthly payment (or your DTI) the way a dealer-financed policy does.

Myths That Keep Getting People in Trouble

"I have full coverage — that means my loan's covered, right?" This one catches more people than you'd expect. "Full coverage" really just means you have collision plus comprehensive. It pays what the car is worth — not what you owe. Surveys consistently show that most drivers assume their insurance would pay off the full loan after a total loss. It won't. Not even close, in a lot of cases.

"GAP is only a thing for new cars." Not true. New cars do depreciate faster in year one, but if you're financing a used vehicle with a small down payment or a long loan term, you can end up just as underwater. The window might be shorter, but on a high-value used car, the dollar gap can still be thousands.

"My lender will probably just forgive the leftover balance." They don't have to — and most won't. In plenty of states, lenders can legally chase you for the full deficiency through collections, wage garnishment, or court judgment. That balance doesn't just vanish.

"I'll just get GAP later if I need it." By the time you realize you need it, it might be too late. Most insurers only sell GAP coverage within a certain window after you buy the car — usually the first year. Some have model-year or mileage limits too. Wait too long and you could be locked out.

"Accidents are rare — GAP is a waste of money." Maybe. But this isn't about how often it happens. It's about what happens when it does. A single total-loss event without GAP can kick off a credit and financial spiral that takes years to clean up. Good risk assessment isn't just about probability — it's about how bad the downside gets.

Frequently Asked Questions

What exactly does GAP insurance cover?

It pays the difference between your car's actual cash value at the time of a total loss or theft and whatever's still left on your loan or lease. It kicks in after your regular collision or comprehensive coverage does its part — so you're not stuck paying off a car you no longer have.

How does a deficiency balance after a total loss affect my credit?

If your insurance payout doesn't cover the full loan and you can't pay the rest, your lender starts reporting it as delinquent. A single 30-day late mark can shave 60–100 points off your score. A charge-off or collection entry is worse — and stays on your credit report for up to seven years under FCRA rules.

Is GAP coverage legally required?

No state requires it by law. But plenty of lease contracts do — it's built into the terms. Some subprime lenders also make it a condition of funding. Always read the fine print on your loan or lease agreement.

Dealership GAP vs. insurance company GAP — what's the real difference?

Mostly price. Buying through your auto insurer usually costs $20–$100 a year. At the dealership, you're typically looking at $400–$800 rolled into your loan, which means you're paying interest on the GAP fee for the life of the loan. That adds up fast.

How long should I keep GAP coverage?

Until your loan balance drops below your car's market value. For most people with a standard down payment, that takes about 18–36 months. Once your payoff is lower than what the car's worth, you can cancel — and many providers give a prorated refund.

Does buying GAP at the dealership mess with my DTI ratio?

It can. When the dealer rolls it into your loan, your total financed amount goes up — which bumps your monthly payment and, by extension, your DTI. If you add it through your insurer instead, it's just a small bump on your premium and doesn't show up as a separate debt obligation on your credit profile.

Can I get GAP on a used car?

Yes, but it depends on the car's age and mileage. Most insurance companies limit GAP to vehicles within two or three model years and under 30,000 miles. If you're financing a used car with a high LTV, don't wait — shop for GAP early before you age out of eligibility.

The Bottom Line: Think of GAP as Credit Armor

Look, GAP insurance isn't sexy. Nobody gets excited about adding another line item to their car paperwork. But when you zoom out and look at it through a credit risk lens, it starts to make a lot more sense.

It's not just about protecting yourself from a freak accident payout. It's about keeping your installment loan clean on your credit report. It's about making sure a single unlucky event doesn't wreck your DTI, tank your score, and push your next big approval out of reach.

In the 2026 market — where loan balances are at historic highs, terms keep getting longer, and depreciation hasn't slowed down — carrying an underwater auto loan with zero protection is a real, measurable credit exposure. Whether you're working toward a mortgage, building up to a business loan, or just trying to keep your financial foundation solid, understanding how GAP fits into your bigger picture is worth the 10 minutes it takes to evaluate.

Don't make this call based on vibes or whatever the finance manager tells you at the dealership. Run your own numbers. Check your LTV. Know your payoff timeline. Then decide.

Written by: Marcus Whitfield Title: Credit Risk Strategist & Funding Readiness Analyst Experience: 12+ years in fintech credit modeling, auto lending risk assessment, and consumer credit profile analysis

Marcus has spent over a decade helping borrowers and business owners make sense of how everyday lending decisions — things like auto loans, insurance choices, and debt structure — actually show up in underwriting. His analysis pulls from industry frameworks, CFPB and Federal Reserve regulatory guidance, and live lending data from Experian, Equifax, and TransUnion. He believes the best financial decisions start with understanding how the system actually reads your profile.

Disclaimer: This article is for educational purposes only and does not constitute financial, lending, or legal advice. The information here reflects general credit analysis principles and 2026 market conditions. Your individual results depend on your personal credit history, the lender's specific underwriting criteria, and applicable state and federal regulations. Talk to a licensed financial professional for guidance tailored to your situation.

Sources referenced: Experian State of the Automotive Finance Market (Q3 2025), Bankrate Auto Loan Rate Survey (February 2026), Consumer Financial Protection Bureau (CFPB) auto lending reports, Kelley Blue Book depreciation data, Insurance Information Institute GAP coverage guidelines.