7 Best Credit Cards for Bad to Fair Credit in 2026: A Complete Guide

Navigating the credit card market with a bad to fair credit score can feel like a maze of high fees and instant denials. The right card, however, isn't just a spending tool; it's a strategic asset for rebuilding your financial health and unlocking future opportunities, from mortgages to business funding. Many applicants face rejection because they apply without a clear strategy, accumulating unnecessary hard inquiries that further damage their scores. The key is to shift from hopeful guessing to informed action.

This comprehensive guide is designed to provide that clarity. We will break down the best credit cards for bad to fair credit, moving beyond generic lists to offer actionable insights. You will learn the critical differences between secured and unsecured cards, how to interpret complex terms like APRs and fees, and which cards align with specific financial goals.

Crucially, we'll explain how to prepare your credit profile before you apply to maximize your approval odds. For entrepreneurs and funding companies, understanding this pre-application stage is vital. Using a tool like Score Machine to analyze your credit report first can significantly increase funding approvals by identifying and addressing underwriting red flags before a lender ever sees them. This guide provides a clear roadmap, transforming a stressful application process into a confident step toward building a stronger financial future.

1. NerdWallet

NerdWallet is a top-tier financial resource hub, particularly valuable for those searching for the best credit cards for bad to fair credit. Instead of being a card issuer, it acts as a comprehensive editorial guide. Its team of finance experts researches, reviews, and compares hundreds of financial products, presenting their findings in easy-to-digest roundup articles and comparison tools.

This platform is ideal for users who feel overwhelmed by the sheer number of credit card options and need trusted guidance to narrow down their choices. It simplifies the complex world of credit by organizing cards into specific categories, such as "Best Secured Cards" or "Cards for Fair Credit," allowing you to focus only on products you're likely to qualify for.

Why It Stands Out

What makes NerdWallet a must-visit resource is its commitment to detailed, unbiased comparisons. The platform uses a consistent evaluation framework for each card, covering critical factors like annual fees, APRs, security deposit requirements, and potential paths to "graduate" to an unsecured card. This structured approach lets you quickly see how different cards stack up against each other side-by-side.

Key Insight: NerdWallet's expert commentary often highlights hidden perks or potential pitfalls that aren't immediately obvious on a card issuer's website, such as a history of reporting to all three credit bureaus or a lack of rewards.

The user interface is clean and intuitive. You can filter options based on your specific needs, like finding a card with no annual fee or one that offers cash back rewards. Once you find a suitable card, NerdWallet provides a direct "Apply Now" link, streamlining the process.

How to Use NerdWallet Effectively

- Start with the Right Category: Navigate directly to their pages for "Bad Credit" or "Fair Credit." This pre-filters the selection to cards designed for your credit profile.

- Use the Comparison Tools: Pay close attention to the side-by-side tables. Focus on the annual fee, regular APR, and any specific credit-building features mentioned.

- Read the Full Review: Don't just look at the summary. Click through to the full review of a card you're considering. This is where you'll find expert analysis on who the card is truly best for.

- Check for Prequalification Links: NerdWallet often notes if an issuer offers a prequalification tool. Using it can show you your approval odds without a hard inquiry on your credit report.

Key Details & Access

- Pricing: Free to use. NerdWallet earns commissions from its partners when a user is approved for a product, which can influence placement.

- Pros: Trusted editorial reviews, powerful filtering and comparison tools, direct application links.

- Cons: Affiliate relationships may affect which cards are featured most prominently. Always verify rates and terms on the issuer's official site.

While NerdWallet excels at comparing cards with standard features, some consumers may be looking for specific introductory offers. For more information on promotional rates, which are less common but still available on certain cards, you can explore these 0% interest credit card options.

Website: https://www.nerdwallet.com/credit-cards/best/bad-credit

2. Credit Karma

Credit Karma is a powerful, free platform that gives users personalized insights into their credit health. Instead of just offering articles, it provides a tailored experience based on your actual credit profile, making it a crucial tool when searching for the best credit cards for bad to fair credit. By monitoring your VantageScore 3.0 from TransUnion and Equifax, it helps you understand where you stand and then matches you with credit card offers you have a higher probability of qualifying for.

The platform is designed for individuals who want to take an active role in their credit journey. It demystifies the credit-building process by showing you not only your score but also the factors influencing it, such as payment history and credit utilization. For those with damaged credit, this direct feedback loop is invaluable for making targeted improvements while simultaneously shopping for appropriate financial products.

