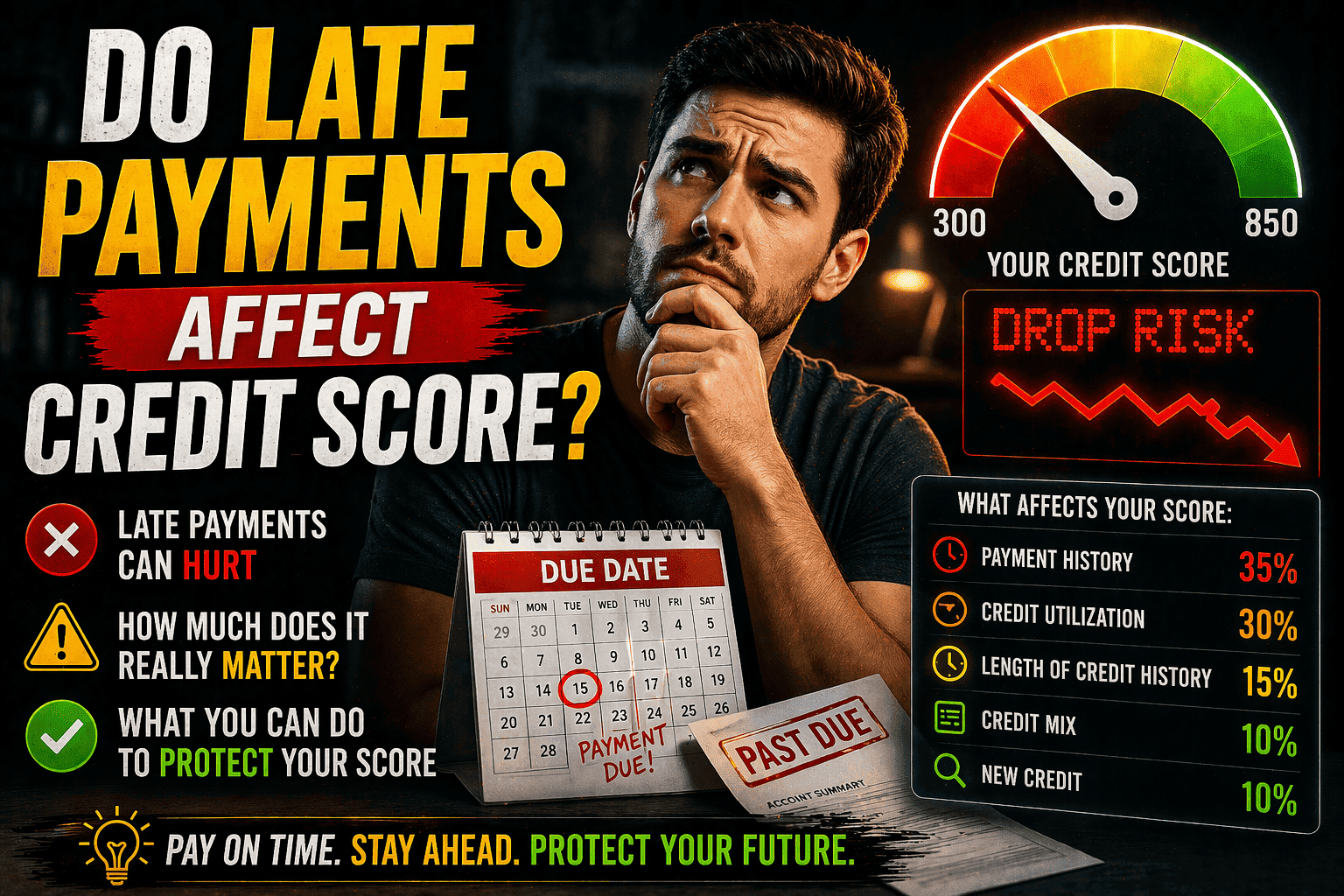

So, do credit repair companies really work? The short answer is yes, but their success hinges on their Experience, Expertise, and Trustworthiness. Their entire purpose is to find and dispute inaccurate, incomplete, or unverifiable information on your credit report. They have no legal power to remove legitimate negative items, like a late payment you actually made. Their effectiveness comes from navigating a complex legal system on your behalf.

