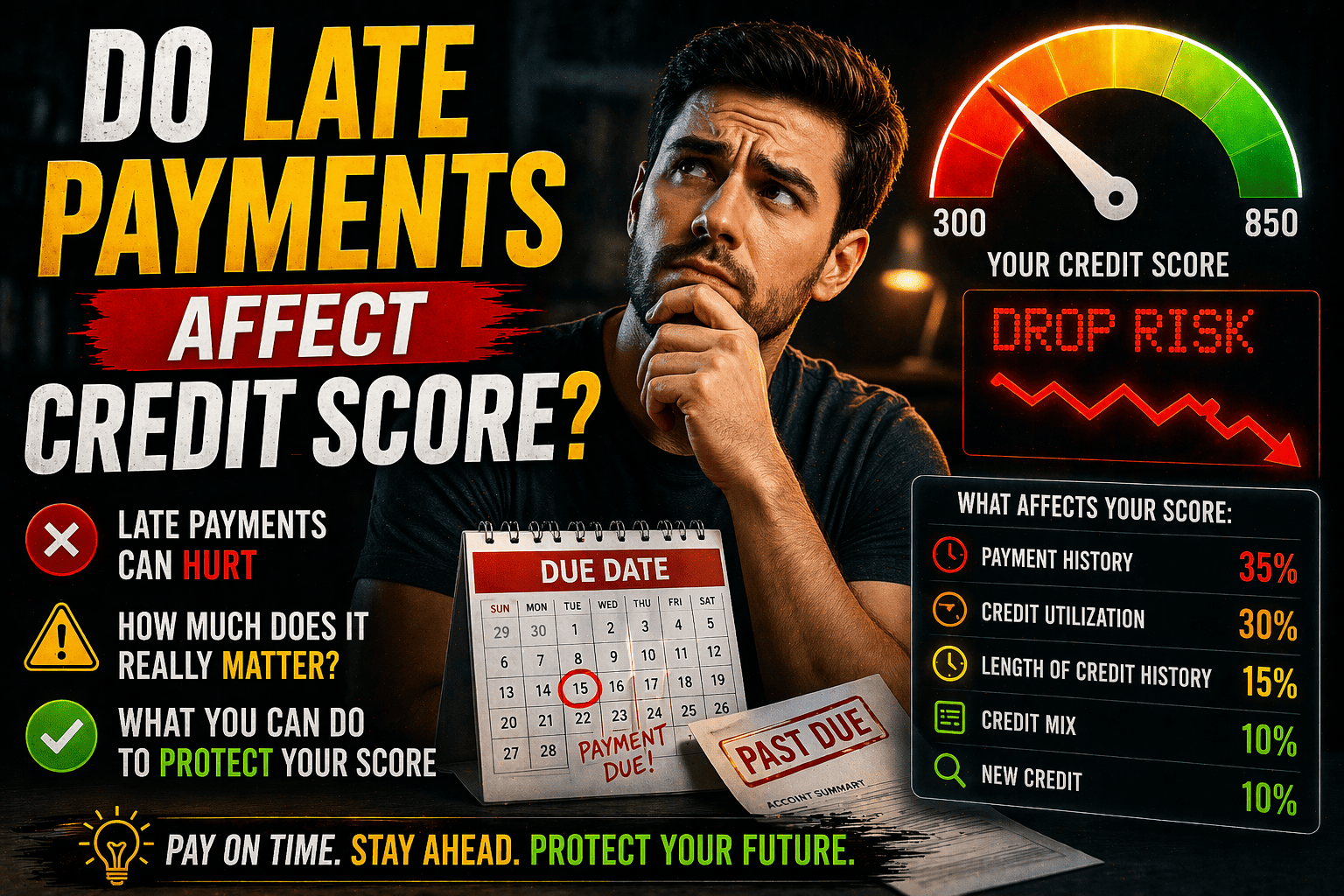

Missed a credit card payment? You might be wondering how much damage one late payment can do. It’s a common fear, and for good reason. Yes, do late payments affect credit score is a question with a clear answer: they absolutely do — but the impact depends on timing and severity. Your payment history is the single most important factor in your credit score, making up 35% of the calculation.

This guide will break down exactly how much a late payment affects your score, how long that negative mark lasts on your credit report, and, most importantly, how to fix it. We'll provide a clear roadmap to help you recover and protect your financial health. For more deep dives into credit and financial wellness, check out our credit education blog.

What Counts as a Late Payment?

We've all had that moment of panic: you realize a bill was due yesterday. While your lender might charge you a late fee, they won't immediately report you to the major credit bureaus—Experian, Equifax, and TransUnion. There’s a grace period.

The real trouble begins when your payment is officially 30 days past due. This is the critical threshold when a creditor is allowed to report the delinquency, causing the first significant damage to your credit score. From there, the negative impact grows with each passing month: a 60-day late payment is more harmful than a 30-day one, and a 90-day late payment is even more destructive.

When does a late payment show up on your credit report?

Many people ask, does a one day late payment affect credit score? The answer is almost always no. Lenders typically wait until an account is a full 30 days delinquent before reporting it. Payments that are 1–29 days late will usually only result in a late fee from your creditor, not a negative mark on your credit report. This gives you a window to correct the mistake before it impacts your score.

As you can see, crossing that 30-day mark is when the real credit damage begins.