Why It Stands Out

The key differentiator for Credit Karma is its "Approval Odds" feature. Before you submit an application that results in a hard inquiry, the platform uses your credit data to estimate your chances of being approved for specific cards. This soft-pull matching system can save you from applying for cards you are unlikely to get, thereby protecting your credit score from unnecessary dings that can hinder your progress.

Key Insight: Credit Karma's score simulator is a standout tool. It allows you to see the potential impact of financial decisions-like paying down debt or applying for a new card-before you make them, providing a risk-free way to strategize your credit-building efforts.

The user interface is built around your personal dashboard, making it easy to track score changes over time and receive alerts for significant activity on your reports. This constant monitoring helps you stay on top of your financial health and spot potential issues quickly.

How to Use Credit Karma Effectively

- Create Your Free Account: Sign up and provide the necessary information to pull your credit reports and scores. This process does not impact your credit.

- Review Your Credit Factors: Before looking at cards, examine the "Credit Factors" section. Understand what's helping and hurting your score so you can focus your improvement efforts.

- Browse Personalized Offers: Navigate to the credit card section to see recommendations tailored to your profile. Pay close attention to the "Approval Odds" (e.g., Outstanding, Very Good, Good) for each card.

- Filter by Your Goals: Use the filters to find cards specifically designed for "Building Credit." You can further narrow the results by features like "no annual fee" or "secured card" to match your needs.

Key Details & Access

- Pricing: Free to use. Credit Karma is compensated by lenders when users are approved for offers found on the site.

- Pros: Personalized card matches with approval odds, helps avoid unnecessary hard inquiries, excellent tools for tracking credit progress and simulating score changes.

- Cons: Approval odds are only an estimate and not a guarantee. Recommendations are influenced by advertising partnerships.

For businesses in the funding space, leveraging a client's improved credit profile is key. As clients use platforms like Credit Karma to build their scores, they become better candidates for funding. Integrating a tool like Score Machine can streamline the underwriting process, allowing a funding company to quickly analyze these improved credit reports and increase their funding volume by identifying more qualified applicants.

Website: https://www.creditkarma.com/credit-cards

3. Bankrate

Bankrate is a long-standing authority in personal finance, offering a robust platform for comparing the best credit cards for bad to fair credit. Like a seasoned financial journalist, Bankrate provides in-depth analysis, editor picks, and clear snapshots of current rates and fees. It serves as a trusted guide, especially for consumers cautious about predatory offers and high-fee cards that often target this demographic.

The platform is designed for users who want more than just a list; they want a clear methodology and expert vetting. By separating its resources into dedicated hubs for "bad credit" and "fair credit," Bankrate helps you concentrate your search on financial products that are realistically within reach, saving you time and preventing unnecessary application denials.

Why It Stands Out

Bankrate's commitment to transparency is its key differentiator. The platform clearly explains its evaluation methodology, giving users confidence in its recommendations. Its editors frequently publish deep dives into specific cards, exploring crucial details like security deposit requirements, potential paths to graduate to an unsecured card, and the long-term value of building credit with a particular product.

A significant advantage is Bankrate's proactive warnings about predatory cards. They often call out products with excessive upfront fees or confusing terms, steering users toward safer, more constructive credit-building options. This editorial oversight is invaluable for consumers who may not yet be able to spot the red flags of a bad financial product.

Key Insight: Bankrate excels at providing a quick, at-a-glance snapshot of a card's most critical numbers, such as the purchase APR and annual fee, directly in its comparison tables, making it incredibly efficient for initial screening.

The user interface is professional and data-driven. While navigation can sometimes lead to multiple subpages, the core comparison tools are straightforward, presenting a healthy mix of secured cards and carefully vetted unsecured options. This balance helps users see the full spectrum of available products.

How to Use Bankrate Effectively

- Select the Correct Hub: Start by choosing either the "Best for Bad Credit" or "Best for Fair/Average Credit" section from their main credit card menu to ensure you're viewing appropriate offers.

- Review Editor's Picks: Pay close attention to the cards designated as "Editor's Picks." These are often highlighted because they offer superior features, such as a clear graduation path or no annual fee.

- Scrutinize the Fee Snapshots: Use the comparison tables to quickly rule out cards with high annual fees or other setup costs. Focus on the regular APR to understand the long-term cost of carrying a balance.