1. Understanding Credit Repair: What These Companies Actually Do

To understand if these services are worthwhile, we need to look past the marketing and see what's happening behind the scenes. Think of a reputable credit repair company as a professional advocate whose Expertise is the world of credit reporting. They aren't erasing your history; they're masters of a specific, legally defined process focused on credit health recovery.

1.1 The Core Services Credit Repair Companies Provide

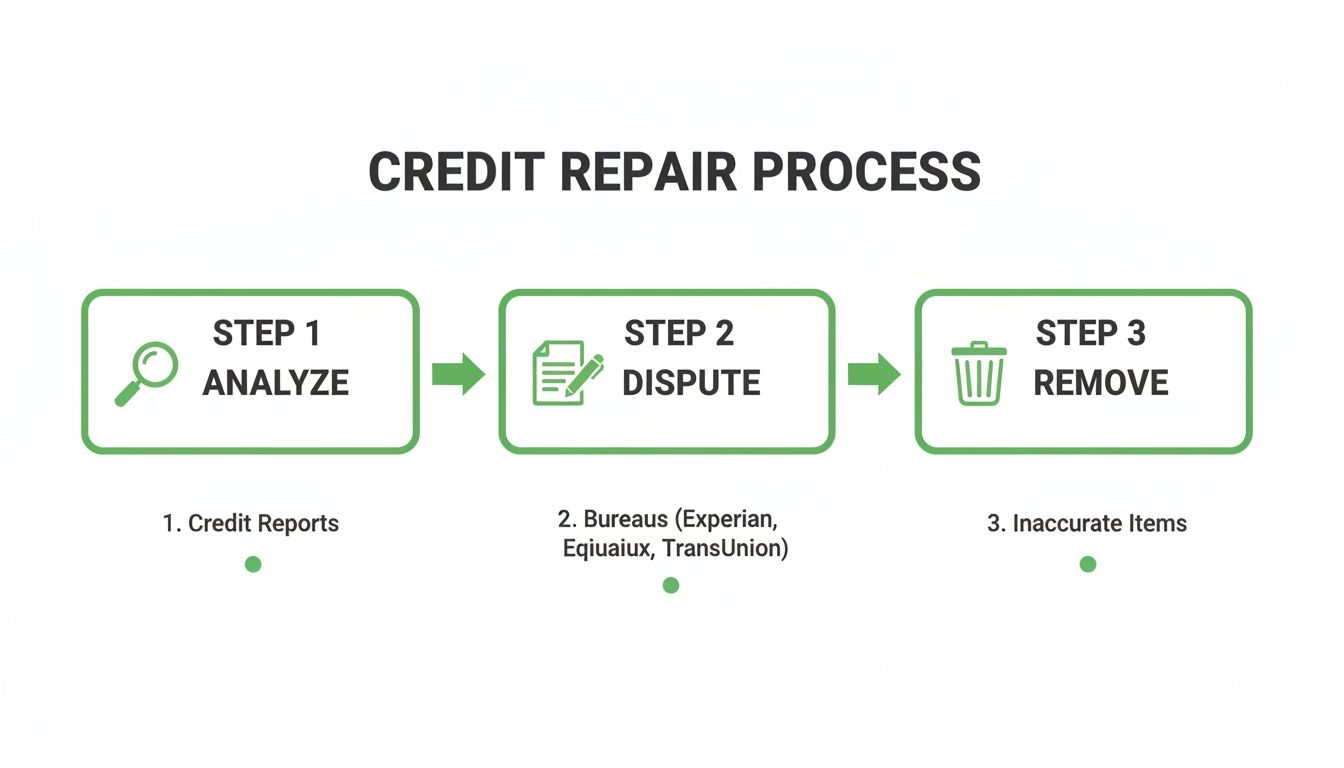

The daily work of these firms is systematic and built on Experience. It begins with obtaining your credit reports from all three major bureaus—Experian, Equifax, and TransUnion—and meticulously combing through them to identify discrepancies.