How Much Does a Late Payment Affect Credit Score?

This is the crucial question: how much does 1 late payment affect credit score? The impact can be substantial. A single 30-day late payment can cause your score to drop by anywhere from 60 to 110 points.

The exact number depends heavily on your starting credit score. A person with an excellent 800 FICO score could see a drop of 100+ points because the late payment is a significant blemish on an otherwise perfect record. In contrast, someone with a 650 score will still see a drop, but it won't be as drastic because their score already reflects a certain level of risk.

Why a single missed payment hurts more than you think

So, will a 3 day late payment affect my credit score? No, but once you hit 30 days, the damage is severe because payment history accounts for 35% of your FICO score. It's the most heavily weighted factor. Lenders see a late payment as a primary indicator of risk, signaling that you may have trouble managing your financial obligations. A study by Milliman revealed that missing just one mortgage payment can cause an average score drop of over 50 points, which can be a major hurdle during loan preparation.

How Long Does a Late Payment Stay on Credit Report?

Once a late payment is on your report, you're likely wondering, how long does a late payment affect your credit score? According to federal law, a delinquency can remain on your credit report for a full seven years from the original date it was missed.

However, the good news is that its impact diminishes over time. A five-year-old late payment carries far less weight in credit scoring models than one from five months ago. Lenders are always more focused on your recent payment behavior to assess your current creditworthiness.

Can late payments be removed early?

Yes, it's possible in some cases. If the late payment was an isolated incident and you have an otherwise good history with the creditor, you can send a "goodwill letter" politely requesting its removal. Another option is to dispute the late payment if you believe it was reported in error. For more complex situations, credit repair services can help guide you on how to remove late payments from credit report and clean up your credit history.

Do Late Payments on Closed Accounts Affect Credit Score?

It's a common misunderstanding that closing an account erases its history. So, do late payments on closed accounts affect credit score? The answer is a definitive yes.

When you close an account, its payment history is frozen and remains on your credit report. Any late payments associated with that account will continue to be reported for the standard seven years from the original delinquency date. On the flip side, if the account was closed in good standing, its positive payment history can stay on your report for up to 10 years, which is beneficial because closed accounts stay on credit report for 10 years when positive, helping your credit age.

How to Recover After a Late Payment

A late payment is a setback, not a permanent failure. The first and most critical step is to bring the past-due account current to prevent further damage. Once that's done, focus on building a strong defense against future mistakes.

5 ways to improve your credit score after a late payment

Rebuilding your credit requires consistent positive actions. Here are five effective ways to improve credit score after late payment:

- Pay off balances quickly: Lower your credit utilization ratio by paying down credit card balances. This can provide a significant boost to your score.

- Set up autopay: Automate your payments to ensure you never miss a due date again. It's the most reliable way to maintain a perfect payment history.

- Keep old accounts open: The age of your credit accounts is a valuable factor. Closing old accounts can shorten your credit history and lower your score.

- Avoid new hard inquiries: Pause applications for new credit while you're in recovery mode. Each hard inquiry can cause a small, temporary dip in your score.

- Dispute errors if incorrect: Regularly check your credit reports from all three bureaus and dispute any inaccuracies you find immediately.

Expert Tips: How Credit Scoring Models View Late Payments

Different credit scoring models, like FICO and VantageScore, weigh factors differently, but they all place immense importance on payment history. A VantageScore survey found that 68% of consumers understand that even a single late payment can damage their score. You can learn more about these consumer credit trends to see how vital this is.

Why recent late payments hurt more than old ones

Both FICO and VantageScore models are designed to predict future risk, so they give more weight to your recent financial behavior. A late payment that occurred last month is a much stronger indicator of current financial stress than one from five years ago. As a late payment ages, its negative impact fades, being replaced by your more recent, positive payment history. This is why consistency is key to improving your credit readiness.

Conclusion

To recap, do late payments affect credit score? Yes, significantly. A single payment that is 30 days past due can cause a major drop, and the negative mark will stay on your report for seven years. However, recovery is entirely possible.

The impact of a late payment lessens over time, and you are in control of the recovery process. By paying down balances, automating payments, and maintaining good credit habits, you can rebuild your score and prove that a past mistake does not define your financial future.

- Check your credit score now.

- Learn how to remove late payments from your report.

Do Late Payments Affect Your Credit Score?

Late payments can significantly impact your credit score, depending on how late the payment is and how often it happens. Even a single missed payment can lower your score, but the impact grows with time and frequency.

How Late Payments Impact Your Credit Score

Credit bureaus typically report late payments after 30 days past due. Here’s how it breaks down:

- 1–29 days late: Usually not reported but may incur fees.

- 30 days late: Reported to credit bureaus, impacting your score.

- 60–90 days late: Larger hit to your credit score and visible to lenders.

- 120+ days late: Account may go to collections, severely damaging your score.

How to Recover From a Late Payment

If you’ve missed a payment, you can take action to minimize the impact:

- Pay the overdue balance as soon as possible.

- Contact your lender to request removal of the late mark.

- Set up automatic payments to prevent future misses.

How to Remove Late Payments from Credit Report

Follow these steps to dispute or remove late payments from your credit report:

- Get a copy of your credit report from all three bureaus.

- Verify the late payment entry.

- Dispute incorrect information with the credit bureau.

- Ask your creditor for a goodwill adjustment if the late mark is accurate.