- Read the Cautions: If Bankrate includes a warning or a specific caution about a card, take it seriously. This expert guidance can help you avoid costly mistakes.

Key Details & Access

- Pricing: Free for consumers. Bankrate may receive compensation from its partners when a user applies and is approved for a card.

- Pros: Reputable publisher with regularly updated information, strong focus on methodology and transparency, clear warnings against predatory products.

- Cons: Navigation can sometimes feel layered, and promoted partner offers may be featured prominently. Always confirm the final terms on the card issuer's website.

Bankrate is excellent for getting a vetted overview, but to maximize your approval odds, it's wise to know your credit standing inside and out. For funding companies aiming to increase approval rates for their clients, integrating a tool like Score Machine can provide the detailed credit analysis needed to match applicants with the right products confidently.

Website: https://www.bankrate.com/credit-cards/bad-credit/best-for-bad-credit/

4. WalletHub

WalletHub positions itself as a data-driven personal finance resource, making it an excellent stop for anyone researching the best credit cards for bad to fair credit. Unlike purely editorial sites, WalletHub integrates extensive card data with aggregated user reviews, offering a unique blend of expert analysis and real-world consumer feedback. The platform's goal is to provide a 360-degree view of financial products, empowering users to make informed decisions.

This site is particularly useful for individuals who want to dig into the numbers behind each credit card. It excels at presenting granular details like specific APR ranges, minimum security deposit amounts, and all associated fees in a clear, upfront manner. This data-first approach helps you move beyond marketing claims and evaluate cards based on their true costs and terms.

Why It Stands Out

What truly distinguishes WalletHub is its incorporation of community input. Each card profile features a score based on aggregated user reviews, providing a layer of social proof that complements the editor's rating. This allows you to see how actual cardholders feel about customer service, the mobile app, and the day-to-day experience of using the card, which is often missing from standard reviews.

Key Insight: WalletHub’s user reviews often reveal practical issues or benefits, such as how quickly a security deposit is refunded or the average credit score of approved applicants, giving you a crowdsourced glimpse into your approval odds.

The platform also maintains monthly updated rankings for various credit card categories, ensuring the information is timely and reflective of current offers. Its detailed card pages are packed with data points, and the integrated "WalletAnswers" Q&A section provides expert responses to common credit-rebuilding questions, making it a comprehensive learning tool.

How to Use WalletHub Effectively

- Check the Monthly Rankings: Start with their list of "Best Credit Cards for Bad Credit." Since this is updated regularly, you’ll see the most current top-rated options.

- Scrutinize the Card Details: On a card's dedicated page, expand all sections. Pay close attention to the "Rates & Fees" table and compare it directly with other cards you are considering.

- Read User Reviews: Don't skip the user reviews section. Filter by "most recent" to get a current perspective on the cardholder experience. Look for patterns in complaints or praise.

- Use the Q&A Section: If you have a specific question about a card or a credit-rebuilding strategy, browse the WalletAnswers section. It's likely another user has already asked it and received a detailed reply from a financial expert.

Key Details & Access

- Pricing: Free to use. WalletHub, like other comparison sites, is compensated by financial partners.

- Pros: In-depth data on fees and deposits, user reviews provide real-world context, regularly updated card rankings.

- Cons: Includes some high-fee subprime unsecured cards that require careful scrutiny. The extensive amount of data on a single page can sometimes feel overwhelming.

For funding companies aiming to increase their approval volume, understanding a client's full credit profile is crucial. Utilizing a tool like Score Machine before directing clients to apply through platforms like WalletHub can significantly enhance funding outcomes by ensuring applicants are matched with the most suitable products from the start.

Website: https://wallethub.com/credit-cards/bad-credit/

5. Capital One (Fair and Building Credit pages)

Capital One is a major card issuer that provides a direct and accessible pathway for consumers searching for the best credit cards for bad to fair credit. Unlike comparison sites, Capital One's dedicated "Fair and Building Credit" pages act as a curated portal to its own starter products. This makes it an excellent destination for applicants who prefer to deal directly with a well-known, reputable bank.

The platform is specifically designed for individuals who are actively rebuilding their credit or just starting out. It clearly separates its offerings, showcasing secured cards that help establish positive payment history and unsecured cards for those with fair credit who are ready for more traditional options. This direct approach removes the guesswork of navigating a massive portfolio of cards meant for excellent credit.