Once potential errors are flagged, their primary services kick in:

- Detailed credit report analysis and error identification: They use their Expertise to spot mistakes, outdated information, or entries that cannot be substantiated.

- Dispute letter preparation and submission to credit bureaus: They draft and send formal credit bureau disputes, referencing specific consumer protection laws to challenge inaccuracies. This demonstrates their Authoritativeness in legal matters.

- Communication with creditors and collection agencies on behalf of clients: They handle the persistent follow-up required to force creditors to validate the debts they claim you owe, a key part of debt management.

This infographic breaks down the fundamental workflow that every legitimate company uses.

This simple three-step method—Analyze, Dispute, Remove—is the engine that drives any real credit recovery effort. It’s methodical, not miraculous.

1.2 The Legal Framework Behind Credit Repair Services

These companies operate within a strict legal framework, not a gray area. Their entire business model is built on consumer rights established by federal law, which lends them Authoritativeness.

- Rights established under the Fair Credit Reporting Act (FCRA): This foundational law guarantees your right to an accurate credit report, forming the basis for all credit report correction.

- Credit Repair Organizations Act (CROA) regulations and consumer protections: CROA dictates how these companies must operate, making it illegal to charge upfront fees or make false promises. This law ensures their Trustworthiness.

- State-level licensing requirements and compliance standards: Many states add another layer of oversight, requiring companies to be licensed and compliant with local regulations.

1.3 How Credit Repair Differs from DIY Credit Improvement

While you have the right to dispute errors yourself, the difference between DIY and professional help comes down to Expertise and efficiency. Professionals have extensive Experience with the nuances of the system.

- Professional knowledge of dispute processes and documentation requirements: They know precisely what evidence is needed for different types of disputes and how to present it effectively.

- Systematic approach to addressing multiple credit issues simultaneously: Their Experience allows them to manage multiple disputes across all three bureaus at once, a task that can overwhelm an individual.

- Time investment comparison between self-repair and professional services: You're paying for convenience and specialized knowledge, which can be invaluable if your situation is complex or you lack the time to become an expert yourself in legal credit repair methods.

2. When Credit Repair Companies Can Be Effective

Credit repair isn't a solution for every financial problem. However, in certain overwhelming situations, professional intervention can be a game-changer for your financial reputation repair. The real value of their Expertise shines when you're facing a complex mess on your credit reports.

2.1 Scenarios Where Professional Help Shows Real Results

A reputable company earns its fee by tackling challenges that require deep knowledge and persistence. Their Experience is your greatest asset in these scenarios:

- Complex cases involving multiple inaccurate entries across different bureaus: When errors are widespread, a coordinated, multi-front attack is necessary for effective credit report correction.

- Identity theft recovery requiring extensive documentation and follow-up: This is a full-time job involving police reports, affidavits, and relentless communication with creditors. A professional’s Expertise is critical.

- Outdated information that creditors have failed to update or remove: Professionals know how to hold creditors accountable for reporting old, expired negative information.

2.2 Types of Credit Issues That Respond Well to Professional Intervention

While no one can legally erase accurate debt, the legal credit repair methods used by trustworthy firms are highly effective against data errors.

- Reporting errors such as incorrect payment histories or account statuses: These are the most common targets for credit bureau disputes.

- Duplicate accounts appearing multiple times on credit reports: A professional can quickly identify and challenge these duplicates.

- Accounts that should have aged off reports but remain visible: The Experience of a good company ensures these are removed according to legal timelines.

2.3 The Timeline and Realistic Expectations for Success

Managing expectations is key to understanding credit counseling effectiveness. Federal law gives credit bureaus 30 days to investigate a dispute, but a significant credit score improvement won't happen overnight.

- Typical duration for seeing initial results from dispute processes: You might see the first corrections within 30-45 days.

- Factors that influence how quickly improvements appear: The number of disputes and the responsiveness of creditors will affect the timeline. Meaningful, lasting change often takes three to six months.

- Measuring success beyond just credit score increases: True success is achieving a clean, accurate credit report. This is what truly rebuilds your financial reputation and is a core part of credit rebuilding services.

3. Limitations and When Credit Repair Falls Short

Before signing up, it's crucial to understand the limits of these services. Their Authoritativeness is strictly confined to challenging inaccurate information; they cannot legally erase your actual financial history. Recognizing this is key to setting realistic goals and avoiding scams.

3.1 Legitimate Negative Items That Cannot Be Removed

A company's Trustworthiness is demonstrated by being honest about what they cannot do. If a negative mark on your report is accurate and within the legal reporting time limit (usually seven years), it is there to stay.

- Accurate late payments, defaults, and charge-offs that correctly reflect your payment history.

- Bankruptcy, foreclosure, and tax lien records that are correctly reported public records.

- Court judgments and other public records that reflect actual events.

Any company claiming they can remove these is not using legal credit repair methods and is likely breaking the law.

3.2 Situations Where DIY Approaches Are More Appropriate

Not every issue requires professional intervention. Sometimes, handling a credit report correction yourself is the smarter, more cost-effective route.

- Simple errors that require basic dispute letters and minimal follow-up, like a misspelled name or an old address.

- Single-issue problems that don't justify ongoing service fees, where one dispute can resolve the problem.

- Cases where consumers have adequate time and organizational skills to manage the process themselves.

3.3 Common Overselling and Unrealistic Promises to Watch For

If a company's pitch sounds too good to be true, it is. Scammers prey on desperation with promises they cannot legally keep, undermining the Trustworthiness of the entire industry.

- Guarantees of specific credit score improvements within unrealistic timeframes.

- Claims about removing accurate negative information permanently.

- Pressure tactics and upfront fee structures that violate federal regulations.

The CROA explicitly prohibits such deceptive claims. Real debt management and financial reputation repair are about accuracy, not magic.

4. Evaluating Costs Versus Benefits

Is paying for credit repair worth the money? It's a classic cost-benefit analysis. You must weigh the fees against the long-term financial advantages of a better credit score.

4.1 Typical Pricing Models and Fee Structures

Understanding how companies charge is the first step. The two most common models are:

- Monthly subscription services and their associated ongoing costs: Typically ranging from $79 to $149 per month, this is the most common model.

- Pay-per-deletion models and potential long-term financial implications: You pay a fee for each item successfully removed. This can become expensive if you have numerous errors.

- Setup fees, consultation charges, and additional service costs: Be aware of one-time fees, which can range from $99 to $195.

4.2 Calculating the Real Return on Investment

The true benefit of credit score improvement isn't just a higher number; it's tangible savings and increased opportunities.

- Potential savings from improved loan terms and interest rates: A better score can save you thousands on mortgages and auto loans.

- Credit score improvements and their impact on insurance premiums: Many insurers use credit-based scores to set rates.

- Employment and housing opportunities that may improve with better credit: A clean report can be a deciding factor for landlords and some employers.

4.3 Hidden Costs and Long-term Financial Considerations

While the upside is significant, you must also consider the drawbacks.

- Opportunity cost of monthly fees over extended service periods: Money spent on fees could be used to pay down debt, which also improves your score.

- Potential for dependency on ongoing professional services: The goal should be a short-term fix, not a lifelong subscription.

- Alternative uses for money spent on credit repair services: Consider whether that money is better spent on debt management strategies or building an emergency fund.