Why It Stands Out

Capital One's most significant advantage is its pre-approval tool. This feature allows you to see which of its credit cards you are likely to qualify for with only a soft credit inquiry, which does not impact your credit score. This is a game-changer for credit-builders who want to avoid the negative impact of a hard inquiry from a denied application. The process provides clarity and confidence before you formally apply.

Key Insight: The pre-approval process isn't just a yes or no; it often presents you with specific card offers, including potential credit limits and APRs, giving you a transparent preview of the terms you can expect.

Furthermore, Capital One offers a clear upgrade path. Many users with secured cards report being automatically reviewed for graduation to an unsecured card after demonstrating responsible use. The platform also includes free access to CreditWise, a tool that helps you monitor your VantageScore 3.0 from TransUnion and understand the factors affecting your credit.

How to Use Capital One Effectively

- Use the Pre-Approval Tool First: Always start with the "See If You're Pre-Approved" feature on their fair and building credit page. This is the safest way to gauge your eligibility.

- Compare Your Offers: If you are pre-approved for multiple cards, compare them carefully. A card like the Platinum Secured requires a deposit, while the QuicksilverOne offers rewards but has an annual fee. Choose the one that best fits your financial situation.

- Understand Secured Deposit Options: For the Platinum Secured Mastercard, Capital One may offer you a lower minimum deposit ($49, $99, or $200) for a $200 credit line based on your creditworthiness.

- Leverage CreditWise: Once you become a cardholder, use the free CreditWise tool to track your progress and learn what actions are helping or hurting your score.

Key Details & Access

- Pricing: Card fees vary. The Platinum Secured card has no annual fee, while the QuicksilverOne for Fair Credit has a $39 annual fee. APRs are typically high, reflecting the associated risk.

- Pros: Reputable major issuer, excellent pre-approval tool (soft pull), clear upgrade paths, and free credit monitoring with CreditWise.

- Cons: Unsecured options for fair credit may come with an annual fee, and regular APRs can be very high.

Going through the pre-approval process with a major issuer like Capital One can be a crucial step in a larger financial plan. For those aiming to secure significant funding in the future, understanding your credit standing is essential. You can discover more about comprehensive loan preparation to ensure your credit profile is as strong as possible.

Website: https://www.capitalone.com/credit-cards/fair-and-building/

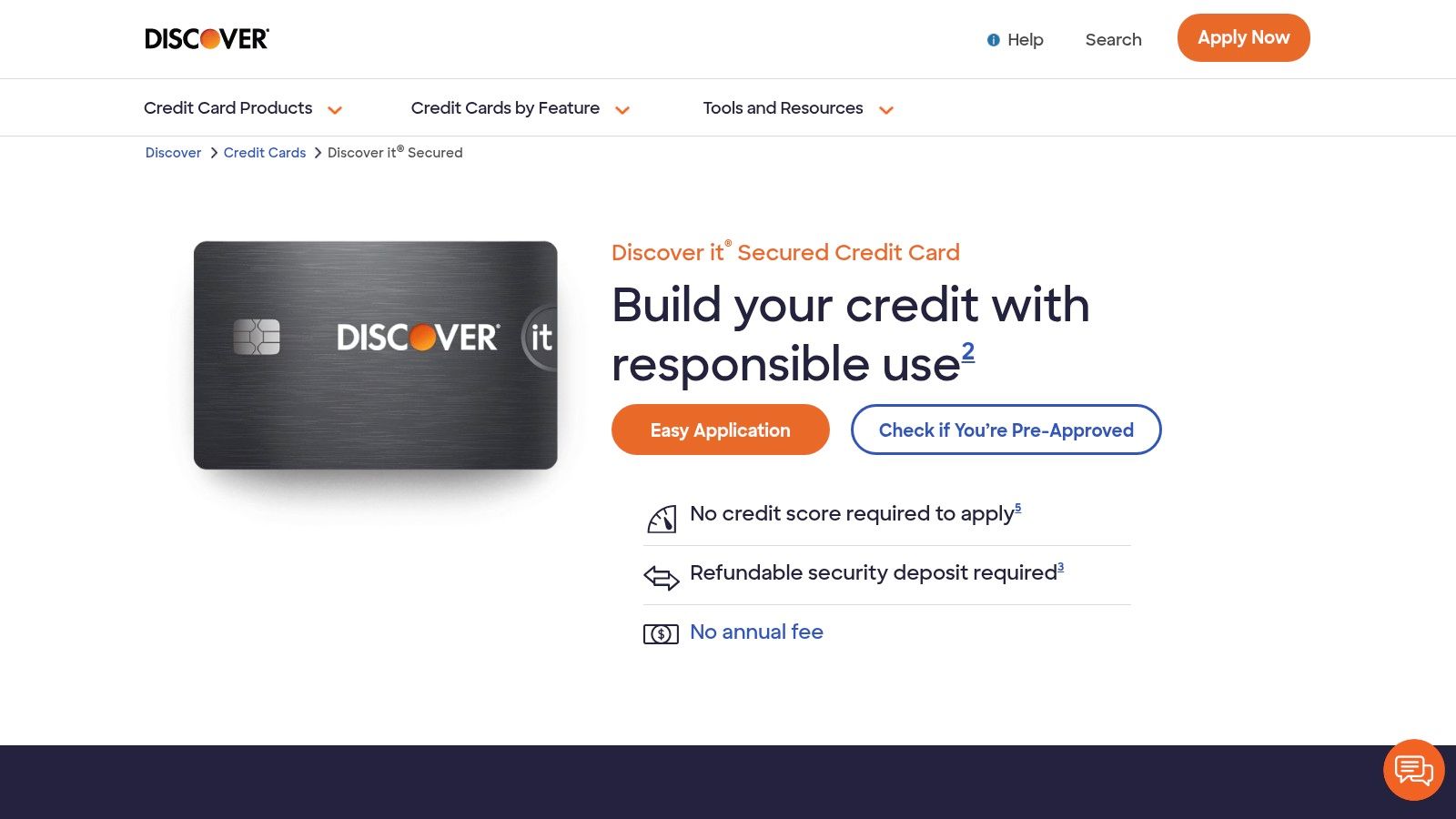

6. Discover (Discover it® Secured Credit Card)

Discover's official website is a direct gateway to one of the most highly-regarded best credit cards for bad to fair credit: the Discover it® Secured Credit Card. Unlike comparison sites, going directly to Discover provides authoritative information straight from the issuer. It allows you to explore the card's features, terms, and conditions without third-party interpretation, making it a crucial stop for serious applicants.

The platform is designed for individuals who are ready to take a significant step in rebuilding their credit with a reputable issuer. It clearly outlines how the secured card works, from funding the initial refundable deposit to its potential for graduating to an unsecured card. This direct-to-issuer approach is ideal for those who have completed their research and are prepared to apply.

Why It Stands Out

What makes the Discover it® Secured Credit Card a standout choice is its rare combination of credit-building tools and genuine rewards on a single platform. The website highlights its $0 annual fee and the ability to earn cash back, features typically reserved for those with good credit. You earn 2% cash back at gas stations and restaurants on up to $1,000 in combined purchases each quarter, plus 1% on all other purchases.

Discover also offers an unlimited Cashback Match at the end of your first year, doubling all the rewards you've earned. This unique benefit provides a powerful incentive to use the card responsibly while rebuilding your credit profile. The website also emphasizes that Discover reports to all three major credit bureaus, which is essential for comprehensive credit building.

Key Insight: Discover's commitment to graduation is a major differentiator. The site explains that automatic reviews begin after seven months, offering a clear and tangible pathway to an unsecured card and the return of your security deposit.

How to Use the Discover Website Effectively

- Review the Secured Card Page: Start on the Discover it® Secured Credit Card landing page. Carefully read the "Card Details," including the APR, fees, and rewards structure.

- Use the Prequalification Tool: Before applying, look for Discover's "Check Now" pre-approval tool. This lets you see if you're likely to be approved with no impact on your credit score.

- Understand the Deposit Process: The site explains that you'll need to provide a refundable security deposit ($200 minimum) which will equal your credit limit. You'll need a bank account to fund this.

- Explore Credit-Building Resources: Discover's site offers more than just applications. It provides free FICO® Score access and educational content to help you monitor and improve your credit health.

Key Details & Access

- Pricing: $0 annual fee. A refundable security deposit is required, starting at $200.

- Pros: Offers cash back rewards and a first-year Cashback Match, no annual fee, and a clear graduation path. Reports to all three credit bureaus.

- Cons: The variable APR can be high, making it crucial to pay the balance in full each month. Requires a bank account to fund the security deposit.

Ensuring your credit profile is strong before applying directly with an issuer like Discover can significantly boost your approval odds. To understand your underwriting risk and overall financial standing, you can learn more about assessing your credit readiness.