5. How to Choose a Reputable Credit Repair Company

Finding the right partner is the most critical step. Your success hinges on your ability to see through hype, spot red flags, and ask the right questions to verify a company's Experience, Expertise, Authoritativeness, and Trustworthiness.

5.1 Red Flags and Warning Signs to Avoid

Some companies are out to make a quick buck using shady, illegal tactics. Learning to spot these warning signs is your first line of defense.

- Companies requiring upfront payments before providing any services: The CROA forbids this. If they ask for money before doing any work, walk away.

- Unrealistic promises about guaranteed results or score improvements: No legitimate company can guarantee a specific outcome. This is a dead giveaway of a scam.

- Lack of transparency about pricing, processes, or consumer rights: A company lacking Trustworthiness will be vague about their contract and your rights.

5.2 Essential Questions to Ask Before Signing Up

Once you've weeded out the obvious scams, dig deeper. A company's answers will reveal their Expertise and legitimacy.

- Specific services included in monthly fees and what costs extra? Get clarity to avoid surprise charges.

- Company track record, success rates, and client testimonials? This provides proof of their Experience and performance.

- Cancellation policies, money-back guarantees, and contract terms? You should be able to cancel without a major penalty.

5.3 Verification Steps for Company Legitimacy

Finally, do your own independent research to confirm a company's Authoritativeness and credentials.

- Better Business Bureau ratings and complaint resolution history: How a company responds to complaints speaks volumes about its Trustworthiness.

- State licensing verification and regulatory compliance records: Check with your state attorney general to ensure they are operating legally.

- Professional certifications and industry association memberships: Affiliation with groups like the National Association of Credit Services Organizations (NACSO) shows a commitment to ethical standards.

Summary

Credit repair companies can provide genuine value for consumers dealing with complex credit report errors, identity theft, or situations requiring extensive documentation and follow-up. However, their effectiveness is limited to addressing inaccurate or unverifiable information—they cannot remove legitimate negative items or guarantee specific score improvements. Success depends largely on the individual's credit situation, the company's expertise and ethics, and realistic expectations about outcomes and timelines. For simple errors or single issues, DIY credit repair often proves more cost-effective, while complex cases may justify professional intervention despite the associated costs.

Frequently Asked Questions

Q: Can credit repair companies remove accurate negative information from my credit report?

A: No, legitimate credit repair companies cannot remove accurate negative information. Their Expertise lies in disputing inaccurate, incomplete, or unverifiable items. Any company promising to remove accurate negative information is likely operating illegally and lacks Trustworthiness.

Q: How long does it typically take to see results from a credit repair service?

A: Initial results from credit bureau disputes may appear within 30-45 days, as bureaus must investigate within 30 days. However, significant credit score improvement often takes 3-6 months or longer, depending on the complexity of the credit health recovery process.

Q: Is it better to repair credit myself or hire a professional company?

A: This depends on your situation's complexity, time, and organizational skills. Simple errors are often best handled personally. Complex cases involving multiple bureaus or identity theft may benefit from the Experience and Authoritativeness of professional credit rebuilding services.

Q: What should I expect to pay for credit repair services?

A: Monthly fees for credit rebuilding services typically range from $79 to $149, with some companies charging setup fees of $99 to $195. Pay-per-deletion services may charge $50 to $150 per successfully removed item. Always avoid companies requiring large upfront payments.

Q: Are there any guarantees with credit repair services?

A: Reputable companies cannot guarantee specific credit score improvements or promise to remove accurate information. Their Trustworthiness is shown by guaranteeing they will follow proper dispute procedures and may offer money-back guarantees if no progress is made within a specified timeframe.

Tired of guessing what's holding your credit back? Before you pay for repairs or apply for funding, get a clear, AI-powered blueprint. Score Machine analyzes your credit report in seconds, flagging errors, revealing fundability, and giving you an actionable plan. Stop wondering and start knowing. Get your instant credit analysis at https://thescoremachine.c