Website: https://www.discover.com/credit-cards/secured/

7. OpenSky (Capital Bank) – OpenSky Secured Visa

OpenSky stands out as a direct issuer offering one of the most accessible best credit cards for bad to fair credit, specifically designed for individuals who have been denied elsewhere. The OpenSky Secured Visa is a powerful tool for those with very poor credit or no credit history at all, as its application process removes a major barrier to entry: the hard credit check. This makes it a go-to option for consumers focused purely on building or rebuilding their credit profile without risking another inquiry.

This card is ideal for users who need a guaranteed entry point into the credit system. By requiring a refundable security deposit that sets your credit limit, OpenSky minimizes its risk, allowing it to approve applicants that traditional lenders would turn away. It’s a straightforward, no-frills product aimed at establishing a positive payment history.

Why It Stands Out

The single most compelling feature of the OpenSky Secured Visa is its no credit check application. This is a game-changer for applicants with recent bankruptcies, charge-offs, or extremely low scores who need a fresh start. By eliminating the credit pull, OpenSky makes approval nearly certain as long as you meet basic identity, income, and age requirements.

Furthermore, OpenSky reports your payment activity to all three major credit bureaus (Equifax, Experian, and TransUnion). Consistent, on-time payments will build a positive history across the board, which is essential for improving your credit score. The entry point is also relatively low, with security deposits starting around $200, making it an affordable way to begin your credit journey.

Key Insight: OpenSky is one of the few issuers where approval isn't dependent on your credit past. Its value lies in being a reliable launchpad for credit building when other doors are closed.

The application process is simple and provides a real-time decision, so you know immediately where you stand. While it lacks rewards or perks, its core function is executed perfectly: providing a pathway to better credit for those who need it most.

How to Use OpenSky Effectively

- Fund Your Deposit: Once approved, you must fund your security deposit. This amount becomes your credit limit, so choose a figure you can comfortably afford.

- Make Small, Regular Purchases: Use the card for a small, recurring expense like a streaming subscription or a tank of gas. This keeps the account active.

- Pay in Full, Every Month: The most critical step is to pay your balance in full and on time each month. This demonstrates responsible credit management to the bureaus.

- Monitor Your Credit Reports: Use a tool like Score Machine to track how your on-time OpenSky payments are positively impacting your credit scores across all three bureaus. This helps you see the direct results of your efforts.

Key Details & Access

- Pricing: The OpenSky Secured Visa typically has an annual fee (check the issuer's site for current rates). The security deposit is refundable.

- Pros: No credit check required for application, reports to all three major credit bureaus, low minimum security deposit.

- Cons: Charges an annual fee, does not offer a guaranteed path to "graduate" to an unsecured card.

For funding companies, helping clients secure a card like OpenSky can be a crucial first step. By establishing this initial tradeline, a client's credit file begins to build the positive history necessary for larger funding approvals. This directly increases the company's funding volume and client success rate by turning previously un-fundable applicants into qualified candidates.

Website: https://www.openskycc.com/

Top 7 Cards for Bad-to-Fair Credit

| Item | 🔄 Implementation complexity | 💡 Resource requirements | ⭐ Expected outcomes | 📊 Ideal use cases | ⚡ Key advantages |

|---|---|---|---|---|---|

| NerdWallet | Low — simple browse & filters | No cost; time to read; must verify issuer terms | ⭐⭐⭐ — clear editorial shortlists, not personalized | Researching fees/APR, comparing features, learning graduation paths | Trusted editorial summaries, side‑by‑side comparisons, direct issuer links |

| Credit Karma | Medium — create free account for personalized tools | Free account; soft‑pull profile data | ⭐⭐⭐⭐ — personalized soft‑pull odds & ongoing score monitoring (estimates) | Avoiding hard inquiries; shopping with approval‑odds; tracking credit progress | Soft‑pull prequalification, credit tools (alerts/simulator), personalized matches |

| Bankrate | Low — browse detailed hubs and editor picks | No cost; time to read; cross‑check offers | ⭐⭐⭐⭐ — reputable, regularly updated comparisons with methodology | Vetting fees/APRs; spotting predatory/high‑fee cards | Methodology transparency, vetted options, editor picks |

| WalletHub | Low — browse rankings and card detail pages | No cost; time to read; may need account for some tools | ⭐⭐⭐ — granular fee/deposit data + user reviews (varied quality) | Finding detailed fee/deposit info; seeing real‑user sentiment | Monthly rankings, aggregated reviews, comprehensive card data |

| Capital One (Fair & Building) | Medium — soft‑pull preapproval then apply | Account/application; possible refundable deposit for secured cards | ⭐⭐⭐⭐ — good odds for fair credit; issuer pathways for graduation | Fair‑credit applicants seeking issuer options and preapproval | Issuer preapproval (soft‑pull), automatic reviews, accessible secured options |

| Discover it Secured | Medium — secured card application & deposit | Refundable deposit (~$200+), bank info to fund deposit | ⭐⭐⭐⭐ — strong for building credit + rewards if balances paid | Building credit with cashback and no annual fee | Cashback rewards, reports to all 3 bureaus, no annual fee, graduation reviews |

| OpenSky Secured (Capital Bank) | Low — no credit check application | Refundable deposit (≈$100–$200+), possible annual fee | ⭐⭐ — highly accessible for credit establishment; limited graduation guarantees | Applicants declined elsewhere or with very thin/poor credit | No credit check application, low entry deposit, reports to all 3 bureaus |

From Rebuilding to Rewarding: Your Next Steps to Better Credit

Navigating the landscape of credit cards when you have a less-than-perfect score can feel daunting, but as this guide has shown, you have powerful options. We've explored a range of the best credit cards for bad to fair credit, from the comprehensive comparison tools at NerdWallet and Bankrate to specific, accessible products like the Discover it® Secured Credit Card and the OpenSky® Secured Visa® Credit Card. Each of these serves a critical purpose: to provide a stepping stone toward a stronger financial future.

The journey isn't just about getting approved; it's about building sustainable credit habits. A secured card, for instance, is not a final destination but a training ground. It allows you to demonstrate responsible credit use-on-time payments and low utilization-which lenders want to see. Your primary takeaway should be that these cards are tools designed to help you construct a positive payment history, the single most important factor in your credit scores.

Key Takeaways for Your Credit Rebuilding Strategy

To truly leverage the information in this guide, it's essential to move from knowledge to action. Your next steps will determine how quickly and effectively you can improve your credit profile and unlock better financial products in the future.

Here’s a summary of the most critical actions to take:

- Diagnosis Before Application: Before you apply for any card, you must understand your credit report's strengths and weaknesses from a lender’s perspective. Don't just look at the score; analyze the data behind it.

- Strategic Selection: Don’t just pick the first card that will approve you. Match the card's features to your goals. Are you looking for a card with a path to graduate to an unsecured product? Do you need a card that doesn’t require a credit check at all? Choose with intention.

- Responsible Utilization is Non-Negotiable: Once approved, your focus must shift to management. The golden rule is to keep your credit utilization ratio low, ideally below 30%, but even lower (under 10%) is better. This demonstrates to lenders that you are not reliant on debt.

- Consistency is Your Superpower: The most impactful thing you can do is make every single payment on time. Set up automatic payments or calendar alerts to ensure you never miss a due date. This consistent, positive behavior is what builds a trustworthy credit history over time.

How to Choose the Right Tool for Your Situation

Selecting one of the best credit cards for bad to fair credit depends entirely on your unique financial picture. If you have some positive credit history but a few blemishes, a starter unsecured card from a major issuer might be within reach. If you are starting from scratch or have significant negative items on your report, a secured card is almost always the most effective and accessible first step.

Think of it this way: the card you choose today is a key that can unlock prime lending opportunities tomorrow, including mortgages, auto loans, and business funding. For financial professionals, such as loan officers or credit repair specialists, guiding a client to the right starter product can accelerate their progress and improve their overall financial health. For a funding company, using a system like Score Machine to analyze and prepare a client’s credit profile before they apply increases the likelihood of approvals, thereby growing the company’s total funded deals.

The ultimate goal is to graduate from the "rebuilding" phase to the "rewarding" one, where you can qualify for cards with cash back, travel points, and premium benefits. This journey begins with a single, smart decision. By taking a proactive, analytical approach to your credit and choosing the right foundational tool, you are not just getting a new piece of plastic; you are investing in a future with greater financial freedom and opportunity.

Don't leave your approval to chance by applying blindly. Prepare for your application by analyzing your credit report with the same tools lenders use with Score Machine. Understand exactly what underwriters see so you can apply with confidence. Get your detailed credit analysis with Score Machine today!